by Wine Owners

Posted on 2019-02-11

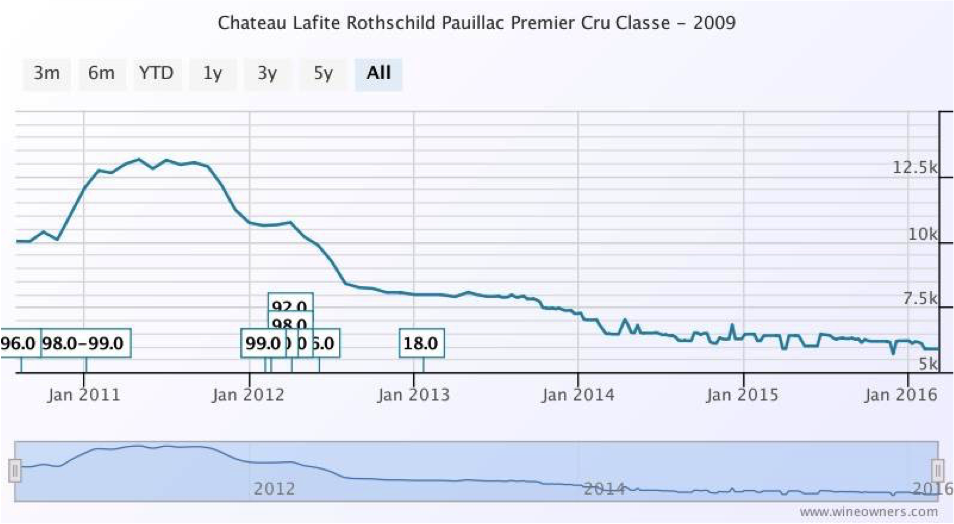

If you’re looking to buy some Lafite, the 2010 vintage looks like reasonable value, given we are talking the brand that is Lafite. It achieves the highest WO score of 98 (extraordinarily high given our rather ‘mean’ methodology) and it comes from the vintage that is establishing itself as the pinnacle of the modern era, perhaps to be challenged by ’16 but that hasn’t been confirmed as yet.

If we brought the price down to the level we can actually offer at (£7,225 net per 12 as opposed to the chart price of £7,475), the Relative Value Score rises to above 6 – cheap for Lafite!

by Wine Owners

Posted on 2018-04-10

Starting early, we hit the Monday-morning Bordeaux commuter congestion armed with laptops, phones and an excellent pain au chocolat. Day one launched us headlong into the Medoc grand crus, starting at Lafite, then moving through Mouton, Cos d'Estournel, Pontet-Canet, Calon-Segur, Montrose, finishing at Chateau Margaux.

©Jonathan Reeve / Wine Owners

Tongues still tingling from untamed tannins, we are now reviewing the day from the wine-free environs of our rented loft- conversion apartment. There is blue sky peeping through the skylights.

Three main themes emerged from today's en primeur 2017 tastings:

Cabernet Cornucopia

The most obvious pattern is that 2017 was clearly a Cabernet vintage in Pauillac and Saint-Estephe. Almost all of the wines we tried have a higher proportion of Cabernet Sauvignon in their blends than in 2016. The particular weather patterns of the 2017 growing season meant that Merlot was tricker in 2017, and Cabernet performed well. Lafite, Montrose and Calon-Segur particularly exemplified this - their wines glowing from the healthy Cabernet. The Calon tasting demonstrated this most clearly; comparing side-by-side the Marquis de Calon and the Calon-Segur (Cabernet was particularly higher in the latter) it became clear how a higher percentage of Cabernet has worked wonders in 2017. The Calon is fresher, brighter and more defined than the Marquis, has more-focused acidity, and will be by far the longer-lived wine.

A noteworthy exception to this pattern is the grand vin at Chateau Margaux, where the team are obviously very happy with their Merlot this year. In fact, their Merlot was apparently so good that it was used worthy of a greater dose in the grand vin this year - a move which brought production levels of the grand vin up to almost 2015 levels (impressive from the smaller 2017 vintage). This is an unusual moment of glory for Merlot, which is typically the ‘insurance policy' grape.

