by Wine Owners

Posted on 2021-07-27

(in which we discuss why this is such a good idea!)

Miles Davis, July 2021

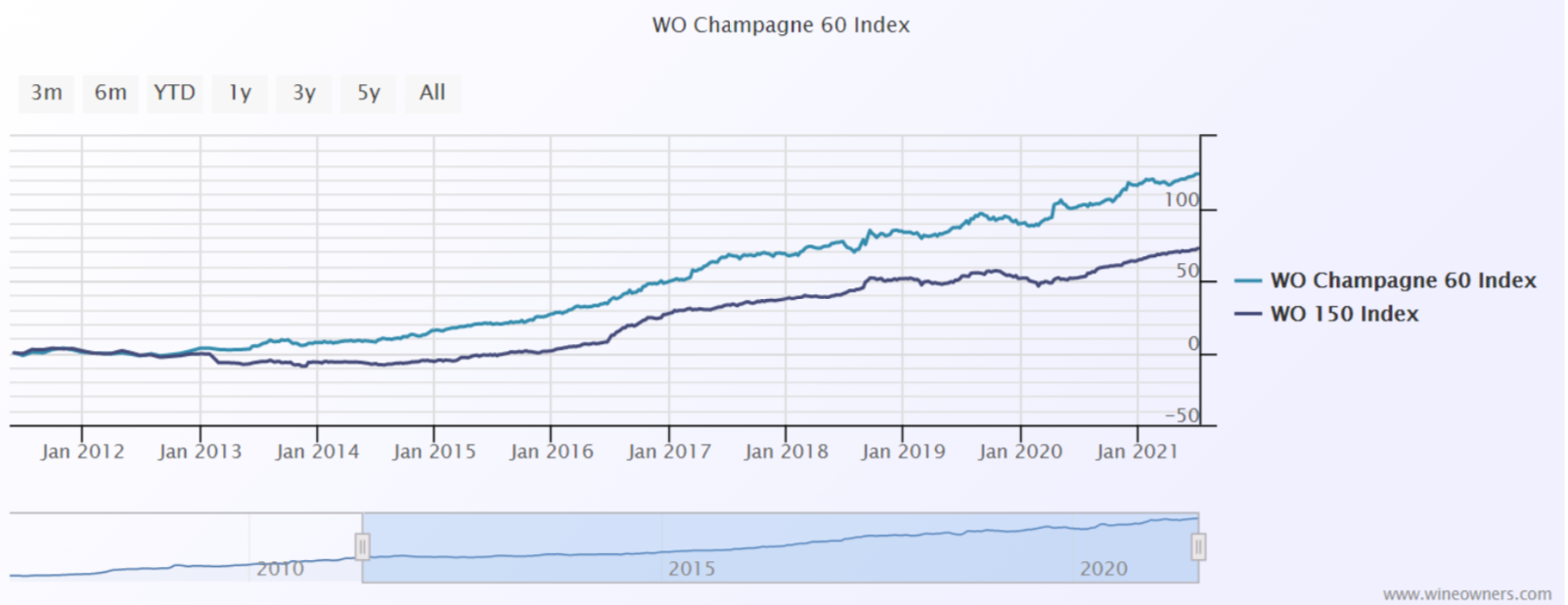

Vintage Champagne has been a sound investment for the last ten years, with our index annualising a return of 8.6%. The index is comprised of all the top cuveés from the giants of this most celebrated of wine regions, Dom Perignon, Krug, Louis Roderer Cristal, Pol Roger, Salon, Taittinger et cetera, et cetera. Indices never contain costs but that is not something many people bother to point out!

Champagne is, quite rightly, associated with luxury, celebrations, and fun, and is a genuine mood lifter. It is sprayed across crowds, associated with brazen displays of wealth in society hot spots, served at all manner of celebratory events, whilst also being adored by genuine connoisseurs – it finds a home across multiple layers of society and across the globe. Most of us are introduced to it at quite an early age through Bond, James Bond. In ‘Goldfinger’ Bond drinks Dom Perignon ’53, and that is what did it for me, I was hooked, although it took a fair few years after that to get my hands on the stuff! Vintage Champagne can age for decades and as supply runs down, so the price goes up (see below). It is probably the steadiest performer of all the sub sections of the fine wine market and some Champagne should be in every single cellar, collection, or portfolio always and forever!

