by Wine Owners

Posted on 2017-09-13

After a busy summer including in August our most productive trading month to date, we thought it would be instructive to run some analysis of trading trends and movements, compared to the same quarter in 2016.

Market share between regions remains relatively stable despite a large increase in trading value overall, with Bordeaux holding first place with a 75.14% share of market compared to 78.15% in the same quarter of 2016. That there is a drop is interesting in its own right, perhaps pointing to greater diversity in wines offered for sale, as well as to diversifying demand in export markets.

Burgundy is the major winner in market share, extending from 11.78% in summer 2016 to 17.10% over the same period in 2017, and we’ve certainly seen an increase in Burgundy purchases from Far East markets, showing a 17% increase on 2016 numbers by value.

Other regions remain very much minority sports, with Rhone up to 2.03% from 1.8% and Italy, surprisingly, down from 4.85% to 2.5%.

Within Bordeaux, the share of the market taken up by First Growths has grown from 28.26% in 2016 to 44.05%, perhaps reflecting heightened interest in the top wines, though the real interest is in how the First Growths compare within their own category.

Haut Brion is the major winner amongst the Firsts, increasing its share of the Bordeaux market to 13.35% from 3.2%. As a proportion of the First Growth market, the share increased from11.31% to 30.3%, putting Haut Brion at the head of the market alongside Lafite.

Lafite moved up to a 13.34% share of the Bordeaux market from 11.62%, but lost ground against the other First Growths, slipping to 30.29% from 41.12%, exchanging a clear lead in the class for an almost dead heat with the progressive Haut Brion.

Mouton showed a similar fall-off in share, dropping from an 8.63% share of Bordeaux to 7%, and a 30.54% share of the First Growth market dropping to a 15.89% share. Market and trading values for Lafite and Mouton remain robust however, so this feels more like a positive story about Haut Brion than a negative for the two Rothschild properties.

Latour has benefited too here, growing a very small share of Bordeaux (1.18%) to 5.07%, and increasing its share of the First Growth market from 4.18% to 11.05%.

Margaux has the least movement to comment on, increasing its share of the Bordeaux market marginally to 5.29% from 3.6%, and falling from 12.84% to 12.01% in its share of the First Growths.

by Wine Owners

Posted on 2017-03-22

Few producers ever achieve the magical 100 point rating from the Wine Advocate. Parker’s ratings have been the most influential in the world, so to achieve the magic century is quite some accolade; to achieve it more than once is the stuff of dreams; to achieve it 28 times as have Guigal’s famed Cote Rotie triumvirate of La Landonne, La Turque and La Mouline (collectively nicknamed ‘the La Las’) is unprecedented. No other producer from a single appellation comes close.

You might have thought that these three wine with a claim to be among the finest in the world should cost the earth, shouldn’t they? Well, in fact they don’t – at least not in comparison with the finest wines of Bordeaux, Burgundy and California.

For the purposes of this analysis we’re going to look at the 2009 vintage, which paints a fairly typical picture for these wines. Historically there is very little variation in the values of the three wines, with prices often within a 3% range. So, this chart for La Mouline ’09 is mirrored closely by the other two. What is immediately noticeable is that prices have, until midway through last year, fallen consistently. This despite two 100 point scores in November 2013 and September 2014!

The fall in price is on a par with the falls in value of Bordeaux wines in the same period, but importantly the La Las did not have a huge price rise immediately prior to the falls that insulated many buyers from the slump. It seems, on the face of it that Guigal’s amazing wines were simply the victim of a lack of global interest in Rhone wines at the top end.

This seems to be changing however, as over the last 6 to 9 months the relatively attractive pricing has found favour, and sentiment seems to have turned positive. All good vintages across all three wines are moving upwards, and demand is out-stripping supply for the first time in many years.

La Mouline 09 is 15% up since July, and is on its way back to the £4000 a case level last seen in early 2013. In our view there is reason* to be confident that this recovery is a fundamental re-evaluation of the value of the wine, rather than simply the beneficial effect of weak Sterling, and there is definitely reason* to add this to a cellar, for both investment and drinking purposes.

So, what is this reason you may well ask?

Sadly, the La La’s were among the chosen wines of various boiler room, sales led operations who decided that they were ideal wines to sell as investments to unsuspecting investors at way over fair market prices. This created skewed pricing and led to reputational damage to the wines that caused prices to drop. Thankfully most of these operations have now closed down, and their negative impact on the market has dissipated. The secondary market is now a healthier place for these great wines, and prices are once again reflecting the supreme quality and longevity of Rhone’s finest.

by Wine Owners

Posted on 2016-06-10

There’s a clear division between 2015 En Primeur releases before Vinexpo Hong Hong and those that have been announced since. It begs the question, why?