House Styles

One obvious pattern showing in day one's tastings was house styles. These are very much in evidence in 2017, and most obvious at the Mouton stable, where d'Armailhac, Petit Mouton, Mouton and Aile d'Argent all shared the house's exuberent, borderline-exotic richesse. This continues right down to the house's entry-level Baronarques brand from Limoux, which we were also warmly invited to taste. The four Cos d'Estournel wines also had a family feel about them, being clean, bright and focused, without being overly ‘new world'. The pattern was most pleasing, perhaps, at Montrose, where both the Dame de Montrose and the grand vin showed brilliantly, and shared a distinctive style; cool, fresh wines (yes, high Cabernet content) with lots of tightly wound potential, and a whiff of something herbal (along the lies of nettles and lavender) marking them out from the crowd.

©Jonathan Reeve / Wine Owners

Past and present

References to the past, as a means of promoting the present, were frequent in the presentations today.

Lafite's new director, Jean-Guillaume Prats (previously of Cos d'Estournel), pointed to technology as being significant in the quality of this 2017 vintage. Thirty years ago, he said, given the same vintage conditions, it would have been 'very tricky' to make a wine of such high quality as they have managed this vintage with both the Carruades and grand vin. Of course, his job is to say such things, but his demeanour was very real, honest and open. And the wines spoke for themselves; the Lafite was its usual elegant, impressive self even at this early stage in its life.

Also illustrating progress by pointing to the past was Thibault Pontalier of Chateau Margaux, who highlighted that the blend of Pavillon Rouge today is exactly the blend of the grand vin thirty years ago. A strong part of his reasoning for this was the ever- increasing quality of Cabernet Sauvignon that Margaux is able to produce, thanks to investment in technique and technology. This was in evidence for more than just the reds, however; Margaux's stunning Pavillon Blanc 2017 ended today with a refreshing flourish of beautifully concentrated, linear Sauvignon.

©Jonathan Reeve / Wine Owners

Comparing 2017 with 2016, the majority of wines from day one appear to be a notch less intense and refined than 2016. We're interested to see if this continues on the right bank.

Tomorrow we visit Nenin, Vieux Chateau Certan, Cheval Blanc, Gazin, La Couspade, Canon and Pavie. Watch this space tomorrow, for reflections on the right bank.

by Wine Owners

Posted on 2017-09-13

After a busy summer including in August our most productive trading month to date, we thought it would be instructive to run some analysis of trading trends and movements, compared to the same quarter in 2016.

Market share between regions remains relatively stable despite a large increase in trading value overall, with Bordeaux holding first place with a 75.14% share of market compared to 78.15% in the same quarter of 2016. That there is a drop is interesting in its own right, perhaps pointing to greater diversity in wines offered for sale, as well as to diversifying demand in export markets.

Burgundy is the major winner in market share, extending from 11.78% in summer 2016 to 17.10% over the same period in 2017, and we’ve certainly seen an increase in Burgundy purchases from Far East markets, showing a 17% increase on 2016 numbers by value.

Other regions remain very much minority sports, with Rhone up to 2.03% from 1.8% and Italy, surprisingly, down from 4.85% to 2.5%.

Within Bordeaux, the share of the market taken up by First Growths has grown from 28.26% in 2016 to 44.05%, perhaps reflecting heightened interest in the top wines, though the real interest is in how the First Growths compare within their own category.

Haut Brion is the major winner amongst the Firsts, increasing its share of the Bordeaux market to 13.35% from 3.2%. As a proportion of the First Growth market, the share increased from11.31% to 30.3%, putting Haut Brion at the head of the market alongside Lafite.

Lafite moved up to a 13.34% share of the Bordeaux market from 11.62%, but lost ground against the other First Growths, slipping to 30.29% from 41.12%, exchanging a clear lead in the class for an almost dead heat with the progressive Haut Brion.

Mouton showed a similar fall-off in share, dropping from an 8.63% share of Bordeaux to 7%, and a 30.54% share of the First Growth market dropping to a 15.89% share. Market and trading values for Lafite and Mouton remain robust however, so this feels more like a positive story about Haut Brion than a negative for the two Rothschild properties.

Latour has benefited too here, growing a very small share of Bordeaux (1.18%) to 5.07%, and increasing its share of the First Growth market from 4.18% to 11.05%.

