by Wine Owners

Posted on 2018-09-14

Rioja was Spain’s answer to Bordeaux - incredibly high quality AND quantity produced from noble grape varieties (in Rioja’s case Tempranillo).

Back in the 1950s and 1960s the large Rioja houses were making wine of extraordinary quality to rival their Bordeaux neighbours to the north. By the 1980s and 1990s many Bodegas had let standards slip (with a few notable exceptions) and the outside world turned away from Rioja, creating a self fulfilling downward qualitative spiral. Since the early 2000s the region has turned itself around, make serious investments, and more recent vintages have attained (or perhaps even bettered?) the heights achieved of their great post-war vintages.

Rioja prices are still great value but the world is catching on, the positive cycle is established an the region’s future as a blue chip wine producing region is more or less assured.

The following shows the jump in the last 12 months of Rioja prices compared to the general Spanish Index (in which there is a hefty Rioja set of constituents as well).

For the budding collector, without access to unlimited funds, Rioja is the obvious region to buy into on a 10-year view.

by Wine Owners

Posted on 2018-03-23

The KFFWII is up 9.6% over the year to March 2018, with a 2% gain in the last quarter.

Consolidation of the market at current valuation levels is on the back of the 24 months to December 2017, seeing gains of 38%.

The top of the market is significantly influenced by Asian demand, where a weak dollar is causing bid prices to fall. Changes within secondary market wine distribution into China may create a degree of uncertainty not seen since 2014.

The outlook for the rest of 2018 is one of subdued growth, with the Sterling-denominated index at risk of downward pressure as the currency appreciates against the US Dollar and Euro.

Bordeaux

First Growths are up just 3.8% over the last 12 months, half of which can be accounted for by the last 3 months. This broadly reflects the rest of the Bordeaux fine wine market (classified growths and equivalents). However, this subdued performance ought not to detract from 3-year performance (43% price growth) in First Growths, and 55% appreciation in the classified growths and equivalents over the same period.

Risers substantially outnumber fallers in Bordeaux, reflecting the market's continued overall growth. Less new wine is being released from chateaux than ever before, and quality is increasingly consistent. These factors point to continued growth during 2018, although it will remain in single figures, as orderly trading patterns continue.

Burgundy

Burgundy values continue to appreciate, with increases of 21% to March 2018, and 4.6% over the last quarter. To date there are no signs of a let-up in the upward trajectory of top producers' Burgundy prices. We’re about to see Burgundy price appreciation break through the 100% mark over the last 5 years, and reach 257% over 10 years.

Northern Italy

Northern Italy (represented in the KFFWII exclusively by Piedmont and Tuscany), is up 9.5% over the last 12 months, of which 2.7% is within the last quarter. The leaderboard is dominated by Monfortino, the standout Italian performer of the last 4 years which is consolidating its position as one of the most investible wines in the world.

Expectations for Northern Italy - Barolo in particular - are that prices will continue to increase into double digits over the remainder of 2018.

Champagne

Vintage champagne has performed well over the year, up a full 10%, and has kicked up 3% in the last quarter.

The best performers are rarer cuvees from such stalwarts as Selosse, Bollinger, Krug and Pol Roger. Over 10 years Champagne has performed even better than Burgundy, up 283%: demonstrating the liquidity that volume can drive, brand values and early consumption patterns.

USA

California’s moderated growth continues, with annual performance to March 2018 of 6.3%, and is up 2% within the last quarter. After years of bewilderingly strong growth (385% over 10 years), fallers are as numerous as risers within the California index, implying further downsides or a relatively flat outlook.

Spain

Top Spanish wines dominated by iconic and traditional large estates in Rioja and Ribero del Douro still represent good value, have good ageing potential, and are produced in large volumes.

These positive trading fundamentals support a market up 8.25% in the last year, and a healthy 3% in the last quarter.

A related effect is that Spanish blue-chips (particularly Vega Sicilia's top wines) are increasingly being traded on exchanges, and markets are being made for these wines through the usual offer and bid mechanisms used by market-makers.

