by Wine Owners

Posted on 2022-02-03

As eagerly anticipated as the Sue Gray report, here it is, the annual WO round up and look ahead.

So, what happened?

2021 turned out to be a very good year for the wine market, the owners of wine and therefore for Wine Owners Ltd. also. Turnover on the exchange ramped up by 77% in 2021, producing more buying and selling opportunities than ever before! Our tenth year of trading is set to be an exciting one and has started well.

The broad based WO150 Index returned +15% with the stars of the show being Champagne and Burgundy, posting respectively +30% and +27%. Bordeaux returned a more modest 10% while Italy, having led the charge in 2020 came in with more modest numbers, yielding 6.5%. Tuscany performed better than Piedmont which was flat on the year. The Rhone did well, notching low double figures and the Rest of the World was twice as good as that, all thanks to California.

The reasons for the strength in the market were various; probably the biggest two were continued liquidity being pumped into the system in a low interest environment pushing more buyers into real assets, and the very real fear of inflation. Savings derived from staying at home more seems to have pushed up the spend on what people have been consuming at home – a quality driven drowning of sorrows in yet another lockdown!? The lifting of U.S. tariffs on some European wines brought a weight of new buying activity from across the pond, as did a lot of ‘new wave’ investment dollars - this should not be underestimated.

The market pre Covid had been largely stifled by various different factors but once demand started to outstrip supply, the market started to motor. Hong Kong and China were not responsible (for once) and collectively have been less of a force in recent times. Stringent lockdowns and border controls have meant very few visitors, especially of Mainland Chinese to Hong Kong, and an exodus of wealthy residents seeking a more liberated culture – some of the demand is moving elsewhere. Current thinking is that will last for some time (not just until after the Winter Olympics!), so be warned. I would expect Singapore to take up some of the slack and become a more prominent player.