Champagne has not really been treated as an investment staple within the wine world until relatively recently. The performance of famous brands and now the turnover in the secondary market makes it qualify for that description with consummate ease.

I have looked at these five vintage champagnes, based on their overall quality and their liquidity in the secondary market, from only the best vintages of modern times. Here are their prices (per bottle):

| Vintage | 1990 | 1996 | 2000 | 2002 | 2004 | 2006 | 2008 | Average |

| Current prices | | | | | | | | |

| Comtes de Champagne | 462 | 376 | 156 | 225 | 104 | 90 | 125 | 220 |

| Cristal | 374 | 371 | 209 | 221 | 165 | 137 | 208 | 241 |

| Dom Perignon | 269 | 317 | 200 | 167 | 124 | 119 | 130 | 189 |

| Krug | 508 | 350 | 225 | 281 | 189 | 171 | - | 287 |

| Winston Churchill | 393 | 319 | 192 | 175 | 132 | 132 | 165 | 215 |

Comtes is made by Taittinger, Cristal by Louis Roderer, Dom Perignon by Moet Hennessy and Winston Churchill is Pol Roger’s top cuvée.

What is quite amazing is how similarly these are all scored, (using WO aggregated methodology):

| Vintage | 1990 | 1996 | 2000 | 2002 | 2004 | 2006 | 2008 | Average |

| WO Points | | | | | | | | |

| Comtes de Champagne | 95 | 94 | 96 | 97 | 96 | 95 | 96 | 95.6 |

| Cristal | 96 | 95 | 93 | 94 | 96 | 95 | 98 | 95.3 |

| Dom Perignon | 94 | 95 | 93 | 97 | 95 | 95 | 98 | 95.3 |

| Krug | 96 | 97 | 94 | 96 | 97 | 97 | - | 96.2 |

| Winston Churchill | 96 | 94 | 95 | 96 | 93 | 96 | 96 | 95.1 |

Here are the PPP (price per point) scores, to establish what is good value:

| Vintage | 1990 | 1996 | 2000 | 2002 | 2004 | 2006 | 2008 | Average |

| PPP (Price per point) | | | | | | | | |

| Comtes de Champagne | 4.9 | 4 | 1.6 | 2.3 | 1.1 | 0.9 | 1.3 | 2.3 |

| Cristal | 3.9 | 3.9 | 2.2 | 2.4 | 1.7 | 1.4 | 2.1 | 2.5 |

| Dom Perignon | 2.9 | 3.3 | 2.2 | 1.7 | 1.3 | 1.3 | 1.3 | 2 |

| Krug | 5.3 | 3.6 | 2.4 | 2.9 | 1.9 | 1.8 | - | 3 |

| Winston Churchill | 4.1 | 3.4 | 2 | 1.8 | 1.4 | 1.4 | 1.7 | 2.3 |

Although Vinous Media only has a range of between 93 points (2000 vintage, easily the weakest of this selection) and 97+ (2008) for the different vintages, those in the know realise that ’08 is a mega vintage with ’02 breathing down its neck, which is on a par with ’96, and all of those slightly better than ’04 and ’06 and this is already reflected in the prices.

The wines are all superb, but some more superb than others. If the PPP is way below the average (in red) for any of the wines, I have little hesitation in recommending them.

When thinking about possible returns I have compared prices from the ’02, ’04, ’06 and ’08 vintages relative to the ’96 price and adjusted for time (10 years for the ’06, 12 for the ’08) for example and have come up with the following numbers (obviously this is just a simplistic exercise but interesting nonetheless):

| Vintage | 2002 | 2004 | 2006 | 2008 |

| Annualised ROI benchmarked to '96 price* | | | | |

| Comtes de Champagne | 8.90% | 17.40% | 15.30% | 9.60% |

| Cristal | 9.00% | 10.60% | 10.50% | 7.00% |

| Dom Perignon | 8.30% | 10.20% | 8.50% | 6.30% |

| Krug | 3.70% | 13.90% | 7.40% | - |

| Winston Churchill | 10.50% | 11.70% | 9.20% | 5.70% |

*No dealing, logistics or storage costs factored in

And lastly, a look at the production levels; the Champagne houses are notorious for keeping their levels of productions under wraps, but I have gleaned some information (not necessarily 100% accurate):