Margaux has the least movement to comment on, increasing its share of the Bordeaux market marginally to 5.29% from 3.6%, and falling from 12.84% to 12.01% in its share of the First Growths.

by Wine Owners

Posted on 2017-08-08

Early afternoon 22 May 2017 word spread that Lafite was out. A few calls were made. But where was the wine? Allocations were down 50% but with the promise of another tranche in a couple of weeks’ time. Négociants waited, not wishing to be stuck with more highly priced second tranche releases.

In tandem the Chateau also attempted to revive its 2010 vintage strategy of tying other wines in the stable to allocations of Carruades and le Grand Vin. Either Rieussec and Carmes de Rieussec were being tied to Carruades, or Carruades was being tied with Duhart, or Duhart was being tied with Lafite.

As an aside, there was nothing subpar with Duhart this year, a properly serious wine in fact. But using it in a bait-and-switch move is unlikely to enhance the bait’s secondary market reputation.

Then, without waiting for the second tranche, more than one of the smaller négociants broke ranks on releasing the first tranche to customers, but estimating the cost of the second tranche and pricing at the intersect of the two. With lack of market transparency buyers were uncertain what fair value might look like.

In fact the majority of estimated intersect prices turned out to be the level of the second release price, handing merchants a handy profit of 20%, and suggesting Lafite were less aggressive with their second release pricing than they had previously signposted.

Thankfully, Lafite 2016 represents a big step up on the previous vintage, so the price increase will likely be justified in the medium term, if as expected, the secondary market adds 25% to its release price over the next few years. In fact Lafite 2016 is simply glorious: an absolute pinnacle of classicism in this great left bank vintage.

Notwithstanding, the Lafite release ‘strategy’ represents everything that is most unattractive about Bordeaux en primeur at its opaque worst.

None of which would matter, if it weren’t for the consumer. It wasn’t so long ago that the Bordeaux market was moribund: the market killed off by aggressive pricing of 2009 and 2010 vintages and a subsequent market collapse. As long as consumers end up nursing persistent losses, there is a high risk of a collapse in market confidence. Commodity-like collectible markets that wine epitomises are particularly sensitive to the maintenance of positive sentiment.

We’re certainly not back in territory as yet. Lafite 2016 released at almost 50% below that of 2010, whilst for UK buyers the collapse of Sterling has magnified price increases, whereas the strength of the US Dollar provides a tailwind for Bordeaux sales into the USA.

But the Bordelais need to be mindful of what happened following the mis-priced 2010 release. Lest we forget, it was barely 3 years ago that the Bordeaux secondary market was still in the doldrums. The remarkable market resurgence that started in late 2014 should not be taken for granted. The Chateaux have a profound responsibility to avoid the Dory Syndrome, named after the forgetful fish in the Disney film animation.

by Wine Owners

Posted on 2017-05-23

Early afternoon 22nd May word spread that Lafite was out. A few calls were made. But where was the wine? Allocations were down 50% but with the promise of another allocation in a week’s time at a premium of between 30%-40%. No prices, no offers.

Then, more than one of the smaller négociants decided to pull the trigger on releasing the première tranche, but estimating the cost of the second tranche and pricing at the intersect of the two. Perhaps guessing they were unlikely to get any more and taking attractive profits on the first tranche.

In UK terms the averaged, intersect price is £480 a bottle, which puts the first release at around £384 a bottle whilst the second release could be in the range £540-£575.

That compares to the 2015 release price of £358 per bottle, which in turn leads us to the conclusion that in euro terms the first tranche release price is likely to have been more or less flat year on year. But of course, we can’t be sure.

The rest of the supply chain is sitting tight. The majority of Lafite offers won’t now reach your inbox for another week. The channels of distribution are showing admirable sense and fair play in averaging the two release prices and treating their customers with the egalité most deserve.

So how about the wine? Lafite 2016 is glorious: one of a handful of wines that stand imperiously; pinnacles in this truly great left bank vintage. Is it worth £480 a bottle? A difficult question to answer, but surprisingly, it does look like acceptable value in the context of current market prices of prior excellent or great vintages.

Below is our relative value analysis. Based on our estimations of what’s likely to happen in the next week, 2016 is showing a small advantage over prior vintages. If you consider that 2009 and 2010 are well off their lows, and that the absolute low of Lafite 2010 was £446 a bottle, it indicates that 2016 has very limited downside, and might well run up to around £600 a bottle over the next 3 years.