The Spanish index is up 155% in the last 10 years. 45% of that growth has taken place in the last 3 years. The timing of that resurgence coincides with the inflection point in Bordeaux markets in the winter of 2015, when they rebounded from cyclical lows.

by Wine Owners

Posted on 2016-03-23

With the base price taken on January 2008, the WO Bordeaux Index has significantly outperformed the Dow Jones Index, peaking at 147.33% as of 17 March, 2016, dwarfing Dow Jones' seemingly modest gains of 40.40%. With growing demand for Bordeaux market within the Asian market, such inflation in prices is undoubtedly set to increase. The WO Bordeaux Index's ability to weather through financial instability is also illustrated in its appreciation in the midst of the 2008-2009 financial crisis, obtaining a 74.73% increase compared to Dow Jones' depreciation of 43.60%.

Note: The Dow Jones Industrial index (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq.

by Wine Owners

Posted on 2016-03-10

The Wine Owners First Growths Index is up 3.71% Year to date, whilst the Medoc Classed Growth index is up 5.1% for the same period.

The Wine Owners Libournais Index - comprising top Pomerol and St Emilion wines - is also up 4.24% over the last 3 months.

Buyers are coming back into the market in the last few weeks and early signs are very promising: this feels very different to the various short lived rallies since 2013, and is on the back of single digit, consistent quarter on quarter gains over the course of calendar 2015.

The Wine Owners First Growths Index had previously risen 4.6% in 2015. The Medoc Classed Growth index had gained 9% over the course of 2015, with rises dominated by the older back vintages tracked in the vintage range 1996-2006. At this level versus the First Growths it’s noticeable that 2009s are also on the move up.

What does 2016 hold for the collector?

GET YOUR FREE REPORT TODAY

by Wine Owners

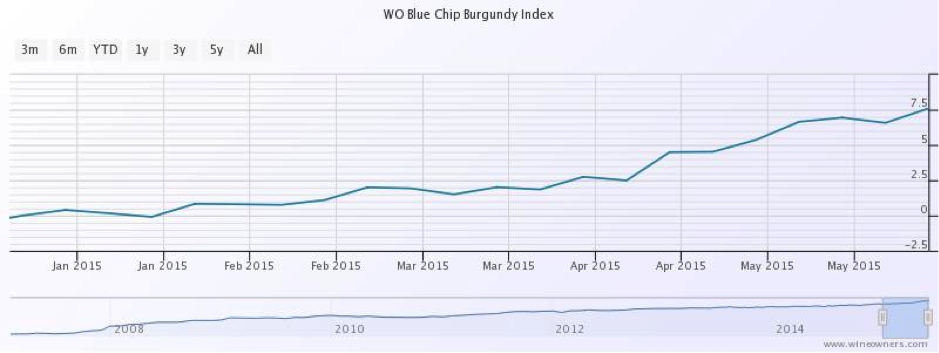

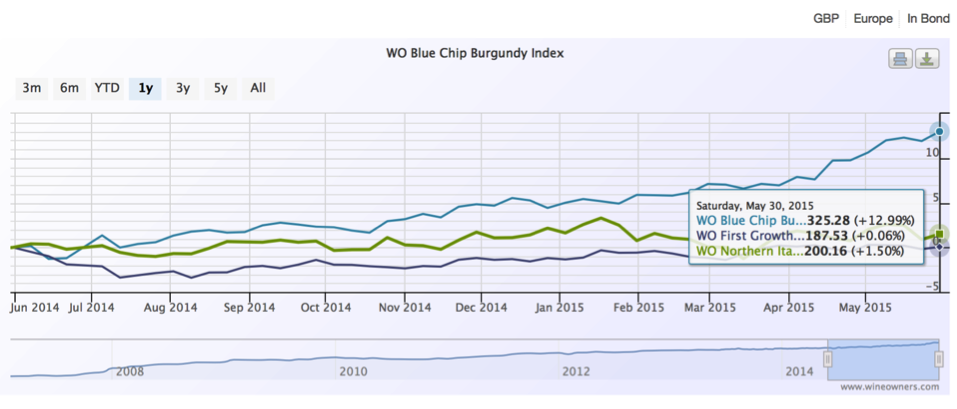

Posted on 2015-06-04

The WO Blue Chip Burgundy index continues to power ahead, up 5% in just 7 weeks.

