by Wine Owners

Posted on 2022-10-13

Today the wine part of the Wine Owners team, as opposed to the tech team who provide our best-in-class software solutions, tasted wines from one of the great sub-sections of the Union of Grand Crus; it is called the Bordeaux Grands Crus Classés - to avoid confusion!

Wines offered came from 2018-2021 vintages. What was abundantly clear was that 2019 has reconfirmed itself as the best of modern vintages. Also, 2018 is not for the faint hearted, especially Montrose, and also that second wines offer a lot of drinking pleasure at a diddly squat fraction of grand vin prices. La Dame de Montrose excelled, as did La Croix de Canon. The unpronounceable Chateau d’Aiguilhe from the Cotes de Castillon performed well, as usual (apart from the ’21), and at £150 per 12 in bond for the 2019 is remarkable value. Chateau Canon reinforced its ‘polished’ status and was probably the most consistent.

There were some volatile samples of ‘21s, which we imagine not to be representative.

To my mind, the question is not what to buy but when to buy, if you haven’t already - 2019 should be in everybody’s cellars.

Chateaux represented:

Smith Haut Lafitte

Gazin

Vignobles Comtes Von Niepperg - d’Aiguilhe, Clos de l’Oratoire, Canon La Gaffeliere, La Mondotte

Canon

Rauzan Segla

Branaire Ducru

Pontet Canet

Montrose

Guiraud

For enormous pleasure and for a twist on sweet wines, readers should definitely embrace the current trend of lighter wines from the region. Fresher and less sweet wines from Sauternes were particularly well represented by the second wines of Chateau Guiraud and these will make a very stylish aperitif. The dry whites of Smith Haut Lafitte were superb, and are so often overlooked for more obvious alternatives, Burgundy normally, as are most dry white Bordeaux wines - in the U.K. at least.

Miles Davis October 11th 2022

by Wine Owners

Posted on 2021-11-22

For a couple of days at least the world felt normal again as the English wine trade returned en masse to Burgundy for the first time in two years. How wonderful it was to be back was the most prevalent sentiment and ‘ooh, aren’t the wines good’ the most repeated phrase. The Burgundians are a little more patient than their counterparts from Bordeaux and wait for a little over a year, as opposed to a few months, after harvest to show their wines to the world, making en primeur tastings that much more informative, and pleasant, so here’s a quick review of Burgundy 2020.

2020 was another very warm and dry year but the range in temperatures between night and day and the ongoing improvement and knowledge of how to handle the heat meant the vintage is a good one, a very good one. The whole winemaking process is more scientific and exacting than ever before and the attention to detail demonstrated by some winemakers is incredible. Whether it is more work in the vineyard, including the lighting of candles in the vineyards at four o’clock in the morning to stave off potential frost (or not as it turned out for Cyprien Arlaud of the eponymous domain in spring this year), harvesting earlier, new technology and/or machinery including a million-euro bottle washer machine (at Domaine Lorenzon in Mercurey), or organic or even bio dynamic farming these guys are giving themselves every chance of making great wine whatever mother nature throws their way. It was noticeable that bio dynamic farmers reported less loss of crop due to frost than others as their plants are healthier – at least that is what they say! Another technique favoured by some to avoid frost damage is to prune closer to springtime whereas traditionally pruning of the vines took place in November. This means they can control budding more closely and not leave the new buds exposed for longer. This has helped some growers enormously.

The devastating frosts of earlier this year (2021), particularly for Chardonnay, will be discussed repeatedly during the impending 2020 campaign in January, as growers will be factoring their lack of supply for next year into prices for this. Apart from the odd pause for breath Burgundy prices have been on the rise significantly for well over a decade now and there is no reason to suggest this will cease anytime soon.

There is just something very special about Burgundy; it appears there are just more aficionados plugged into this region than any other. Perhaps it is because it offers so many world class wines in both red and white, from two of the world’s favourite grape varieties, that no other region can compete with it in quite the same way. Release prices are going up and wines in the secondary market will continue to rise. Demand for all top end Burgundy is insane but the supply shortages of white coming up are going to impact prices heavily.

In brief, the whites from 2020 were picked early and characterised by mineral driven intensity and focus, not quite as fleshy as ‘17s, but fresh and zippy and generous too. Red berries were smaller than usual, with thick skins producing wines of good concentration and structure, bursting with fruit flavour and with early picking acidity was maintained.

Producers visited: Domaine Sauzet, Domaine Lorenzon, Domaine Chavy-Chouet, Domaine Ballot-Millot, Domaine Launay-Horiot, Domaine Duroché, Domaine Henri Magnien, Domaine Georges Noellat, Domaine Thibault Liger-Belair, Domaine Arlaud Pere et Fils, Domaine Marchand Tawse

For me the standouts were Sauzet, Duroché and Arlaud.

Bottle of the trip: Chambolle Musigny, Domaine G. Roumier 2017

Take aways from the trip: The quality of Thibault Ligier-Belair’s Morgon and how few people in the wine trade have ever been to Beaujolais!

The epic combination of Epoisses and red Burgundy (apparently, it’s ‘a thing’ but we didn’t know).