Once selling commission of 5% inclusive is taken into account and an adjustment for storage fees, your net proceeds would be £567, or a return of £87 a bottle: a return or discount to future market value (depending on your perspective) of 15%. Based on the above illustration an en primeur purchaser will be therefore looking at growth averaging 5% per annum.

It’s tight. There’ll be buyers. Notwithstanding, if the averaged price per bottle shakes out around £450-£460 many more collectors would swing behind it.

by Wine Owners

Posted on 2016-03-14

OWNER

Chateau Lafite Rothschild

APPELLATION

Pauillac

BLEND

Bordeaux Red

AVERAGE SCORE

95 points

REVIEW

Intense crimson. Nose offresh, ripe black fruit, elegant oak. Fullness is a key theme on the palate,concentration, fine grain, power, finesse. Remarkable.

(Gilbert & Gaillard, 2010)

VIEW THE FULL PROFILE

by Wine Owners

Posted on 2015-10-29

Quite a lot of members we speak to these days assume that the market prices of Bordeaux are still stagnating or falling. The morosité that had descended on the region's finest wines in by 2012 does not appear to have lifted.

Wine traders will point to volumes that are much reduced since the giddy heyday of 2009-2011, and that is of course true.

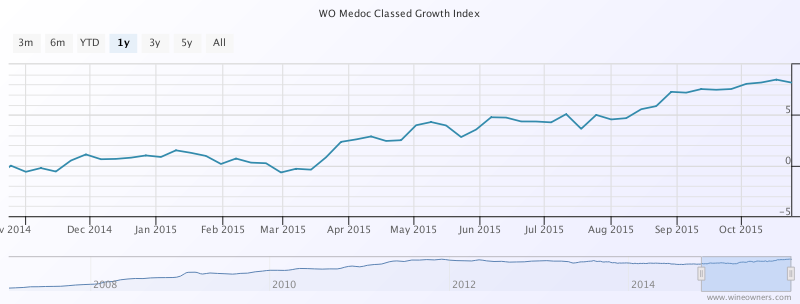

However, it does not mean that in aggregate, prices of Bordeaux have begun an upward trend. In the last year, the Wine Owners Medoc Classed Growth Index is up 8.2%.

Whereas the Wine Owners First Growth Index has only managed half of that in the last year, up 4.1%.

That's still better than the performance of the FTSE100, which is fractionally underwater over the last year, and exactly where the S&P500 has clawed it's way back to after the summer's wobbles.

Wine Owners 150 = Turquoise

FTSE100 = Navy

S&P500 - Green

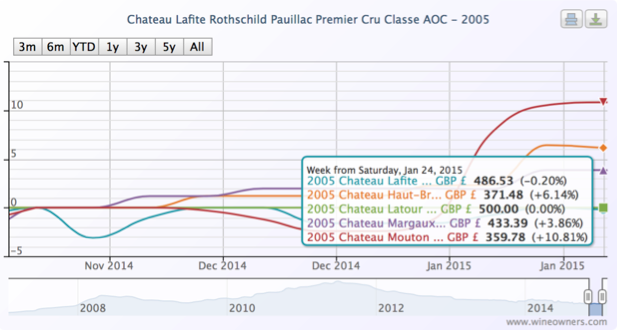

However, when looking at First Growth performance over the last 12 months, it is far from broad-based. 'The further they rise, the longer they fall' seems to hold true, with Lafite 1986 and 1989 performing the worst at -8% and -9% respectively.

| Chateau Haut-Brion Pessac-Leognan Premier Cru Classe AOP | 1999 | -5.45% | £ 216.68 |

| Chateau Latour Pauillac Premier Cru Classe AOP | 2006 | -5.75% | £ 286.67 |

| Chateau Haut-Brion Pessac-Leognan Premier Cru Classe AOP | 2009 | -5.82% | £ 441.67 |

| Chateau Haut-Brion Pessac-Leognan Premier Cru Classe AOP | 1982 | -5.92% | £ 436.68 |

| Chateau Lafite Rothschild Pauillac Premier Cru Classe AOP | 1982 | -6.29% | £ 1,810.14 |

| Chateau Latour Pauillac Premier Cru Classe AOP | 1998 | -7.15% | £ 270.83 |

| Chateau Haut-Brion Pessac-Leognan Premier Cru Classe AOP | 2006 | -7.26% | £ 212.50 |

| Chateau Margaux Premier Cru Classe AOP | 1989 | -7.59% | £ 250.10 |

| Chateau Lafite Rothschild Pauillac Premier Cru Classe AOP | 1986 | -8.13% | £ 651.48 |

| Chateau Lafite Rothschild Pauillac Premier Cru Classe AOP | 1989 | -9.11% | £ 395.92 |

Among the vintages populating negative territory, 1986 has suffered with the exception of the very great Mouton. The exceptional 1989s and 1990s have fallen, along with with the dull 1999s.