It's not just that the bigger Chateaux are the ones releasing later. After all, many important names had released well beforehand.

The answer is what happened whilst the producers were in Hong Kong.

We understand that producers were taken aback by the demand they experienced this year at Vinexpo, and they boarded the flight home with bulging order books.

For every producer who wants to sell the new wines through En Primeur and recognises the importance of providing a future upside for buyers of non-physical stock, there are others who see a new opportunity within the changing global fine wine market.

Bernard Magrez was full of the joys of spring at Vinexpo Hong Kong, confirming he had sold out of his impressive Chateau Pape Clement in 40 minutes.

He was refreshing in his analysis, saying that he knew he’d left money on the table for the merchant and En Primeur buyer, which he saw as a positive for the property’s burgeoning reputation. Surely if you’re going to be part of En Primeur that’s the way to do it: body and soul.

Many others however have been eyeing life after En Primeur for some time, but have held back from backing one horse or another by the generally morose market conditions. With green shoots appearing over the last 12 months, few were in the mood to risk seeing them wither.

But what they experienced at Vinexpo may have shifted the balance further away from genuine, tangible broad-based support for En Primeur.

The Chateaux owners were surprised by the jump in orders experienced for their back vintages. There was a realisation that the wine market in China was coming back after 4 years of austerity and Party approbation.

The politics seem to be loosening up a touch, the consumer is spending again and contributing strongly to GDP growth, imports of luxury goods are steady (and proportionately performing better than exports).

Not that the Chinese buy En Primeur, there’s still almost no market there for it there, but with physical stocks in Bordeaux being soaked up by a sharp uptick in demand, it’s hardly surprising many producers are choosing to hold onto significantly more of the new vintage, so that they can serve the Asian market further down the line.

What a relief it must be to see all those accumulated bottles sell.

If it’s all heading towards producers being the stockholders and focusing on selling back vintages at premium prices, the one thing I’d say to them is, don't confuse the issue by using the En Primeur system as purely a promotional opportunity in the marketing calendar to get press and attention, if you don't care so much if any actually sells. It creates mixed messages.

I am super-impressed by what Palmer are doing in terms of developing sales channels worldwide, focusing on selling physical stock, staging stunning auctions through their negociant shareholder, creating a brand to rival the Firsts - but the En Primeur thing just muddies the water and undermines the brilliance of everything else.

If the recent Sotheby’s auction of Chateau Palmer in Hong Kong points the way to selling En Primeur by the barrel to high rollers with privileged access thrown in, I would surely go down that route as a producer too. The equivalent of £10,800 per 9 litres (12x75cl) before seller commission is simply amazing if you can get it.

“Chapeau”. I raise my hat to the Chateaux who go the full-on brand-building route and do it this well - but why risk the negative sentiment and comments that a perceptually very high En Primeur release price creates? There are simply too many foreseeable consequences: negative comments (mea culpa); anxious merchant emails to clients warning them off; negociants dropping prices during the course of the same day the release happens in a mildly desperate attempt not to be left with expensive stock that might/ will have to be written down; and static or lower secondary market prices that will make consumer buyers feel negative about the brand due to being under water ‘x’ years down the line.

With Asian appetite for Bordeaux on the rise once again, the moment may have arrived when more and more producers will respond to the shift in demand for primary market releases of back vintages by backing the new horse. It’s a complicated decision with a brew of old allegiances, dependent market structures, local friends, brand building, rising land values and a changing global market. Watch this space.