Many thanks to Flint Wines for organising the itinerary and to Cuchet and Co. for driving. Nice to see Albany Vintners, Brunswick, Decorum Vintners, FMV, IG Wines and Uncorked.

by Wine Owners

Posted on 2021-06-30

As mentioned in our recent and well received offer of the incredibly well priced Montepeloso Eneo 2010 (there are a few left), we promised a closer look into the relative value of Italian wines. I know I have been banging on about Italy for quite a while now but there is every reason for it – there is some terrific value to be had, and so on will I bang!

The facts are that there are only a handful of Italian wines that trade at, what we are going to call here, ‘silly money’ compared to vast swathes of wines from their rather posher neighbour - namely La Belle France. It is true that the same can be said for Spain, and for most of the New World. The U.S. is an exception, as like France, it has many an offering at ‘silly money’. But for my pound, I say sweepingly, these regions do not offer such a vast variety of quality wines that appeal in quite the same way (I should qualify at this point I am really talking about top quality red wines).

What Italy offers, unlike everywhere else, is a multitude of wines at relatively affordable prices with absolutely massive ratings. There are two variables here, the prices and the ratings; the simplest explanation for the comparatively lower pricing is that Italian wines have not yet been recognised, and accordingly priced, as truly international brands. Put another way, Asia has not got to grips with it yet. Other than a few ‘Super Tuscans’ and the top labels from the likes of Giacomo Conterno, Bruno Giacosa and Gaja from Piedmont, very little starts life close to £100 a bottle. There have been half a dozen EP releases every day last week from Bordeaux that qualify for that prize! In Burgundy a hefty percentage of premier crus start there and for some more sought-after growers, your £100 only buys you a taste of a lowly village wine.

The ratings are, rather obviously, dished out by the critics. It is worth remembering that each region is scored on its merits in a peer group fashion. The wines, as are the vintages, are reviewed in the context of that individual region or vintage. What has happened, however, is that tones have been set for different areas which do seem to vary from each other. Burgundy, for example, tends to harbour rather conservative scoring where anything over 95 is a massive achievement. Prices for these trophies are also massive. It is different in Italy. There are countless Brunelli with huge scores and even people in the trade ask, ‘how come there are so many 100 pointers we’ve never heard of’?

A possible explanation is that the bar has been set so high, and for so long, by the likes of DRC and Rousseau that a mere premier cru from someone like Dujac or Roumier is only worthy of 90/91 points. So, perhaps a cleaner canvas for the critics to assess has led to some more generous brushstrokes? Or perhaps it is a more generational thing; France has long been understood, consumed, and pontificated upon by the old guard, who might not quite understand the Italian way? An old friend of mine, an experienced wine merchant recently said to me “I don’t really get Italian wine” (Burgundy and Sauternes are more his bag!) and then confused me further by saying “except I couldn’t possibly eat Italian food without Italian wine”. I understand exactly what he means with the latter statement (but not the first), and this goes from pizza level all the way to Piazza Duomo, a three star Michelin in Alba – quite good by the way! Either way, some of the scores in recent times and particularly for the amazing ’16 vintage, in all of Italy, and the ’15 vintage in Tuscany, have drawn truly flamboyant landscapes from the young masters – and for not many Lira either!

The other thing to remember is that the critics live and die by their reputations, so if they are going to award high nineties or even the magical triple digits, you know the wines are going to be very good indeed – within the context of their peer group.

Obviously, we would love to hear from you to discuss the opportunities further and there will be offers to follow based on this theme. In the meantime, you may want to engage with the ‘Advanced Search’ button or take in some of these names which spring to mind:

Piedmont: Alessandria, Cavallotto, Grasso, Sandrone, Scavino, Vajra

Tuscany: Fontodi, Fuligni, Grattamacco, Il Poggione, Isole e Olena, Pertimali, Montepeloso

Ciao for now! Miles 07798 732 543

by Wine Owners

Posted on 2020-12-04

Wine Owners is the market-leading collection management platform that provides instant valuations and connects you with a peer to peer trading exchange.

Today, we're very pleased to announce that our collection management platform just got even better - and now includes a fabulous new home cellar management capability.

Imagine knowing exactly where each bottle is stored down to a hole in a rack, and being able to effortlessly move cases from a stack in the corner into bins or racks. Home cellars constantly change and this new release helps make organising them a joy.

Easily catalogue and organise wines at home.

Create new racks, bins and mixed cases

Move or add wines easily to your home cellar.

Save time by copying wines.

And create and update cellar references.

All this while getting the same high quality pricing data from our referential database.