Has this rise been driven by recent demand and auction performances in Hong Kong, or are we just seeing the latest kick upwards driven by increasingly difficult-to-find wines in the face of growing global appreciation?

Whilst to 2010 DRCs have fallen over the last year by 7-10%, the scarcest wines from blue chip producers have registered strong double-digit growth in the last year.

Burgundy is substantially outperforming Bordeaux First Growth performance and Northern Italy. First Growths show flat performance over the last 12 months, whilst Northern Italy has edged up by 1.5%.

You can see performance of indices and their constituent wines here.

by Wine Owners

Posted on 2014-08-14

Unsurprisingly, given the continuing market morosité over classed growth Bordeaux, the index plumbed fresh 2014 lows last week, down -3.83% since January, and -6.8% from this time a year ago. The right bank fared marginally better with the Libournais Index year to date (-2.68%) whilst year to date it was down -4.61%.

| Chateau Cheval Blanc Saint-Emilion Premier Grand Cru Classe A AOC |

2000 |

-16.15% |

£475.00 |

| Chateau Beausejour Becot Saint Emilion Premier Grand Cru Classe B AOC |

2000 |

-16.19% |

£41.31 |

| Chateau Belair-Monange Saint Emilion Premier Grand Cru Classe B AOC |

2010 |

-16.55% |

£81.66 |

| Chateau La Fleur Petrus Pomerol AOC |

2001 |

-16.78% |

£93.70 |

| Chateau Latour a Pomerol Pomerol AOC |

2005 |

-17.02% |

£48.71 |

| Chateau Le Tertre Roteboeuf Saint Emilion Grand Cru AOC |

2001 |

-17.63% |

£100.72 |

| Chateau Beausejour Duffau-Lagarrosse Saint Emilion Premier Grand Cru Classe B AOC |

2005 |

-17.90% |

£48.33 |

| Chateau Cheval Blanc Saint-Emilion Premier Grand Cru Classe A AOC |

2005 |

-18.70% |

£325.00 |

| Chateau Figeac Saint Emilion Grand Cru AOC |

2009 |

-18.99% |

£120.83 |

| Chateau Clos L'Eglise Pomerol AOC |

2001 |

-19.55% |

£71.46 |

| Chateau Beausejour Becot Saint Emilion Premier Grand Cru Classe B AOC |

1998 |

-19.82% |

£32.89 |

| Chateau Latour a Pomerol Pomerol AOC |

2001 |

-20.04% |

£32.36 |

| Chateau Ausone Saint Emilion Premier Grand Cru Classe A AOC |

2005 |

-21.21% |

£802.05 |

| Chateau Moulin Saint-Georges Saint Emilion Grand Cru AOC |

2000 |

-21.74% |

£34.45 |

| Chateau Hosanna Pomerol AOC |

2000 |

-21.79% |

£111.60 |

| Chateau Clos L'Eglise Pomerol AOC |

2009 |

-24.12% |

£98.24 |

| Chateau Ausone Saint Emilion Premier Grand Cru Classe A AOC |

2000 |

-25.02% |

£750.00 |

| Chateau Larcis Ducasse Saint Emilion Premier Grand Cru Classe B AOC |

2000 |

-26.15% |

£26.77 |

| Le Dome Saint Emilion Grand Cru AOC |

2000 |

-40.75% |

£76.41 |

The First Growth Index is down -10% year to date and -27.9% since summer 2011 highs. However, there are some surprisingly low prices on back vintages being seen on the fine wine exchange. How about Latour 2004 at £3,050 IB per 12x75cl excluding buyer’s commission? Or Margaux 1996 at £3,500 IB per 12x75cl - one of their great vintages, drinking beautifully now. Frankly, with pretty good to excellent back vintages fetching these kind of prices, no wonder there are no takers for the recent string of Bordeaux off-vintages. The risk to discount ratio is simply not compelling enough. No doubt the market will sort that out over the next couple of years. Contrarily, good to great vintages with 6-10+ years under their belts are starting to look very attractive in places, at least in our eyes, and there’s a trend towards restocking within the fine wine trade - a positive sign.