| Production levels (across all top cuvées, white and rosé) | Bottles | |

| Comtes de Champagne | 140,000 | 2002 = 60,000 |

| Cristal | 400,000 | 2009 = 800,000 |

| Dom Perignon | 1 mill | |

| Krug | 200,000 | |

| Winston Churchill | 120,000 |

|

Of these names, Krug is on top of the pile in reputation, stature and price, Cristal and Dom Perignon are next, are truly international (and are made in huge quantities) and Comtes and Winston Churchill are more the sensible man’s choice for the price/quality ratio. I think they all make sense in their own different ways. Obviously, there are many more choices out there and grower Champagne is becoming ever more popular, but these names are dependable and highly liquid. And taste just so darn good… in case we forget!

by Wine Owners

Posted on 2021-07-19

Miles Davis, July 2021

If you are a regular reader, I would not be offended if you stop here as I am only likely to be repeating myself. The overall market is dull, unexciting, but mainly just plain boring. Sure, there are excitements here and there, an attractively priced en primeur release for example, see a snapshot report of that here, but let us stick to boring. What I mean by boring is that the market continues to be slow and steady and gently rising, not booming and busting, peaking and troughing etc. etc. It is calm, well underpinned by global demand - and a good place to be. To date, my two best investments (not including fine wine obviously!) have been in businesses that, could possibly have been described as boring: pensions administration and company records management - what a snore! They never shot up, or plunged, they just gently attracted more clients and more revenue, month by month, year by year, and have both done very well indeed. So, as you can see, I like boring.

Obviously, I jest but the message is clear. Recently I have even found myself telling clients desperate to sell something to hold on – what sort of a salesman does that!? And of course, I could turn out to be wrong. But… I happen to think the market has had its shock absorbers tested to the max and has survived and prospered in this low interest rate environment. In the last couple of years, we have had political turmoil in Hong Kong, the madness of Trump and his trade tariffs (now all lifted), Brexit and the dreaded C word. Clearly people are still drinking fine wine, perhaps possibly finer wine than normal, as less hard-earned cash is being spent in restaurants. The undercurrent to the whole market is firm, blue chip Bordeaux is well bid and is enjoying its best time for quite a while, and all of this is being achieved in an unfriendly exchange rate environment. GBP strength normally stifles wine prices in the secondary market, and vice versa.

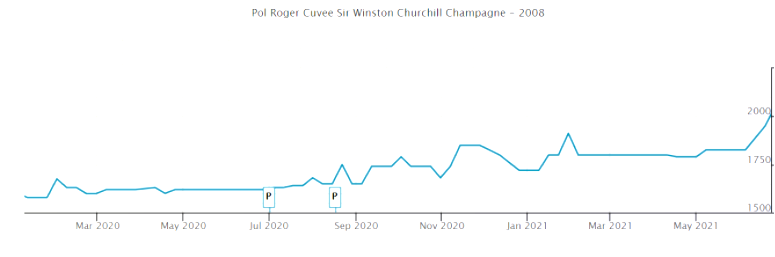

Champagne continues to attract a lot of interest and we have traded significant chunks of Krug ‘04, and Bollinger Grand Année Rosé ’12 recently. As I have written before, I very much like Pol Roger’s Winston Churchill cuvée as it not only delivers on the great price/quality ratio, but it is made in tiny quantities compared to its peers. The ’08 has done very well indeed for followers in recent months, up 20% in the last year (price is 12x75cl):

The 2006 now looks good value in comparison at c.£800 per 6 with stocks dwindling, and I have no hesitation in recommending that. I drank the ’02 recently and it was sensationnel! (C. £1,050 per 6). The ’04 also looks to offer value.

It would appear Rosé Champagne is having a great time of it, with Sainsburys reporting sales growth of nearly 200% recently. I mused on the subject a few weeks back (read the article here), and fear I have been missing out over the years!