If you want to start managing your home cellar, sign in to your account or create an account if you're not yet a member of Wine Owners.

by Wine Owners

Posted on 2020-11-23

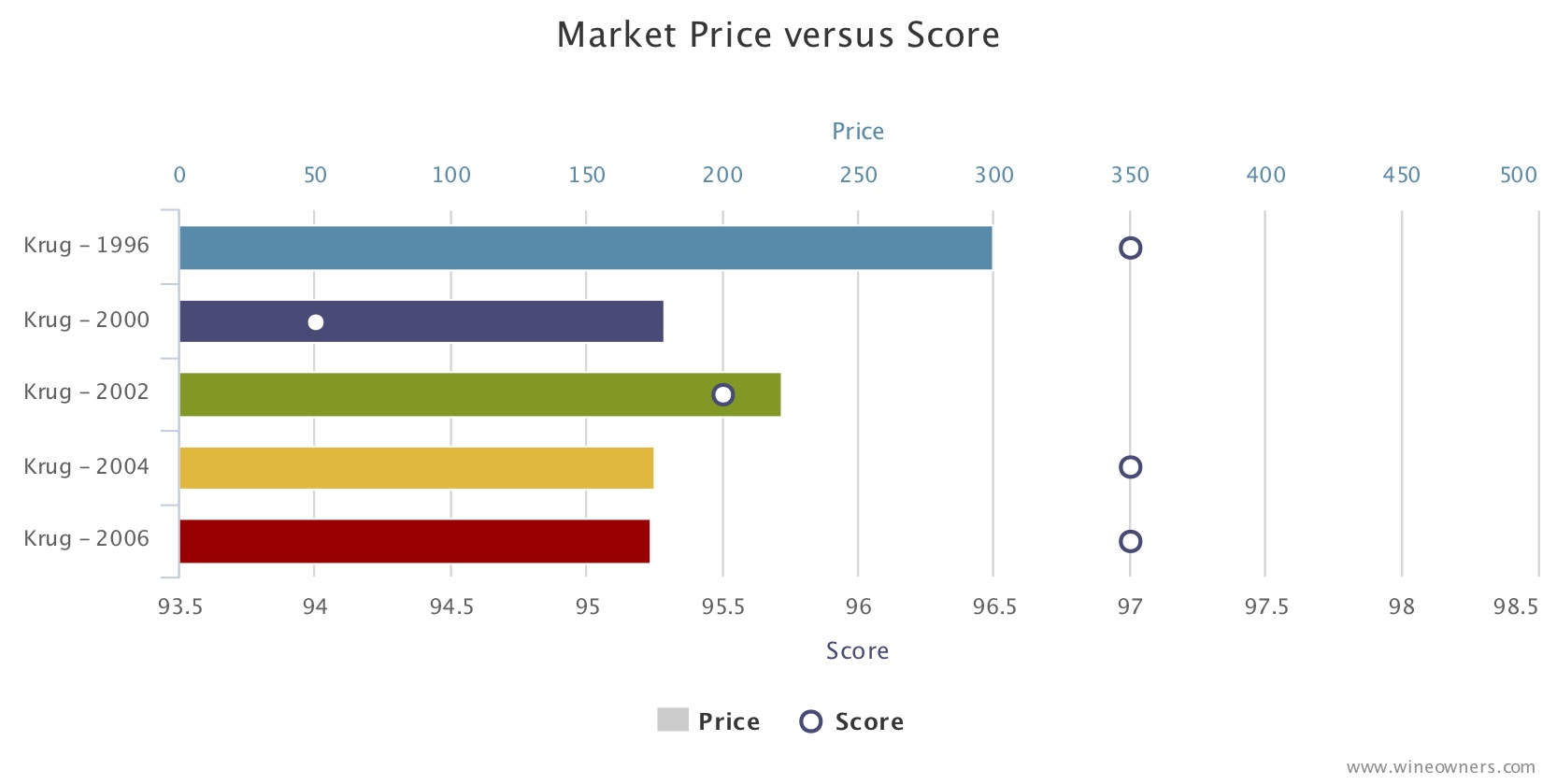

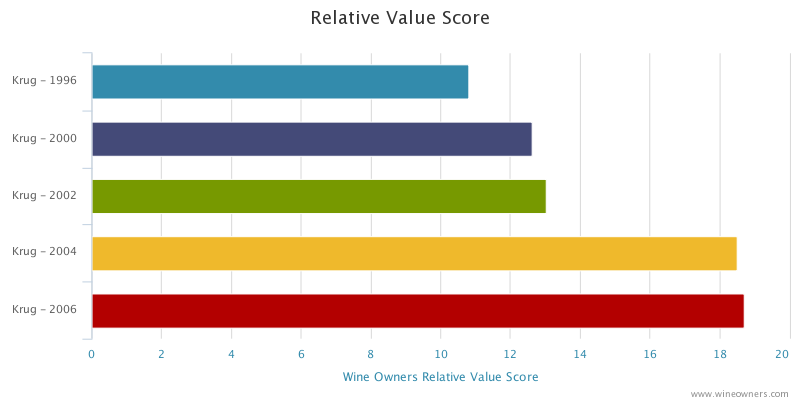

Krug is, surely, a Champagne that needs no introduction.

In all likelihood it is the first name to enter one’s head when considering the top names in the prestige Champagne bracket. It was the first thing I sought out on receipt of my first proper bonus! There are others obviously but Krug has carved itself a special niche of its own.

Krug, founded in 1843 produce a range of different cuvées ranging from the Grande Cuvée for everyday drinking (!) to the Clos d’Ambonnay for that very, very special occasion (at £2k+ per bottle it should be at least a very good excuse!). Here we are looking at Krug’s Vintage Champagne over some of the best vintages of the last two decades.