Looking at constituents of the Wine Owners 150 (which comprises 150 Investment Grade Wines across the top 40 performers of the last 10 years), the leaderboard is topped by Monfortino 2002, up 39% in the last 12 months. This is a romantic, if not heroic performance, from one of the greatest wines in the world defying the miserable conditions of the vintage with its superlative microclimate and the producer’s belief in the intrinsic quality of the wine.

Year on year top performers (Wine Owners 150):

| Giacomo Conterno Monfortino Barolo Riserva DOCG |

2002 |

39.06% |

£338.62 |

| Screaming Eagle Winery Cabernet Sauvignon Napa Valley AVA |

1995 |

28.99% |

£3,135.00 |

| Domaine Jean-Francois Coche-Dury Corton-Charlemagne Grand Cru AOC |

2005 |

28.50% |

£2,015.74 |

| Tenuta dell' Ornellaia Masseto Toscana IGT |

1998 |

20.66% |

£454.00 |

| Petrus Pomerol AOC |

2001 |

18.28% |

£1,400.00 |

| Tenuta dell' Ornellaia Ornellaia Bolgheri DOC |

2004 |

16.53% |

£133.33 |

| Tenuta dell' Ornellaia Masseto Toscana IGT |

1997 |

15.94% |

£516.67 |

| Chateau Le Pin Pomerol AOC |

2009 |

14.92% |

£2,291.67 |

| Domaine de la Romanee-Conti Richebourg Grand Cru AOC |

2002 |

12.08% |

£1,130.35 |

| Dominus Estate Bordeaux Red Blend Napa Valley AVA |

1997 |

10.66% |

£107.27 |

| Domaine de la Romanee-Conti Romanee Conti Monopole Grand Cru AOC |

2001 |

9.62% |

£7,353.97 |

| Tenuta San Guido Sassicaia Bolgheri DOC |

2006 |

9.36% |

£137.50 |

| Joseph Phelps Winery Insignia |

1997 |

9.19% |

£163.90 |

By the way, not one Medoc classed growth made it into the top 20 of the Wine Owners 150, with the best performing representative of the region being Pichon Baron 2000.

| Chateau Pichon Baron Pauillac Deuxieme Cru Classe AOC |

2000 |

2.47% |

£125.00 |

by Wine Owners

Posted on 2014-07-14

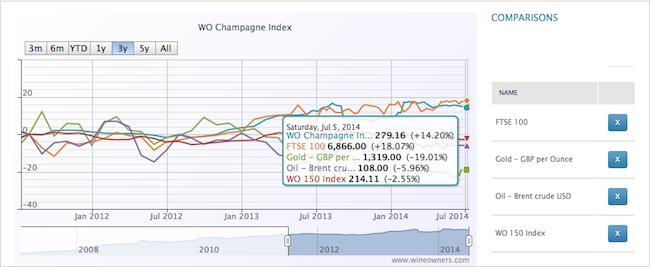

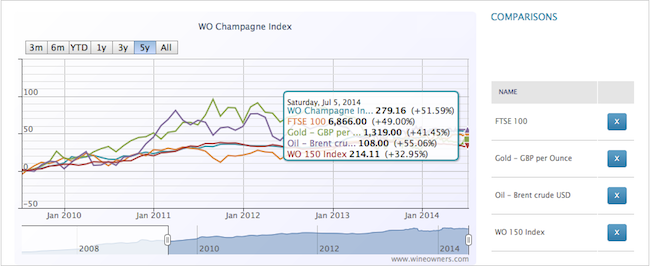

The performance of the Wine Owners Champagne Index has been nothing short of stellar - outperforming most other assets over the last 3, 5 and 7 years.