The risers are headed by Mouton, Haut Brion and Latour. The top 10 performers registering double digit growth are entirely accounted for by these three Châteaux.

| Wine | Vintage | Change 1 year | Price |

|---|

| Chateau Mouton Rothschild Pauillac Premier Cru Classe AOP | 2005 | 22.39% | £ 366.67 |

| Chateau Mouton Rothschild Pauillac Premier Cru Classe AOP | 2008 | 21.13% | £ 262.54 |

| Chateau Haut-Brion Pessac-Leognan Premier Cru Classe AOP | 2005 | 20.95% | £ 437.50 |

| Chateau Mouton Rothschild Pauillac Premier Cru Classe AOP | 1996 | 16.87% | £ 282.74 |

| Chateau Latour Pauillac Premier Cru Classe AOP | 1990 | 14.30% | £ 429.12 |

| Chateau Latour Pauillac Premier Cru Classe AOP | 2005 | 13.36% | £ 566.79 |

| Chateau Mouton Rothschild Pauillac Premier Cru Classe AOP | 2000 | 13.32% | £ 1,038.81 |

| Chateau Haut-Brion Pessac-Leognan Premier Cru Classe AOP | 2008 | 11.00% | £ 226.64 |

| Chateau Haut-Brion Pessac-Leognan Premier Cru Classe AOP | 1989 | 9.08% | £ 1,000.03 |

| Chateau Latour Pauillac Premier Cru Classe AOP | 1995 | 8.49% | £ 316.67 |

Crossing over to the right bank, predominant top performers over the last 12 months are St EmillMedoc Classed Growth Indexon 2005s and the 2001 Class A relative newcomers. Since March 2015 The Wine Owners Libournais Index is up 7%, coming off it's 3 year lows at that point.

| Chateau Angelus Saint Emilion Premier Grand Cru Classe A AOP | 2005 | 53.85% | £ 300.00 |

| Chateau Angelus Saint Emilion Premier Grand Cru Classe A AOP | 2001 | 48.07% | £ 176.57 |

| Chateau Pavie Saint Emilion Premier Grand Cru Classe A AOP | 2001 | 45.67% | £ 183.46 |

| Chateau Angelus Saint Emilion Premier Grand Cru Classe A AOP | 2000 | 37.16% | £ 301.79 |

| Chateau Pavie Saint Emilion Premier Grand Cru Classe A AOP | 1998 | 34.59% | £ 161.84 |

| Chateau Larcis Ducasse Saint Emilion Premier Grand Cru Classe B AOP | 2005 | 27.82% | £ 110.96 |

| Chateau Pavie Saint Emilion Premier Grand Cru Classe A AOP | 2005 | 26.84% | £ 232.57 |

| Chateau La Violette Pomerol AOP | 2009 | 26.67% | £ 208.33 |

| Chateau Cheval Blanc Saint-Emilion Premier Grand Cru Classe A AOP | 2005 | 24.71% | £ 433.34 |

What can we conclude from this? Some commentators are suggesting that value is returning to older back vintages on the back of 4 year declines. Relative value vs quality is likely to be a key driver of future value, for which we recommend you check out the new price per points builder on Wine Owners to which you'll need to subscribe.

Liv-ex have recently seen a predominance of trades of the 2010 vintage, and whilst there seems to be value returning selectively to the Classed Growths, one wonders if it's a little early yet the First Growths, whose starting release prices were in nose-bleed territory. Since 'the further they rise, the longer they fall' it may yet be a bit early to call.

by Wine Owners

Posted on 2015-06-10

Jane Anson’s insight into what courtiers and négoces think about the en primeur system makes for very interesting reading.

Perhaps what many Chateaux are unwilling to go on record with is the question of estate value.