First, the market prices and scores:

And now the relative value score:

The mega vintage that is 2008 has not yet been released, so in the meantime I have no hesitation in recommending both the ’04 and the ’06 as very solid buys for the long term.

Banner Image: www.krug.com/the-house-krug

by Wine Owners

Posted on 2020-10-06

Miles Davis, October 2020.

7min read.

Given the lack of relatively significant news in the wine market, this is the first report since early in the second quarter of the year.

In fact, it is fair to say that the world of fine wine has been relatively boring, and in this world, boring is good! The lack of volatility has been impressive. The WO 150 index has (rather surprisingly) posted a gain of c.%5 this year but that should come with the caveat that the constituents are older vintages and not the most liquid.

In the aftermath of the 2008 financial crisis, the major wine indices (predominantly Bordeaux led) fell sharply (c.25%) as market players and stockholders marked down prices, desperately trying to reduce inventory. The relative newcomer, China, was busy buying all the Bordeaux it could at the time and was presumably a little surprised by this sudden easing of prices – after all, what did wine have to do with the financial markets??

Anyway, Bordeaux prices rebounded quickly and from early 2009 to mid- 2011 witnessed one of the biggest rises in prices this market has ever seen, followed by a sustained bull run for, the recently discovered by China, red Burgundy. Unlike 2008, the Covid-19 infested world of 2020 is yet to lead to a global banking crisis, but the economic effects will surely be felt for some time and some easing of prices would not be surprising; yet in the world of fine wine prices are not being marked down, and the indices are largely flat. There is no panic and this is good. As you would expect, liquidity isn’t great, spreads are wider, and there aren’t many merchants buying for stock. Overall, the volume of wine (number of bottles) traded has increased although there are widespread reports of the value being lower – hardly surprising.

Here’s the WO 150 vs. the FTSE in the last ten years:

Other than a reasonably successful 2019 en primeur campaign, of which more later, Bordeaux has maintained its trend of recent years - its market share continues to slide. In August it hit a new all-time low of 35%, according to our friends at Liv-ex. Ten years ago that number was 95%! It is still easily the most liquid market, however, and that should not be forgotten in times of stress. Lafite and Mouton Rothschild still dominate Asian demand but long gone are the days when the prices just kept on rising; they are flat.

The 2019 Bordeaux en primeur campaign was highly unusual, in many respects. Not only did it happen in lockdown, it happened, apart from the locals, without any but the top wine journalists tasting any of the wines – unheard of! We decided to listen more to Jane Anson (Decanter) and James Lawther (jancisrobinson.com), both based locally, than other international critics after reports of samples being abandoned on melting driveways and being flown around the world in a rush; it just seemed more prudent. The consensus, however, or whatever, was that it was another fabulous vintage and even came out with the highest average scores in fifteen years – no mean feat. The other strange thing that happened was that some Chateaux priced the wine attractively. Prices needed to be 20-30% below 2018 prices to sell through and some were. The leading names for relative value and quality were the Lafite (including L’Evangile) and Mouton stables, Pontet Canet, Palmer, Canon and Rauzan Segla. The campaign came as a much-needed boost to Bordeaux’s flailing reputation, but it took some extreme circumstances to bring it about. In terms of wine, Bordeaux is doing nothing wrong, it is the pricing that is the issue.

The super-fabulous-amazing 2016 Piedmont vintage has been dribbling into the market, some via the grey market European trade and some from agent releases. Given the general mood, these have been easier to accumulate than in a non-virus savaged world and without an organised primeur release. Who knows how well these wines would sell if you had all the merchants shouting their virtues from the rooftops at the same time? Three wines, all with 98 points from Monica Larner that make sense and that I have bought are: Cavallotto Bricco Boschis (£260 per 6), Elio Grasso Gavarini Chiniera (£375) and G.D. Vajra Bricco delle Viole (£360). Luciano Sandrone’s Le Vigne 2016 was awarded the magical three-digit score (ML also) which sent the price from c. £550 to £1,250 before settling at around £1,100 now. From the same estate, Aleste (formerly Cannubi Boschis), with a mere 98 points, makes sense at £650. The official U.K. release from Roberto Conterno will be in October and although they are not yet scored, I have been accumulating in the grey market. They have decided not to make Monfortino in ’16 as it’s not the right style (!!??), which can only leave Cascina Francia as one of the buys of the decade, but what do I know?

As readers know, I am a keen fan of Italian wines for the portfolio, particularly Piedmont and Tuscany and wines from here can easily take greater supporting roles. The lead roles of Bordeaux and Burgundy have never felt more questioned. Super Tuscans are well developed in terms of the market and continue to do well, other Tuscan wines to a lesser degree. 2015 and 2016 were epic years in Tuscany, as we already know, but the ‘16 releases of Brunello are still to come and there will be opportunities ahead.

This interplays with the theme of new areas becoming more accessible and more interesting. The rise of the new world continues gradually as the depth of this market grows. Wine knowledge is on the up, price transparency and trading channels are ever more abundant, so competition from other areas is bound to increase. Quality from everywhere is on the up and the international market is flourishing.