Over the last 12 months, however, the index has stagnated, registering a measly 0.5% growth.

Much was said of Champagne as an investment during the course of 2013. In sharp contrast to other fine wine regions, production quantities tend to be vast, but so is consumption. Analysing the performance of the Champagne market shows that appreciation is entirely driven by the very top vintages. With no stellar vintage such as 1996 or 2002 due for imminent release, we said in the first quarter of 2014 that the vintage Champagne market may drift over the next 1-2 years, though very top back-vintages may well benefit as supply dries up, and Champagne styles suited for long ageing such as Salon may continue to firm.

6 months on, this has indeed proved to be the case, with the top performers over the last 12 months to July 2014 being Jacques Selosse Blanc de Blancs Millésimé 1996 (+40%), Krug Clos de Mesnil Blac de Blancs 1996 (+28%) and Salon Cuveé ’S’ Le Mesmil Blanc de Blancs 1996 (+16.5%). This shows the value of relative scarcity, age and a top vintage - the perfect combination for future returns in a market otherwise dominated by exceptionally high volume production.

The poorest performers over 12 months have been Taittinger Contes de Champagne Blanc de Blancs 1996 (-9%) and 1998 (-28%), along with Dom Perignon 1998 (-11%).

by Wine Owners

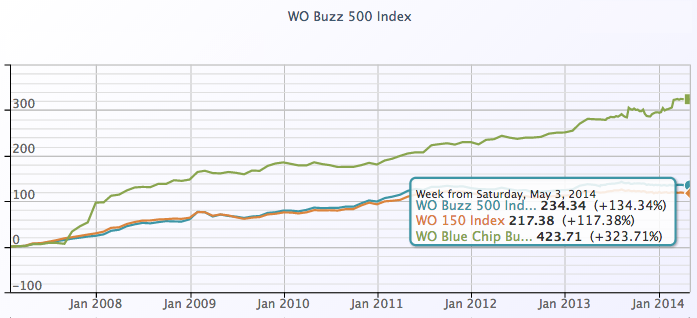

Posted on 2014-05-08

The Buzz 500 was always meant to be a bit of fun. Away from the serious business of formulating the fine wine equivalent of the FTSE100, and key region of production tracker indices, we thought it would be interesting to create a ‘popular’ index.

So we took the 100 most searched for wine names on Wine-Searcher, selected 5 vintages per wine that differed according to region, and turned that list into an index. Well, why not?

We wanted answers to the question: are those wines that are most searched for on Wine-Searcher also those that perform the best over the medium term? Will the most searched-for wines tend to be the most demanded? Does most researched translate into purchases, and does that lend support to, or underpin market pricing?

We kicked off the Buzz 500 at the start of 2013, and from that point onwards, it’s outperformed the WO150. That’s not entirely surprising given the strong Bordeaux representation in the latter index. But actually the Buzz 500 has plenty of claret represented too, just different wines. This highlights the first conclusion: there are always outperformers in any segment, and there is a correlation between the most searched for wines in a category and their performance versus other birds of a feather.

You can Review the constituents of each of the indexes here.

But just because hot wines within a category will outperform other wines in the same category, there’s no substitute for market momentum: and nowhere has that been greater than in burgundy these past three years.

So comparing the Buzz 500 to the Blue–chip Burgundy index is – well, rather predictable.

Whilst Burgundy has risen 40% in the last 3 years, the Buzz 500 has managed a paltry 5.5%. That’s still a third better than the poor WO150, weighed down by its First Growth constituents.

If you're a Burgundy officianado that may be good news, or conversely may have put whole classifications of wine out of your drinking reach. And whilst the scarcity of Burgundy is a huge market driver that may point to inexorable upwards momentum, who’s to say it will continue?

The wine market is characterised by myopia – unable or unwilling to see an end to positive trends, and morose in the extreme when sentiment turns . Neither are helpful for collectors.