Highly priced trophy Burgundy has been selling well again after a bit of a lay off through ’19 and ’20 and sensibly priced DRC, Rousseau etc. do not remain on the platform for long. The gap between the very top level of superstars and the middle tier seems to be widening again, surely pointing to value in the more mid division?

White Burgundy deserves another mention, especially given some reasonably heavy frost damage in the region earlier this year. This will lead to lower supply levels and therefore higher pricing. Load up on 2017s from the best stables if you can find them! The best stables continue to outrun the pack, but can this continue for ever? I doubt it.

Highly priced Piedmont has been slightly disappointing of late, whereas lesser money bets in the area have been rewarding. Surprisingly, superb releases from 2016 from some of the biggest names in the region are still available to buy at release price levels, notably Giacomo Conterno’s Cascina Francia and Bruno Giacosa’s Falletto. The former is extraordinary given Conterno declined to make a Monfortino in 2016 due to ‘stylistic’ matters, seems weird to me! Monfortino, acclaimed as Italy’s greatest and certainly most expensive wine, is made from vines within the Francia vineyard and the latest release from 2014 is offered at £750 a bottle, the Cascina Francia ’16 (an epic vintage in case anyone needs reminding!) at £200. I understand that it will never be a Monfortino, but still…There is still a lot of relative value in Italy, as described here, with mega points for little money readily available. For more money and mega points, the Super Tuscans keep travelling well.

Faring much better in recent months is the performance of wine prices from the Rhone Valley, not surprising given that wines from this region have a lot in common with the Italian theme I mention. There are some mega stars, Guigal’s single vineyard Cote Roties, producers such as Rayas and Bonneau (both Chateauneuf du Pape) Jean Louis Chave (Hermitage), Allemand (Cornas), and Jamet (Cote Rotie) to name a few that trade for big money, but otherwise there are some very affordable high scoring monsters that come (very) relatively cheaply. Even the big money wines trade at a massive discount to their Bordeaux and Burgundy equivalents. The one wine that really sticks out for me is Hermitage La Chapelle from Jaboulet. This extraordinary terroir is capable of producing the very finest wines ever made, the ’61 and ’78 for example (discuss). The last eleven vintages have averaged 97 points and are offered at an average price of £125 per bottle, an absolute snip in fine wine terms!! They also offer a fine second wine, La Petite Chapelle, for those who want a gentle introduction. Seasoned investors have had the Rhone pushed at them before and it has not really worked for them, but I think we live in different times now.

Having said that, the last part of the quarter was stifled by an uninspiring 2020 Bordeaux en primeur campaign and most merchants seemed relieved when it was over. The Covid induced price cuts of 2019 genuinely sparked interest in the old dog, but it was largely back to business as usual from the Bordelais and the bashing started all over again. The campaign started well with a great release from Cheval Blanc but by the end the crowd were throwing fruit and veg onto the stage. As diversity spreads there are more and more stages to consider, and good returns are derived from proper opportunity. I am very pleased to see the grand vins of Bordeaux performing well in the secondary market as it lifts the market as a whole but the slavish obsession that the wine industry pays en primeur saddens me – so, it’s back to other business!

As always, please feel free to call to discuss, or bowl me some fast balls. And have a very lovely summer!

Miles 07798 732 543

by Wine Owners

Posted on 2021-07-11

Will Cheval Blanc and Ausone no longer be Grand Cru Classé ‘A’ as from the 2021 vintage?

If so, it won’t be because of the Commission de Classement. The closing of the Saint-Emilion classification applications took place on June 30 and neither Cheval Blanc nor Ausone returned their copies.

Unlike the left bank classification system of 1855 that is pretty much immutable (with the exception of Mouton’s promotion to Premier Cru in 1973), the St Emilion classification is reviewed approximately once every 10 years, permitting a periodic revaluation of quality and performance. It’s not all been plain sailing; the 2006 reclassification was plagued by accusations of impropriety and was eventually annulled. Consequently, tastings conducted for the 2012 reclassification were outsourced to independent groups from across France to rehabilitate the process.

Cheval Blanc and Ausone, the first St Emilion producers to be awarded Classé A classification in 1954 when it was created, are effectively leaving the classification system.

The Classé A incumbents evidently concluded that the system is no longer sufficiently discriminating to reflect the ranking of their respective properties compared to their peers.