Land values are at least partially driven by the cost per bottle that can be achieved by the Chateaux at the point of release. The higher the release price (whenever that is) the higher the cost of land per hectare.

If you've just blown €200M on a slice of prime classed growth real estate, you want to support the underlying assumptions upon which that price was predicated. The balance sheet value of that asset and its ability to appreciate over time (and not see shareholder value diminished) becomes pretty crucial.

Is this one of the reasons why Calon released so little and massively cut back on the number of Négoces they allowed allocations, narrowing channels to market?

We totally agree with Jane Anson that a number of the First Growths got their pricing right. For me Lafite at first tranche and Mouton (Grand and Petit) got it most right vs market pricing of back vintages. There is future value in those purchases.

The sooner the 'funding' model of EP is clarified, the sooner the negativity surrounding the EP release period will evaporate. I think consumers dislike conflicting messaging and behaviour as much as channels of distribution do.

Let's say it; the top Chateaux (the only part of the EP market that appears to be worth bothering with) don't need us to fund the next vintage. Nor therefore do they have a need to leave enough on the table to convince us of the opportunity-cost of stockholding for them. That illusion is about to be shattered.

by Wine Owners

Posted on 2015-05-27

So goes the good luck saying, advising what a bride might wear at her wedding to bring good fortune.

In reviewing Bordeaux 2014 releases to date what could be more appropriate? After all, this has been a campaign where a few enlightened producers got their winemaking and pricing aligned, whilst others (the majority?) have simply ignored the current compelling pricing of many of their back vintages of comparable quality.

In the light of that, what mixture of old and new vintages might the wine lover or collector consider?

SOMETHING OLD

Something old is symbolic of continuity.

When comparing the 2014s to broadly comparable back vintages, it reaffirms the value there is in wines around the 7-12 year old mark. In the majority of cases these are wines just hitting their stride, and in some cases with enormous drinking windows ahead of them.

Here are some examples but today Bordeaux unquestionably is generally favouring back vintages over new releases.

L’Eglise Clinet 2006

I just love L’Eglise Clinet, so I’m delighted to give it my first mention. Only, why buy 2014 when 2004, 2006 and 2008 are all cheaper? Personally I’d probably pay the market premium for the 2006, simply because that vintage is proving to be such a fine year in Pomerol. There is so much definition to the fruit, and such balance to the best wines. L’Eglise Clinet is an obvious choice due to winemaking of the highest order over the last decade.

Haut Brion 2008

At around £2,400 per case, the 2008 makes a profoundly compelling case for itself, as does the 2012 in the light of its recent Parker rerating, reinforced by other reviewers such as Jeff Leve. Throw 2006 into the mix as a wine of exceptional purity, and there’s an embarasse de richesses for grown up lovers of Graves.

Palmer 2004

Leaving aside the fact that the beautiful 2014 is Palmer’s first vintage made entirely biodynamically, 2004 still stands out as a wine value that warrants the wine lover’s attention. According to Parker it’s a modern day version of Palmer’s brilliant 1966, majoring on elegance and precision, freshness and depth of flavor.

SOMETHING NEW

Represents good luck, success and hopes for a bright future.

Let’s start with a handful of winners. Using the soon to be released price per points analysis feature on Wine Owners highlights value in the context of broadly comparable quality. The teetering Euro helped, creating a rare opportunity for Châteaux to please the market and satisfy their accountants. A handful grasped the opportunity.

Le Petit Mouton 2014

Growing positive sentiment in respect of the quality of the last decade’s vintages has given those years a recent helping hand. This is the cheapest vintage in the market at £375, and a 40% discount to its possible qualitative equal – 2006. Different too. The success of Merlot on gravel relegated a big slug of Cabernet to the second wine, so atypically cabernet-dominated and correspondingly serious.

Mouton Rothschild 2014

Outstanding in a vintage in which Pauillac starred. There’s a breezy balance whilst its Merlot genes and dash of Cabernet Franc complete a raspberry-driven, fresh, complex palate with plenty of fine-grained tannins. They got the price right as the charts show.

Lynch Bages 2014

Poised, with classic Pauillac character; loaded with griottes fruit and flowing Saville Row lines. It was priced to within a hairs-breadth of 2011 and 2012 current market value but the value difference over 2008 and 2006 must have convinced loyal buyers to part with their money early as merchants reported healthy demand.