Champagne

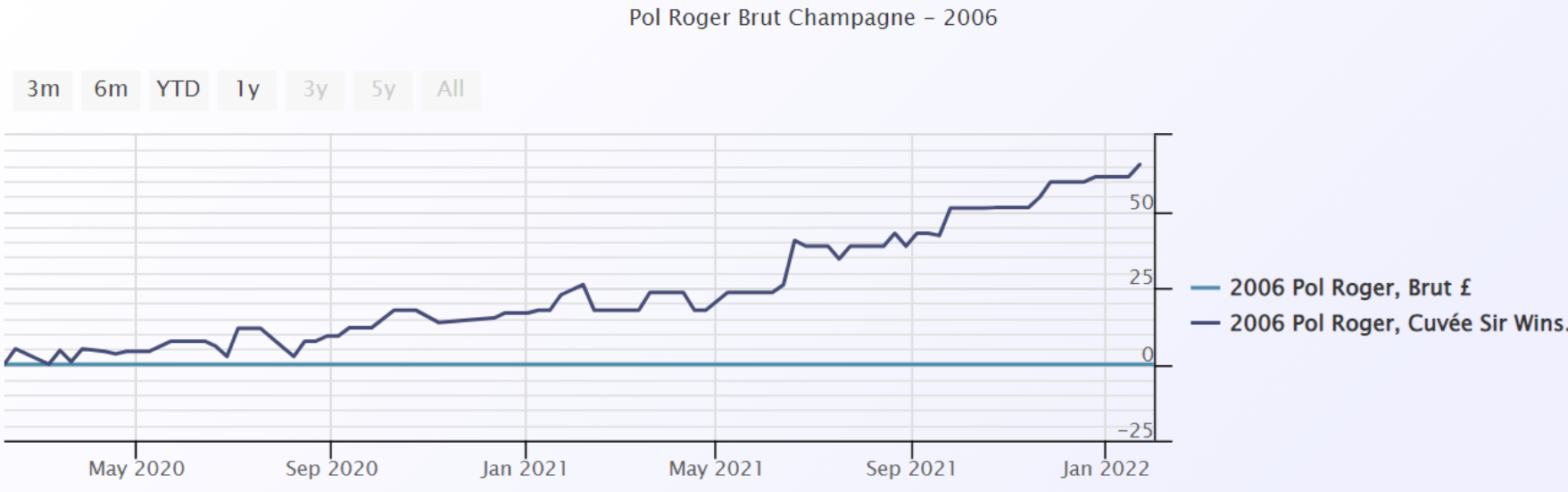

I cannot remember Champagne ever being the star turn in the wine market before but given the cyclical nature of the market and the fact that the different regions are much more equal than they used to be, it is not surprising. It has also consistently delivered steady returns, see my report from last July, just before the market really accelerated. Reports of supply shortages coming out of the region and a slew of really good quality releases added further weight to the concept of Champagne as an investment proposition which led to some voracious buying activity. The Champagne Index is dominated by the biggest names and/or the tête de cuvée of noble producers. As ever, fine wine collectors and investors focus in on the most prized assets driving the gap between the seriously good and the seriously a little bit better than that ever wider. Here’s a good example, vintage Pol Roger ’06 versus the Sir Winston Churchill cuvée from the same year:

The ‘simple’ vintage Champagnes from good producers offer extremely good value to drinkers and is a segment of the market that has been left behind.

Where Champagne goes from here is one of the big questions as some of the recent returns have been enormous. Various vintages of Krug, Dom Perignon, Taittinger’s Comtes de Champagne, Pol Roger’s Winston Churchill have added more 50-100% in the last year and rosé Champagne has been bought in a way not seen before. I am tempted to take some profit from some of the biggest risers and look for some laggards.