by Wine Owners

Posted on 2016-03-24

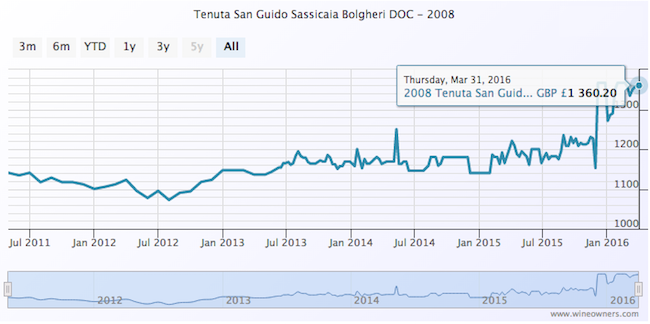

OWNER

OWNER

Tenuta San Guido

APPELLATION

Bolgheri

BLEND

85% Cabernet Sauvignon, 15% Cabernet Franc

AVERAGE SCORE

94/100

REVIEW

The 2008 Sassicaia is a rich, deep wine imbued with notable class in its black cherries, plums, grilled herbs, minerals and smoke. The 2008 is a decidedly buttoned-up, firm Sassicaia that is currently holding back much of its potential, unlike the 2006 and 2007, both of which were far more obvious wines. Readers who can afford to wait will be treated to a sublime wine once this settles down in bottle. Muscular, firm tannins frame the exquisite finish in this dark, implosive Sassicaia. The 2008 Sassicaia is 85% Cabernet Sauvignon and 15% Cabernet Franc. The wine spent 24 months in French oak barrels. Anticipated maturity: 2018-2038. Tenuta San Guido is on a roll these days. Over the last few years, the estate has released a number of hugely delicious wines. These new releases are nicely aligned with their respective vintages. The entry-level Le Difese and Guidalberto both capture the essence of a sunny year that made wines well suited to near-term drinking, while the 2008 Sassicaia captures the potential of a powerful vintage characterized by low yields and a late harvest. (Robert Parker, 2011).

by Wine Owners

Posted on 2016-03-24

Sales of Bordeaux through the

exchange saw a significant increase on the preceding month, rising from a 75%

share of the market to 88%, the highest market share since the launch of the

exchange in 2013. Bids overall in Bordeaux have increased in value by 2

percentage points, perhaps reflecting a slight upturn in confidence in the

market.

The steep rise in Bordeaux’s market

share overshadows other regions, pushing Burgundy right back to 5%, though the

figure reflects less a decline for Burgundy than the strengthening of the

market in Bordeaux. Volume and value traded were in fact similar to the

preceding period. Rhone had a poor showing overall, dropping market share to

1.3%. Again, the figure is skewed by Bordeaux, but in any case volumes were

down, mitigated only by a flurry of interest in Henri Bonneau triggered by the

announcement of his death on Wednesday. The remainder of the market was shared

almost equally between Champagne and Italy, where trading in top level Barolo

oustripped Supertuscans two to one.

As usual, the First Growths accounted

for the lion’s share of the Bordeaux market, 72% of the value of Bordeaux

trades were made up of 1ers crus and their right bank equivalents. Several

large trades in Haut Brion saw that wine take 61% of the value of 1st

growth trades, though Mouton continued to hold its own at 11.7%, down by

percentage on the preceding period, but up in overall value and volume. Lafite

remained strong at 5.8%, with Latour and Margaux lagging behind. Petrus showed

strongly too, picking up a share of 11% among the 1st growths,

though the high value of these wines always has a tendency to distort market

share by value.

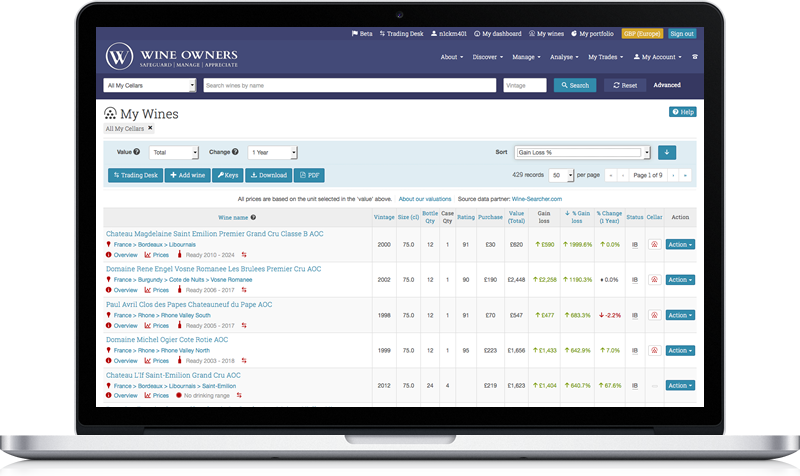

Access the Trading Desk to view recent trades, bids & offers.

by Wine Owners

Posted on 2016-03-23

With the base price taken on January 2008, the WO Bordeaux Index has significantly outperformed the Dow Jones Index, peaking at 147.33% as of 17 March, 2016, dwarfing Dow Jones' seemingly modest gains of 40.40%. With growing demand for Bordeaux market within the Asian market, such inflation in prices is undoubtedly set to increase. The WO Bordeaux Index's ability to weather through financial instability is also illustrated in its appreciation in the midst of the 2008-2009 financial crisis, obtaining a 74.73% increase compared to Dow Jones' depreciation of 43.60%.

Note: The Dow Jones Industrial index (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq.

by Wine Owners

Posted on 2016-03-22

Undoubtedly, the market potential for wine producers and trading platforms is set to growth, the number of wealthy households in China expected to expand at an annual rate of around 16% for the next 5-7 years. Moreover, there has been high increases in Chinese internet penetration with an increase of 31 million new Internet users in 2015 (reaching a total of 649 million). Such a catalysis, together with general perception of foreign brands being of superior quality (i.e. Burgundy, Bordeaux markets) has hence led to strong import dependence of the Chinese, Japanese and Korean markets, with consumers importing as much as 96-100% of their wines.