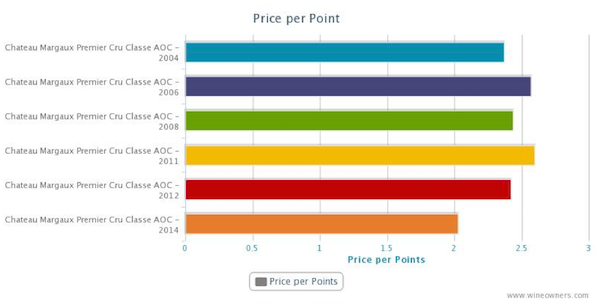

Lafite 2014

We didn’t think Lafite was the most immediately impressive First Growth in 2014. In fact it seemed to be the most obdurate. Yet the critics lapped it up, and we’re more than happy to defer to their better judgement. In the meantime one thing is very, very obvious looking at the price per points analysis. It’s priced as a come-on to consumers to open their pocket books and buy early.

SOMETHING BORROWED

Anything can be borrowed but it must be returned afterwards.

A couple of worrying features of the 2014 campaign have emerged.

The first is linkage. Back in 2010 Bordeaux chose to tie certain wines with others. The most interesting example was a pack of Rieussec linked to a pack of Carruades. Interesting because of the distorting factor it had on the market for Rieussec. Back then, merchants simply added a couple of hundred pounds to the price of their Carruades allocation before dumping Rieussec onto Livex and selling through at £210-£220 per 12; roughly half the retail release price offered to consumers. To this day those Livex members who jumped in and hoovered up stock are sitting on the best returns that the 2010 vintage had to offer. Not great for the consumer who bought Carruades but a creative market response to price manipulation.

Linkage is seemingly back, with Rieussec once again tied to Carruades, according to one or two merchants we talked to. Who’s doing the tying is a question to which I have no answer, and this time the merchants can’t just transfer pricing from one wine (relatively difficult to sell at first release) to another (for which there was unquenchable demand back in 2010).

The second feature is limited quantities released by some Châteaux. Who’d have thought the Bordelais would have de facto discouraged early purchases in 2014 – maybe they don’t believe in the en primeur system after all? Like a boyfriend who isn’t in love anymore, but is too insecure to let his partner go.

Calon-Ségur is a wine I thought showed delightfully in 2014. The vibe among négociants in Bordeaux was positive, lending emotional support to the wine even before release.

Recently acquired by Suravenir Assurance, an insurance company for whom no doubt a higher average release price per bottle will help to sûr-value their estate on a forward-looking basis, chose to release up but at a realistic price point for the fine quality. But then the real game plan became apparent. There was no wine: merchants who had assumed they were in line for a reasonable allocation (and had promised private clients allocations on that basis) found that they were empty handed. Merchants were left scurrying around for whatever they could pick up. Consumers were left feeling that however big Calon’s heart, maybe it was losing its soul.

This is the sort of attempt at market influence that Bordeaux EP does not need. Frankly, if Châteaux would prefer to achieve a higher price than the market can bear, then why not exit EP as Latour did, and release when the wine is considered ready? It’s dishonest to play it both ways and the market will not necessarily reward throttled supply with higher prices: demand is often chocked off too in the process.

SOMETHING BLUE

The symbol of faithfulness, purity and loyalty.

There are so many Châteaux that we could have used to exemplify the question of whether we would have chosen to buy early, or wait a few years until the young wines are fully formed, or go back to earlier vintages where there’s so much value to be had. In most (but by no means all) cases we’d go back to earlier vintages and wait to buy the new releases in bottle. But buying young wine isn’t an entirely rational decision as we all know.