Burgundy

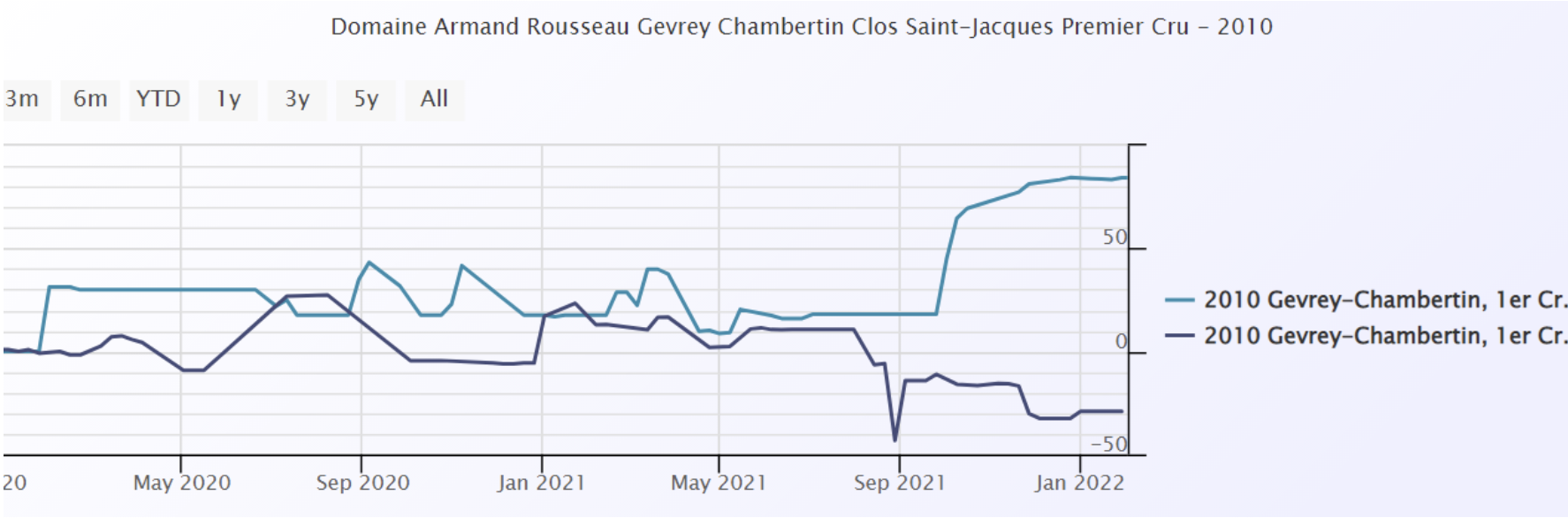

The polarisation of the wine market and the premiums attached to the most desirable names have continued to grow and probably make less sense than ever before. Names such as Leroy, DRC and Rousseau in Burgundy have outperformed their neighbours and as highlighted in some of our recent offers, often trade at multiples of equally high scoring wines from the same vineyards but from less famous producers. Obviously, this creates opportunity and I feel more comfortable making bets at the prices that are a fraction of the big guys. Here is a comparison between Armand Rousseau’s Clos St. Jacques (light blue) versus Bruno Clair’s. This sort of chart can be repeated numerous times - premiums have become too large for my liking, but if Rousseau is your man and you have the cash….

The current shortage of 2020 red Burgundy and the general short supply frost hit ’21 vintage, see report from last November, will push prices and demand ever higher and whilst some price performances seem overly vertiginous, I anticipate they will continue their path – for now at least. High rollers love spending big on Burgundy and the small production levels really adds the glitter dust to this famous region. And there are always the producers that are beginning to make a name for themselves.

Bordeaux

Bordeaux had a decent year, posting +10%. Apart from a brief flirtation with the 2019 en primeur release, Bordeaux has not been sexy for a very long time now. Market share continues to fall as other regions eat into the Bordelais’ gateau. It is still, and always will be, the largest slice of the market and those who buy into the general wine argument and need liquidity are best allocating here. It has become the steady Eddie. As a massive generalisation you know what you’re getting in your glass with a Bordeaux; a lot of that infuriating yet bewitching and beguiling wonder of what to expect from your wine just doesn’t exist in the same way that it does with Burgundian Pinot or Piedmont’s Nebbiolo and passionate collectors are just not quite so aroused by its charms (as I said, a generalisation!). I expect it to remain firm however.

Italy

Italy has had a mixed year. Super Tuscany has done well, the massive names of Sassicaia, Tignanello and Masseto have continued to shine posting average gains in the region of 25%, 35% and 25% respectively, and Solaia and Ornellaia also, but not so brightly. Lots of smaller Brunelli have fared quite well and this sector continues to build – hardly surprising given the price to quality ratio. Piedmont has had a mixed time, Monfortino in general is up a little in most vintages but lots of big names across the region have remained unchanged. I would not be surprised to see interest return to this area once Burgundy’s current run has blown through. There are still numerous 2016s looking very interesting for the longer term.

The Rhone

The Rhone valley is more appreciated than ever before. There are numerous cult producers all over Cote Rotie, Hermitage, Cornas with St. Joseph coming to the party nowadays. Prices of Rayas product from down south have travelled to the far north as collectors chase these rare treasures. White Rhone is still very much a speciality interest but one to keep an eye on. I have bought a lot of red Rhone for drinking from the WO platform in the last year or so as the combination of maturity, quality and price is virtually impossible to beat. There are plenty of names delivering superior returns too.

The Rest of the World

California has dominated the remaining regions with some ease, posting over 20%. Screaming Eagle has led the pack, followed by Ridge and Dominus. Australia has suffered at the hands of China’s tariffs.

Conclusion

I am confident the market will continue to perform well this year. Sentiment is strong, and supply in some key areas is shorter than usual, especially Burgundy. The inflation fear mentioned earlier is real and wine has been seen as a good hedge against this for a long time now. Interest rates are likely to rise but remain historically low and the real asset argument holds sway but will lessen as QE reverses – something to keep an eye on. Access to the fine wine market is greater than ever before, particularly in the U.S., and continues to grow.

As ever, I would be delighted to hear from you to discuss any of this, or anything else wine related. I am happy to help and advise on your portfolio or cellar, for investment or drinking purposes. And now we can go out again I would be delighted to share a bottle!