One behaviour that is consistently predictable is that when wine markets become disconnected with the value in those purses that consume it, the trade and consumers search for better value, Hence the positive kick enjoyed by Northern Italy. More about that in my next index analysis.

by Wine Owners

Posted on 2014-04-22

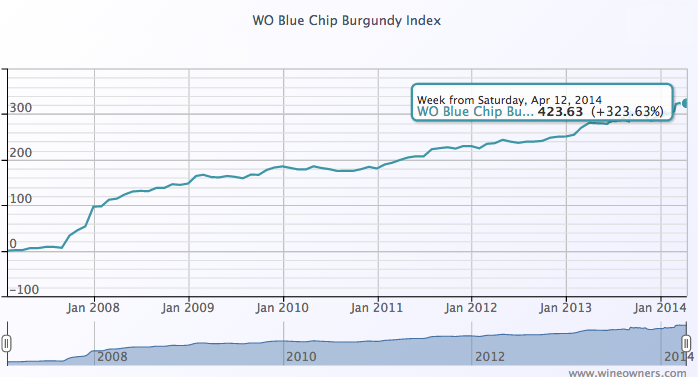

The Blue Chip Burgundy Index is focused on Grand Cru and a small number of top Premier Cru burgundy from the region’s top producers.

These wines are difficult to get allocated at first release in the first calendar quarter two years after harvest, and tend to jump in value as soon

The Blue Chip Burgundy Index is focused on Grand Cru and a small number of top Premier Cru burgundy from the region’s top producers.

These wines are difficult to get allocated at first release in the first calendar quarter two years after harvest, and tend to jump in value as soon as they find their way into the secondary market - such is the competition to own them. So buying in at first release gives the buyer the greatest upside, yet as the graph shows, the upward trend has been irresistible over the last 7+ years.

Once acquired, a significant proportion of these wines never see the light of day again except for when a cork is pulled a decade or so after release. Such is the passion for great burgundy. Does the incredible market performance over the last few years change that we wonder, as more elite producer wines become ultra-expensive - and straying into the lower reaches of DRC, Leroy and Jayer price territory? Nothing has performed as well as fine burgundy in this period, and burgundy’s charted performance (blue) versus the Medoc and Libournais indices (green and orange respectively) looks even more dramatic when compared over the last 3 years.

as they find their way into the secondary market - such is the competition to own them. So buying in at first release gives the buyer the greatest upside, yet as the graph shows, the upward trend has been irresistible over the last 7+ years.

Once acquired, a significant proportion of these wines never see the light of day again except for when a cork is pulled a decade or so after release. Such is the passion for great burgundy. Does the incredible market performance over the last few years change that we wonder, as more elite producer wines become ultra-expensive - and straying into the lower reaches of DRC, Leroy and Jayer price territory? Nothing has performed as well as fine burgundy in this period, and burgundy’s charted performance (blue) versus the Medoc and Libournais indices (green and orange respectively) looks even more dramatic when compared over the last 3 years.

by Wine Owners

Posted on 2014-04-01

The Wine Owners 150 (WO 150) comprises Investment Grade Wines across the top 40 performers of the last 10 years. The goal of the WO 150 is to provide a stable and reliable index for comparison periods over extended periods of time. Because the wine performance is made up of many sub-markets, some of which have risen strongly whilst Bordeaux continues to fall acting as a significant counterweight given its significant representation. The WO 150 reflects a classic portfolio of blue chip wines.

Within the WO 150 index, top performers over the last 3 months seem to reflect a very broad-based group of wines:

Worst performers

Unsurprisingly Bordeaux dominates at the bottom end of performance, where the first quarter of 2014 has seen some quite sharp falls. Interestingly Monfortino 2002 finds its way into this company, in sharp contrast with Northern Italy generally and other vintages from this top micro-cuveé Barolo. Seemingly the market will price in the perceived quality of a vintage, irrespective of how dramatically a specific wine outperforms.

Go to the indices page to see a range of other more specific markets. Want to see an index we don’t yet have? Ask us and we’ll set one up for you if we think it’s of general interest!