The Champagne market deserves more on the limelight too. Here is the ten-year chart of the WO Champagne 60 index, a smooth 9% annualised, with barely a bump in the road:

Burgundy is in a funny place right now. The froth has definitely been blown off the top end of the market, even before the pandemic struck and the usual suspects do not just fly out of the door anymore. There is still demand for DRC, but it needs to be in OWC. Buying is to order, not for stock, and prices need to be sharp to attain a sale. The performance of collectable white Burgundies has been greater than their red counterparts recently and this is a very interesting area. Buy top quality producers at an early stage and do not hold on too long – the fear of premox has not disappeared entirely!

Keep an eye out for South African wines, mainly for the drinking cellar at the moment, but quality and media coverage are on the rise.

Any questions, please let me know.

Good drinking!

Miles

by Wine Owners

Posted on 2020-05-19

Miles Davis, 18th May 2020.

Activity in the wine market in April was, pretty much, a repeat of what we saw in March. Numbers of alcohol and wine sales have been higher across the board since the pandemic struck, with people apparently drinking more, just less publicly! Closer examination would suggest quantity is winning out over quality, as volumes are up but values are lower. This comes as little surprise and this trend has been replicated on the Wine Owners platform. Plenty of gluggers being bought with little activity in the investment grade.

One interesting area of note amongst London’s fine wine traders, who have generally been quieter than in more normal times, has been a few very high value trades purchased by drinkers not investors. High value cases of DRC, Le Pin and other very top end names have been changing hands in piece meal fashion. Otherwise trade stumbles along with consumers rather than investors calling the shots.

The trends that existed pre the virus seem to be continuing and there is no question Italy continues to steal the limelight away from France. There is no doubt the lack of U.S. tariffs on Italian wines will be assisting here but Italy is on fire anyway. Some superb vintages from their finest wine regions, namely Piedmont (2016) and Tuscany (2015 and 2016) are proving popular amongst wine lovers who are accustomed to paying far more for their French equivalents. These wines are coming to the market now as the Italians release their wines much later than the French. The extra ageing that occurs helps enormously as the reputation of the vintage is not speculative; the wines will have been tasted and re-tasted, so that significant element of risk is eliminated. They don’t ‘do’ en primeur like the French either, so there is far less hype and less FOMO (fear of missing out), so all in all it’s better for the purchaser (the two countries really could learn quite a lot from each other!). Chateau Angludet released their 2019 yesterday, even though only a handful of people have tasted it, as the whole Bordeaux en primeur system challenges itself yet further. June is the current plan for the pricing up of Bordeaux primeurs and unless there are substantial price reductions, we must surely be looking more at a case of double amputation rather than simply shooting one’s own foot off!

Whatever happens with Bordeaux en primeur I strongly believe Italy and the rest of the world will continue to eat into the French gateau. The fine wine market continues to broaden, there has never been so much good wine coming out of other regions and other countries, with journalist’s coverage to match, and with points awarded to even outstrip that! The economic effects of Covid-19 are going to be felt far and wide and the quest for relative vinous value will be evermore sought after.

miles.davis@wineowners.com

by Wine Owners

Posted on 2020-04-08

Miles Davis, 2nd April 2020.

If we look at the performance of the wine market relative to the major asset classes, wine has, once again, demonstrated some fine defensive qualities. The wider wine market has traded in a narrow range in the last couple of years, but the WO 150 is still up 57% over a five-year period. So far this year the WO150 is -1.3%. The WO First Growth 75 Index is down 6.6% - not bad compared to the FTSE slide of over 26% (peaking at -34%). There is a correlation in that the Covid 19 crisis has brought both classes down but the difference in magnitude and the speed in which it happens is significant:

Perhaps there will be a time lag response to the wine market as liquidity is so relatively small and because professional investors will not even stop to think about wine in times such as these (a good thing!). Following the Global Financial Crisis in 2008, The Fine Wine Fund, which I was co-managing and invested entirely in blue chip Bordeaux, lost an average 5.5% a month between September and December.

| Wine |

Current Value |

MTD |

YTD |

1 Year |

5 Year |

10 Year |

| WO 150 Index |

306.56 |

2.00% |

-1.52% |

-0.26% |

54.19% |

83.43% |

| WO Champagne 60 Index |

488.78 |

2.24% |

1.73% |

6.53% |

62.87% |

151.71% |

| WO Burgundy 80 Index |

786 |

5.20% |

7.57% |

17.87% |

155.27% |

256.58% |

| WO First Growth 75 Index |

251.92 |

-0.29% |

-7.14% |

-9.68% |

34.15% |

46.01% |

| WO Bordeaux 750 Index |

365.35 |

2.71% |

0.08% |

8.06% |

68.39% |

105.06% |

| WO California 85 index |

685.88 |

1.42% |

0.04% |

2.46% |

94.94% |

292.25% |

| WO Piedmont 60 Index |

312.96 |

2.44% |

-5.89% |

-2.24% |

68.28% |

101.01% |

| WO Tuscany 80 Index |

339.75 |

2.33% |

5.82% |

15.45% |

77.51% |

96.32% |

So far, the current market does not feel like it is going to react in quite the same way as either back then or like the major asset classes. To start with Hong Kong (and therefore China) has been inactive for the last nine months, first with the political troubles and now the virus and inventory must have reduced but, more importantly, the strength of the US dollar versus sterling is in play. At the start of the year GBP/USD was 1.33, falling to 1.15 on the 20th March and now at c. 1.24. The depreciation of GBP has protected sterling holders of wine and encouraged dollar buyers back into the market – indeed, we have seen this as a noticeable trading pattern, one which will probably continue.