Miles Davis 02/02/2022

by Wine Owners

Posted on 2020-12-09

Miles Davis, Wine Owners December 2020

As we head into the final phase of this extraordinary year, the world of wine investment is a calm and beautiful little side water, gently ebbing and flowing with that serene feeling it knows where it is going.Traditional assets continue to bounce around, no doubt causing palpitations and stress. More than ever, this year has been about timing in the capital markets, and if you got that wrong, the chances are you got it expensively wrong. Not so for vino! Unlike after the global financial crisis, the wine market has held its nerve, merchants did not mark down prices and the market has been stable. Investors are about, and even Bordeaux prices feel like they are firming up. Collectible assets are in vogue and it is easy to see why given these circumstances. You cannot even hold, let alone drink, a bitcoin, a share, a derivative, an option or a future and a bottle feels good, especially in lockdown!

Demand from Asia has increased and merchants trading the big names have been pleased with activity levels in recent weeks. There is almost a feeling there is an element of restocking going on after a quieter than usual period (in Asia) over the preceding months. This has happened in a period when the currency has gone against dollar buyers, although only marginally. Buying is very specific but certain names have moved up considerably since the middle of the year, Mouton ’09 and ’10, for example, are both up c.10%, the controversial ’03 c.14%. There does not appear to be any thematic buying, however, so it is not possible to call a vintage, or a certain Chateau or producer. Keep looking for the relative value is my suggestion and do not forget to make use of the useful tools we provide. See below for an example (if anyone would like a demo on how to use this, please ask):

In Burgundy, especially in the trophy sector, if it is not in its original packaging it is not going anywhere and vice versa. We have seen big ticket items in Leroy and Cathiard sell well recently. Provenance is key and is proving valuable.

Piedmont, Super Tuscans and Champagne remain firm, as does my conviction as areas for further purchasing.

We have had a lot of demand for Penfolds products; whether that continues given the newly slapped Chinese tax on Aussie wine imports will be interesting to observe but, in the meantime, we have plenty of two-way activity.

Personally, I have never been able to compute the prices of some of the ‘Cult Californian’ wines but, in fairness, I have rarely tasted them. Not so for that wonderful producer that is Ridge; the wines are lovely and the prices reasonable, in normal fine wine language, and a total give away compared to some of the ‘cult’ counterparts. We have offers of the flagship, Monte Bello, on the platform of the ’10, ’13 and ’17 that I would happily recommend, to anyone!

**************************

We have been busy at Wine Owners, with a lot more trades going through, spread amongst an ever-increasing group of followers. We are at record levels of new subscribers and have £300k of fresh offers in the last week alone. Notwithstanding the difficulties of some warehouse operations presented, our back office is working well, and our post trade analytics improve all the time.

On that bullish note, the team and I would like to thank everyone for their ongoing support. For those who have not yet fully engaged, we look forward to welcoming you soon.

Have a very happy Christmas, a wonderful new year, and drink as well as you can!

Miles Davis, 8th December 2020

by Wine Owners

Posted on 2020-11-12

Miles Davis, Wine Owners November 2020

There is not much to report on for October. The market continues to be very steady, gently rising in fact, and lacking in volatility – we are leaving that for the traditional asset classes and for those with a strong constitution!

The Covid related news had been sending shivers down the spines of stock markets as we here in the UK were heading into our second full lockdown of the year, only for that to turn around swiftly on the good news on vaccines.

The platform was busy in October, however, with good demand from Asia. Bordeaux indices have even been positive although overall market share remains weak. Sterling had been a little weaker during the month and this normally speedily converts into demand for Bordeaux blue chips from Asia. We have seen continued demand for Italian wines and Champagne with red Burgundy more mixed. Top end white Burgundy priced sensibly soon disappears from the platform and liquidity in this sector is perhaps stronger than it has ever been.