However, wine producers must recognise that expansion into Asia, specifically China would face several restrictions with Xi JingPing's government-initiated austerity drive and anti-corruption drive hampering the premium wine market for gifting and banqueting. Hence, firm compliance with central authorities are imperative for the business to thrive. Furthermore, with China's economy growing at a rapid rate of around 6-7% (2016 predictions), China's economy has become multi-dimensional, facing transition challenges as the structure adapts to various economic and market reforms implemented by the central authorities.

by Wine Owners

Posted on 2016-03-16

OWNER

OWNER

Domaine Jean-Francois Coche-Dury

APPELLATION

Corton-Charlemagne

BLEND

Chardonnay

AVERAGE SCORE

95/100

REVIEW

Black tea, pugent herbs, iris, narcissus, and an alkaline, saline note suggestive of ocean breezes greet the nose. On the palate, this grips with penetrating pungency and tactile stoniness, leaving behind a memorable concentrate of chalk, salts, faintly bitter herbal essences, along with marrow and animal bone reduction. Surely it will go on to further glory in the bottle and should reward 15 or more years' cellaring. (Robert Parker, 2008)

SEE FULL PROFILE

by Wine Owners

Posted on 2016-03-14

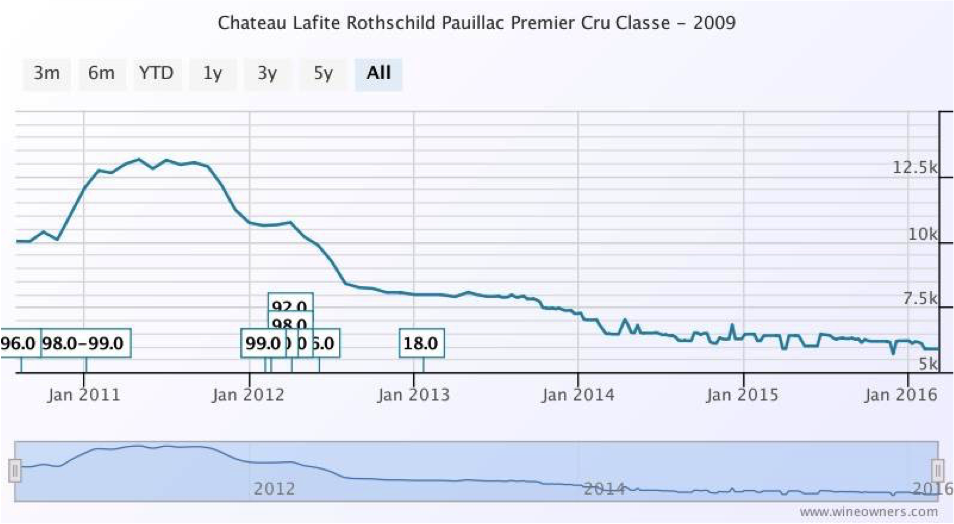

OWNER

Chateau Lafite Rothschild

APPELLATION

Pauillac

BLEND

Bordeaux Red

AVERAGE SCORE

95 points

REVIEW

Intense crimson. Nose offresh, ripe black fruit, elegant oak. Fullness is a key theme on the palate,concentration, fine grain, power, finesse. Remarkable.

(Gilbert & Gaillard, 2010)

VIEW THE FULL PROFILE

by Wine Owners

Posted on 2016-03-03

OWNER

Chateau Haut-Brion

APPELLATION

Pessac-Leognan

BLEND

Bordeaux Red Blend

AVERAGE SCORE

98/100

Haut-Brion 2005 initially enjoyed strong growth, peaking at £7,300 on the 30th September, 2008, ever since then however, the market value has dropped, reaching a trough of £4,561 in Jan 31, 2013. The price has plateaued to around its current value with little room for potential growth.

REVIEW

Another profound effort from Haut-Brion, the 2005 (a 9,000-case blend of 56% Cabernet Sauvignon, 39% Merlot, and the rest Cabernet Franc) has bulked up to the point that it is fair to compare it to the great successes of 1989, 1990, 1995, 1996, 1998, and 2000. A dark ruby/purple color is followed by a nuanced, noble bouquet of blue and red fruits interwoven with wet stones, unsmoked cigar tobacco, scorched earth, and spring flowers. The wine is full-bodied, pure, and complex as well as exceptionally elegant with laser-like precision. (Robert Parker, April 2008)