Our own experience is that we have seen buyers of first growth Bordeaux, village and premier cru Burgundy, 2016 Piedmont and some of the super Tuscans. Most of the sub-indices are in good shape but there are two points to note here; one is that merchants rarely mark stock down unless they have to and the other is that these are calculated using the only readily available price – the offer price. Bids may well tell a different story.

Overall, the wine market is going to struggle this year and I would predict mainline prices, i.e. liquid Bordeaux and expensive Burgundy will be up against it. There will be lots of opportunities however and I do not expect a sudden crash, as we would have seen that by now. In a normal market 2016 Piedmont would have been extremely difficult to buy but, as it is, it is proving a joy. This will not be the case when the dust settles and as there’s very little to go around, I repeat my buy recommendation.

N.B. Our Burgundy index needs reworking as it has too many older, illiquid vintages contained within it.

by Wine Owners

Posted on 2020-01-27

By Miles Davis, 27th January 2020

Summary

Piedmont is on the up, the area and the wine. The region is extremely picturesque, and the food and wine scene is superb. Winemaking is better than ever with younger generations bursting through full of energy and enthusiasm and the wines are getting better and better. In my experience, they are becoming more approachable too. The natural acidities of the grapes and the soils can handle, if not benefit, from the warmer climate and there have been some very fine vintages in the recent past. In global terms, Piedmont is relatively undiscovered and comparative values to other great regions make for a compelling story – read on!

Background

I have just returned from three glorious days in Piedmont. The weather was fine, the food was finer, and the wines were finer still! As readers will know, I have been singing the virtues of Piemontese wines, and the value they offer, for many months now. I was not expecting to have my enthusiasm heightened, just confirmed really, but this trip exceeded all expectations. I have been a few times before but the combination of seeing some top-notch producers, having a local courtier (David Berry Green, DBG Italia) as a guide, and in the company of both an experienced wine journalist (Victoria Moore, Daily Telegraph) and a wine merchant (Mark Roberts, Decorum Vintners), the stars aligned and we hit some celestial heights.

Compared to Bordeaux and Burgundy, Piedmont has not been making wine for very long, certainly not commercially. Producers have been operating for decades rather than centuries. The Nebbiolo grape that provides us with Barolo and Barbaresco was not even the top variety in the region 30 years ago, that was Dolcetto. Back in the eighties, Conterno Fantino encouraged larger orders by giving away six bottles of Barolo for every sixty bottles Dolcetto ordered! Now Dolcetto vines are being grubbed up and replaced by Nebbiolo - oh how trends change! This one will not be reversed, however. Producers are defensive on Dolcetto, arguing it makes wine for everyday drinking and whilst I really wouldn’t mind drinking Bartolo Mascarello Dolcetto most days, it doesn’t compare to the joys produced by Nebbiolo.

Victoria Moore & David Berry Green - © Miles Davis, Wine Owners

Notes

The striking and salient points derived from the trip were all positive. The region has never generated so much international interest, both generally and in the wine department, but largely thanks to the wine department. In 2014 ‘First floor Landscape of Piedmont: Langhe-Roero and Monferrato’ became the official name of a UNESCO World Heritage Site and this has brought tourism flooding in, although some of it is now becoming a problem. The village of Barolo itself and its 700-800 residents now plays host to international rock concerts; Bob Dylan and Eddie Vedder of Pearl Jam have played to 7,000 (presumably ageing and wine loving) rockers in the last couple of years. Basta! scream the residents, producers are less concerned. The U.S., Germany and England are already major markets for the wines, but others are growing. Australia, Japan, Malaysia, South Korea, Singapore were all mentioned, as was Scandinavia. There was one noticeable absentee – China. ‘Not yet’, the producers said.

© Miles Davis, Wine Owners

The Wines

The wines we tasted were largely brilliant and we all agreed what a good reminder it was when we had our first poor tasting - it offered reassurance that we hadn’t become so inured to the place that we had become complacent! To be fair the Baroli we were tasting were mainly from the fabulous 2016 vintage and we were tasting at very good growers, some famous, some less so, but more on them later.

I was surprised by the approachability of most of the wines, a marked difference to previous experiences. The wines were pale, supple and elegant and with a weightlessness (something that perhaps Nebbiolo can deliver more than any other variety) yet packed with fruit, power and nuance at the same time.

Times have been a-changing in Barolo country and where they haven’t changed too much, the results have improved dramatically. The ‘Barolo wars’ are well documented, indeed there has even been a film made about them and concern the traditionalist approach versus the modern. Briefly, this translates into long maceration periods and ageing in large oak barrels (botti), the traditional approach, versus shorter maceration, temperature controlled fermentation and small oak barrels, the modern. It was interesting to note that the two wineries employing the highest percentage of small oak barrels produced the least good wines. The better wines were made in the traditional way but are harvesting better fruit, implying improved work in First floor.