Champagne is the focus of the month and there could even be unprecedented Christmas demand this year if lockdowns ease and families and friends are once again allowed to socialise!

The recent release of Taittinger’s Comtes de Champagne 2008, which receives a fabulous write up from William Kelley of the Wine Advocate and 98 points, was met with great interest. There’s plenty of supply right now but given time there is plenty of room for price upside given the level of the ’02 now. Here is the relative value chart:

Obviously ’06 is the cheapest here but that, nor the ’04 vintage, quite carries the same stature of the fabulous ’02 and ’08 vintages. Having said that and given the quality of the juice we are talking about, Relative Value Scores at 30 or above look good in any book!

Generally speaking, I like the lower production levels of Pol Roger’s Winston Churchill Cuvée. In fine wine terms, Dom Perignon and Cristal produce vast quantities but are truly international brands and therefore trade at premiums to other names. Comtes falls somewhere in between.

Here are some price and point comparisons of the names discussed here, from really good to excellent vintages.

Overall, I would not put anybody off buying these wonderful wines for the medium to long term, they have years of life ahead and plenty of upside potential as they become rarer and rarer – and more golden!

|

| | Vintage | Price | WA Score | Price/Point (WA) | VINOUS Score | Price/Point (VINOUS) |

| Dom Perignon Champagne | 2002 | £127 | 96 | 1.32 | 97 | 1.31 |

| Dom Perignon Champagne | 2004 | £107 | 92 | 1.16 | 95 | 1.13 |

| Dom Perignon Champagne | 2006 | £108 | 96 | 1.13 | 95 | 1.14 |

| Dom Perignon Champagne | 2008 | £110 | 95.5 | 1.15 | 98 | 1.12 |

| | | | | | | |

| Louis Roederer Cristal Brut | 2002 | £213 | 98 | 2.17 | 94 | 2.27 |

| Louis Roederer Cristal Brut | 2004 | £160 | 97 | 1.65 | 96 | 1.67 |

| Louis Roederer Cristal Brut | 2006 | £130 | 95 | 1.37 | 95 | 1.37 |

| Louis Roederer Cristal Brut | 2008 | £158 | 97 | 1.63 | 98 | 1.61 |

| | | | | | | |

| Pol Roger Cuvee Sir Winston Churchill | 2002 | £167 | 96 | 1.74 | 96 | 1.74 |

| Pol Roger Cuvee Sir Winston Churchill | 2004 | £127 | 95.5 | 1.33 | 93 | 1.37 |

| Pol Roger Cuvee Sir Winston Churchill | 2006 | £117 | 95 | 1.23 | 96 | 1.22 |

| Pol Roger Cuvee Sir Winston Churchill | 2008 | £140 | 97 | 1.44 | 95.5 | 1.47 |

| | | | | | | |

| Taittinger Comtes Champagne Blanc de Blancs | 2002 | £166 | 98 | 1.7 | 97 | 1.71 |

| Taittinger Comtes Champagne Blanc de Blancs | 2004 | £96 | 96 | 1 | 96 | 1 |

| Taittinger Comtes Champagne Blanc de Blancs | 2006 | £73 | 96 | 0.76 | 95 | 0.77 |

| Taittinger Comtes Champagne Blanc de Blancs | 2008 | £117 | 98 | 1.19 | 96 | 1.22 |

by Wine Owners

Posted on 2020-01-16

This article is a follow up to our 2019 year end round-up by Miles Davis, published on the 10th January 2020.

The outlook for 2020

The geopolitical climate will continue to dominate the fine wine market in 2020. Uncertainty continues to hamper confidence amongst wine traders and although our view that the robust long-term fundamentals of wine will play out, there are some short-term issues (more on these below) that need to settle. If these issues, some of which are very specific to the wine market, can settle, we will look back on 2020 as the year of opportunity. Physical assets are doing well, gold is at a seven-year high, and we live in a climate of negative real interest rates. Stock markets are trading at all time highs and there is liquidity in the system, it’s just not finding its way into wine right now. Wine has been underperforming these other assets recently (one-year performances), see here:

The fine wine market continues to develop and change, and is becoming more interesting, with different fundamentals developing for individual markets, making them more autonomous all the time.