This bombshell threatens to undermine the kudos and financial benefits of promotion to Classé A, and in turn the market pricing potential of those that are elevated. Not to mention it raises questions of the credibility of the St Emilion classification system more broadly.

So what does the two colossus’s departure say about the process of decennial review? How does this reflect on the composition and process of the Commission de Classement?

Is Grand Cru Classé A about to lose its lustre; devalued by ambitious properties busy erecting glitzy edifices? Concrete and stone, some say, matter more than they ought to compared to the brilliance of the wines and their track record.

Or, is Classé A promotion a reflection of the qualitative transformation we see taking place in St Emilion - given the strongly weighted preconditions of a sustained track record of exceptional results and market recognition - and therefore are not elevations thoroughly deserved?

Let’s see what happens over the coming weeks. Can Cheval Blanc and Ausone be courted back into the fold, or is their departure (by omission of submission) a fait accompli? Assuming the latter, perhaps we'll see more promotions next year than we might have otherwise. What effect this all has economically on those producers who attain Classé A classification is now more uncertain than ever.

by Wine Owners

Posted on 2021-07-08

Top seller:

Cheval Blanc, came out early and flew out the door

Relative value analysis winners (based on JancisRobinson.com scores)

Batailley

Beau Séjour Becot

Clinet

Du Tertre

La Gaffeliere

Laroque

Latour Martillac Blanc

Please see our full analyses of the vintage's releases and identification of great buys (some from 2020 and many more from comparative back vintages) on the Jancis Robinson forum here.

Top buys for an immediate return:

Carruades

Carmes Haut Brion

Possible St Emilion reclassification bets (due 2022 in order of likelihood):

Figeac #1

Canon #2

Belair Monange #3

Top First Growth of the vintage:

Margaux

Wines to watch:

Durfort Vivens

Finally getting noticed with commensurate scores. 2016 was a watershed vintage of great harmony and precision, and the first major Bordeaux property to qualify for both biodynamic certifications. 2018 was an epic qualitative success, even though it was a disaster commercially due to rampant mildew that swept the vineyard in June - the biodynamic treatment regime unable to keep up with the excessively humid conditions. Only 583 equivalent full cases were made and the quality compares to 1945 and 1961. 2020 is another success with modestly reduced yields. The attack in particular is gorgeous, dripping with juicy black cherry fruit, but 2018 is the one to seek out.

La Gaffeliere

For those who missed the Figeac boat before it left the harbour, La Gaffeliere is still at anchor in terms of price, and with every prospect of setting sail with a bit of time. Great terroir next to Ausone, seriously elegant, with layer upon layer of complexity to seduce the connoisseur.

Best commune bets in 2020?

St Emilion

Margaux

Pomerol

Themes of 2020

Black bottles with gold engraving. What Chateau Margaux started off, in 2015 as a fitting tribute and wonderful enduring memorial to the late Paul Pontallier, became ubiquitous in 2020 in honour of all sorts of anniversaries. The black bottle salesperson was probably not referencing their list of ‘wins' in 2020 with their prospects, for fear of undermining the hoped-for premium packaging premium.

Modest increases at the beginning of the campaign over the very well priced 2019s (as is so often the case) ended with a frenzy of price increases for the late releases of between 25%-c40%. Sellers will have had to bank on Giffen’s Paradox to sell through at the top end of price hikes.

2020 vs 2019

There were still values to be had in 2019 at the start of this campaign. Better priced 2019s that were down on their 2018 release prices and which hadn’t budged since last year’s release price got snapped up as this year's campaign played out. There are still plenty to pick from. Overall 2019 is likely a more consistent vintage than 2020, and perhaps rather more balanced in the Medoc notwithstanding plenty of low alcohols in 2020 (partly due to rain which most affected the top half of the Medoc notably St Estephe, Pauillac, a bit less in St Julien, and quite a bit less in the heart of Margaux). Left bank wines’ stats offered up a paradoxical combination of moderate alcohols and very elevated pH values (denoting low acidity in spite of tasters' visceral sense of freshness). The Right Bank got spared the later downpours and so are richer; many with the higher trademark alcohols of a hot vintage (notably the 100% Merlots) but with pH values closer to norms.