As with other regions, alcohol levels in Piedmont have been rising, largely due to climate change. Most of the wines tasted were at 14.5%, but such are the natural acidity of Nebbiolo and the soils you really don’t notice, at least not until you’ve had the whole bottle yourself! It is a very different experience compared to drinking Bordeaux wines at the same level. Another local variety, Pelaverga, produces an even paler juice which is amazingly light and fruity. I had just started dreaming of summer barbecues when I noticed G.B. Burlotto’s offering weighed in at 15% - keep it away from the kids!

-G.B. Burlotto © Miles Davis, Wine Owners

The Market

As previously commented on here, the market in Piedmont wines is firm. Without the geopolitical issues currently hanging over the wider market, it would be a fair chunk firmer. The very loudly heralded 2016 will be released this year and buyers are waiting to pounce. If 2010, another great vintage, is anything to go by they most certainly will, and probably in far greater numbers than back then. In the grand scheme of things, Piedmont is an adolescent and will continue to grow. Wine making will continue to improve and prices will rise.

The Producers (in brief) (and not all)

Punset (Nieve) – previously unheard of (by me). Bio-dynamic and very in touch with climate and nature. Only releases when the wines are ready. Marina Marcarino’s Barbaresco Basarin 2013 (a year very similar in weather to the brilliant 1982, her first vintage) is available now. Delicious and only 13% alcohol. So desperate to make wine, she lied to her parents about the course she was taking at University. They wanted her to join their family widget making business – we were all glad she didn’t! Her range is just great, elegant and refined. She may even save the planet too.

G.B. Burlotto (Verduno) – Premier League status and I now know why! Verduno, at the northern tip of Barolo country, is the village of the moment and its best vineyard, Monvigliero, known for its elegance, is the piece of dirt everyone wants a piece of right now. Fabio Alessandria makes c. 8,000 bottles of Monvigliero - Investment Grade ‘A’. His whole range is superb.

Fratelli Alessandria (Verduno) – Cousins of Fabio and not to be confused with the Glaswegian band. Rising up into the Premiership. Traditional methods, improvements in the winery and focusing on improving quality, not expansion. Their Langhe Nebbiolo ‘Prinsiot’ 2016 is already in my cellar for drinking and I’ve been buying ’13 Monvigliero for investment.

Trediberri (La Morra) – Nicola Oberto and his parents bought a 5 hectare site in La Morra in 2008 and have 2 prime hectares of Rocche dell’Annunziata. Definitely one to watch, this guy is on the move and has been studying Bruno Giacosa’s methods. Refreshingly honest, he was genuinely most excited about his recently made Annunziata 2019 - at three months of age! The Langhe Nebbiolo ’19 might be one to sample. Moving from on the radar to gentle accumulation…

Trediberri (La Morra) – Nicola Oberto © Miles Davis, Wine Owners

Roagna (Castiglione Falletto and Barbaresco) – Now in the hands of Luca Roagna, they are one of the few growers making really serious wines in both Barolo and Barbaresco. The star has been rising for some time. Organic with old vines. We tasted wines from the poorly reviewed 2014 vintage (he releases later) at 10 degrees in the cellars. Although the wines were also cold, they sang their heads off. Both from Barbaresco, the Albesani (2,000 bottles) with the most amazing nose and the Montefico (1,000 bottles) stood out for me. Invest with confidence!

Crissante, La Morra – not on my radar before, Alberto has been running this family affair (we met Nonna (his nan), 88 and still dancing) since 2008. The family owns 6 hectares of vines, 5 of hazelnuts and a lovely holiday house they rent out. The Barolo Classico ’16 will ticks a lot of boxes when released. Thier Capalot ’15 will also give immense pleasure. The ’13 is currently available. Firmly on the radar now.

Bartolo Mascarello, Barolo – Investmnent Grade A. Brilliantly understated and traditional with a touch of jazz, but only in the artwork on display. Maria Theresa’s 2018 Dolcetto was superb, the ’16 Barolo sublime. A blend of 4 vineyards with production at 15-20,000 bottles. Genius. Interesting to spot an empty Trediberri box by the back door!

Giovanni Rosso (sounds so much better than Red John!), Serralunga – Proprietor Davide turned up as we were leaving, completely unphased by his tardiness. How someone so laid back has managed to create such a bustling business is amazing; two tasting rooms, one with a full restaurant style kitchen, a helipad, a contract to make BBR house Barolo and sales all over the world. Our impromptu host excelled in showing us the famous Vigna Rhionda vineyard. Once our feet were double caked in clay he informed us the terroir was nearly all limestone! A rushed tasting followed which was a bit inconclusive but with their top cuvée selling at £500+ a bottle, something is working. Another visit required!

Luciano Sandrone, Barolo – impeccable presentation. Famous for their Barolo labels Cannubi Boschis (Aleste since 2013) and Le Vigne, and now the uber rare Vite Talin, that they vinify themselves, they not only sell a lot of grapes from their Roero sites, they also sell finished wine to others. A mixture of traditional and modern. Barbara works with her Uncle Luca, only 3 years apart in age and Luciano (Barbara’s father and Luca’s brother) is still on site having begun his wine life with Giacomo Borgogno, bang next door and right under the slopes of the Cannubi Bioschis vineyard. Great 16s, the 15s also very attractive. Lovely wines, I have been buying and will continue.