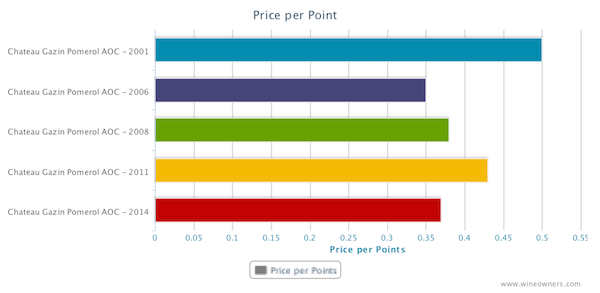

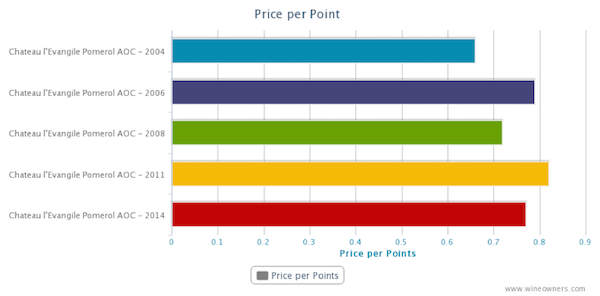

Which vintages would you buy on the basis of the following charts? You decide!

by Wine Owners

Posted on 2015-02-16

The turning point for fine Bordeaux was August of last year. By early October it was unclear whether the tick-up was yet another of those blips we’d seen several of during the previous 24 months.

Today it is clearer: the trend is up, most wines are well off their lows, and the Bordeaux Index overall is 2.17% up on 6 months ago.

The exception is the Libournais index covering Pomerol and St Emilion, which has slipped 0.48%, a reversing the gains of 1.24% between early October and the end of November last year.

The Medoc Classed Growths are collectively up 2.77% form their August 9th 2014 lows.

Whereas the First Growths only managed 1.51% during the same period. Not entirely surprising since top vintages are still highly priced, they have had further to fall, making it hard to call bottom, and started picking up momentum in January 2015. What is clearer is that wines such as Haut Brion 2008 appear to be interesting propositions.

Elsewhere the Blue Chip Burgundy Index continues to power ahead, though within that there are notable, and expensive, fallers (last 12 months):

| Domaine de la Romanee-Conti Le Montrachet Grand Cru AOC |

2010 |

-7.16 |

| Domaine Ponsot Charmes Chambertin Cuvee des Merles Grand Cru AOP |

2010 |

-7.69 |

| Domaine Armand Rousseau Mazis-Chambertin Grand Cru AOC |

2010 |

-7.89 |

| Domaine Jean Grivot Richebourg Grand Cru AOC |

2007 |

-9.43 |

| Domaine de la Romanee-Conti Romanee Saint Vivant Grand Cru AOC |

2010 |

-10.71 |

| Domaine Jean Grivot Echezeaux Grand Cru AOC |

2002 |

-11.2 |

| Domaine Leflaive Batard-Montrachet Grand Cru AOC |

2006 |

-13.15 |

| Sylvain Cathiard Vosne Romanee En Orveaux Premier Cru AOC |

2010 |

-13.69 |

| Domaine Comte Georges de Vogue Chambolle Musigny Les Amoureuses Premier Cru AOC |

2002 |

-13.7 |

| Domaine de la Romanee-Conti La Tache Monopole Grand Cru AOC |

2010 |

-15.38 |

| Domaine Armand Rousseau Clos de la Roche Grand Cru AOC |

2010 |

-16.08 |

| Domaine Leflaive Batard-Montrachet Grand Cru AOC |

2005 |

-16.18 |

| Domaine Jean-Francois Coche-Dury Corton-Charlemagne Grand Cru AOC |

2006 |

-16.35 |

| Domaine Leflaive Chevalier-Montrachet Grand Cru AOC |

2005 |

-16.67 |

| Domaine Leflaive Le Montrachet Grand Cru AOC |

2008 |

-20 |

| Domaine Leflaive Le Montrachet Grand Cru AOC |

2006 |

-20.16 |

| Domaine Leflaive Le Montrachet Grand Cru AOC |

2005 |

-21.94 |

Northern Italy is up 1.42%, with Giacomo Conterno one again heading the leaderboard

Champagne has defied our predictions in gaining a whopping 7.42% over the last 6 months, the top risers comprising exclusively older vintages in the range 1996-2002. This makes a lot of sense. Millions of bottles of top cuvees such as Dom Perignon (up to 8M bottles per annum) means that values kick up only when supply and demand becomes more balanced.

We also thought Californian wines would moderate their growth this year. Comparative to Bordeaux prices, they seem expensive. Since January they have indeed dipped -0.65%, off the back of six month growth of 6.65% up until that point. It’s too early to say whether they are simply pausing for breath, or have reached a natural plateau. The trend line favours the first scenario.