Sandrone © Miles Davis, Wine Owners

General comment

It was an inspiring trip and easily surpassed expectation, particularly in the wine department. Growers tend to be family run businesses, are friendly, engaging and genuinely passionate. The bigger businesses are the antithesis of this and, dare I say it, more reminiscent of Bordeaux producers. These personalities are clearly reflected in the wines and different styles are very apparent.

On my return to my desk I found the tail end of the Burgundy 2018 en primeur offerings. The relative prices just do not make sense. On every level, there is no comparison; there are dozens of Grand Cru Burgundies from a host of producers releasing wines at more than c. £150 a bottle, in Piedmont a tiny handful. From a recent release of Giacomo Conterno’s 2015 wines, only the legendary Monfortino (the most expensive wine in all Piedmont) was above this price level. Many Burgundy premier crus cost more than exceptional Barolo cru, village wines more than ‘classico’ blends etc., etc.

For drinkers and those wishing to dip their toe, all of the producers make an entry level wine, be it a Langhe Nebbiolo, a Langhe Rosso or a Nebbiolo d’Alba. These are released earlier than the aged Barolos and offer an inexpensive way of treating yourself and opening the door.

As ever, please fire away with questions.

© Miles Davis, Wine Owners

by Wine Owners

Posted on 2019-12-09

I have just finished reading the latest threats relating to U.S. trade tariffs. In response to France’s application of a 3% digital services tax on heavyweight U.S. tech companies (you know the ones), DT and his representatives are considering recouping $2.4 billion from France’s premium markets; namely handbags, make up, certain cheeses and sparkling wines made from grapes. These tariffs will not be introduced until the new year if at all, so Christmas is saved at least. These products are possibly facing a 100% tax penalty so it’s out with Vuitton, Chanel, Roquefort and Krug and in with Coach, Maybelline, Monterey Jack and Napa Mumm – maybe Brexit isn’t looking quite so bad for us Brits after all!

How these lists are drawn up I do not know; the cheeses include Edam, Gouda and Parmesan which, as we all know, are not known for their Gallic qualities. Unlike still French wines below 14.1% alcohol, Champagne dodged the tariff bullet in October but may now be hit four times harder. These tariffs are messing up our market and we don’t like it! Tit for tat exchanges cannot be the way forward, and we look and hope for more stable trade agreements globally, but we must live with them for now. We have heard of several ‘swerves’ so far; U.S. buyers storing in Europe in the short term, importers identifying the highest alcohol level of any of a producer’s wine and employing that number universally across the producer’s range and even producers being asked to mark 14.1% on the label!

| Index | Current Value | MTD | YTD | 1 Year | 5 Year | 10 Year |

| WO 150 Index | 315.67 | -1.95% | 1.44% | 2.03% | 62.62% | 91.05% |

| WO Champagne 60 Index | 493.15 | 0.77% | 5.40% | 7.02% | 73.96% | 166.01% |

| WO Burgundy 80 Index | 744.26 | -0.61% | 6.08% | 7.35% | 147.25% | 239.18% |

| WO First Growth 75 Index | 274.38 | -3.16% | -2.76% | -2.65% | 48.45% | 64.45% |

| WO Bordeaux 750 Index | 366.5 | -2.23% | 8.20% | 8.98% | 69.82% | 111.68% |

| WO California 85 index | 679.17 | -3.41% | -0.14% | 0.83% | 98.95% | 296.39% |

| WO Piedmont 60 Index | 335.87 | -1.70% | 5.64% | 6.32% | 81.94% | 125.17% |

| WO Tuscany 80 Index | 312.88 | -2.43% | 6.86% | 10.01% | 61.16% | 86.68% |

As predicted last month, the indices are beginning to tell the story of recent headwinds. It is interesting to note that Champagne was bucking the trend - that will not continue now. All the other main indices drifted down; the Italian numbers surprise me as the wines we are currently seeking to accumulate have shown no weakness in price. Italy remains free of any U.S. tariffs although further scrutiny can be expected.

I expect there to be some continued easiness in the market in the short term, but I would not recommend selling now as I think it unlikely the market will retreat by 10% or more. Spreads have widened a little and bids are currently around 10% (or more) below the cheapest market price. There will indubitably be some very interesting buying opportunities in the coming months for those brave (and clever) enough and it is interesting to note rarer stocks already becoming available. Great 1990 Bordeaux is a perfect example; normally very scarce and difficult to buy, there is some volume available and it is a buyer’s market.

If some of the current headwinds, namely Hong Kong politics, U.S. tariffs and uncertainty surrounding GBP stemming from UK elections, and no deal Brexit fears, died down activity would increase, and the wine market would soon shore up. In the world we live in, with low (or negative) interest rates and where investors buy bonds for capital appreciation and equities for income, wine will make a lot of sense again soon. There needs to be a certain amount of unravelling of these issues first, however.

Please contact miles.davis@wineowners.com with any questions.