A whole new and significant factor is the U.S. and its trade tariffs, not only treating wines from different countries differently, but Champagne differently to still French wines, and wines above or below 14.1% alcohol from the countries on their hit list. Tariffs will influence the underlying markets, so until we have further clarification it is difficult to predict what may happen next.

As a result, I expect the wider market to start the year a little unsure of itself. There are and will always be opportunities within the wine market, however, but perhaps portfolio allocation has never been more important, producer too. And maybe more important than both of those considerations, are prices and relative value. Buying on the bid side of the market will be the key and good buying will be richly rewarded.

A reminder of performance over a five-year period:

I continue to favour Italy, particularly Piedmont and some of the super Tuscans and vintage Champagne. 2016 was an amazing vintage for Piedmont and new releases of Barolo should be considered. Of the major markets, I am generally lukewarm on Burgundy, but keener on Bordeaux where some fantastic older vintages, particularly ’89, ’90 and ‘96, are more available on the market than for some time. I think there will be some amazing opportunities this year in this area. I maintain my view that younger Bordeaux is fully priced, especially block buster vintages of ‘05, ‘09 and ’10 where supply is still plentiful and prices are high. I would be highly selective and very price sensitive in California and other ‘lesser’ investment markets, and always on the look out for lower levels of alcohol.

If I had to name one brand to buy this year it would be Sassicaia.

The issues in 2020

Brexit

The election result in the UK cleared the UK air after a period of uncertainty and it appears that producers and importers are relaxed, for now, about any Brexit impact.

Tariffs

The possibility of further U.S. tariffs has taken the place of the Brexit uncertainty but the situation there will become much clearer in mid-February, but I cannot believe anyone is going to be brave before then. If the tariffs remain as they are, I think the market will react in a positive way, negatively if they are any more punitive. The fact that the tariffs are only levied on wines under 14.1% alcohol, and thus wines stronger than that are exempt, is largely ignored by the market as an overriding sentiment takes over and the damage is done. Only wines from England, France, Germany and Spain are currently subject to these measures, making the rest of the world, particularly Italy in my view, look more interesting in the short term. France has particularly annoyed the U.S. with its digital tax aimed at the big tech companies and Champagne, given exemption last time round, may be in the firing line. But who knows what is going to happen next on this issue – the uncertainty is somewhat paralysing.

Hong Kong

The situation in Hong Kong is also creating uncertainty. The people are scared about the future and feel strongly enough to risk life and limb in protest, and China is not happy. The protests have calmed down from their most violent but there were heavily populated demonstrations at the turn of the year. Last week Beijing replaced their H.K. liaison officer with a senior and trusted aid of President Xi, hardliner Luo Huining, who ominously says that “everyone eagerly hopes Hong Kong can return to the right path." He comes with a reputation for fixing tough problems for Beijing!

The situation is complex, and it is likely the impasse will run and run. China can afford to be patient; it is sitting with the stronger hand and can probably slowly strangle the territory into submission without using undue force. Hong Kong has a long history of migration (especially post Tiananmen Square) and the numbers from now on will make interesting reading. Mainlanders are currently arriving at the rate of 50 a day but how many are leaving? Ultimately, I expect a huge number of democracy loving, wealthy locals will be leaving before 2047 but that this is the dawning of a new era for Hong Kong.

As well as being a lively wine hub itself, Hong Kong has been and is the gateway to China for fine wine and houses a lot of the experience and expertise in the region. More than ever, personnel and the location of businesses are transferable, and Hong Kong may lose market share in the longer term. This does not affect the long-term demand for wine, just where and how it is traded. If China was to open Shenzhen as a free port, for example, the impact would be immediate, and Hong Kong would be shunted sideways.

Other themes and points of interest

Bordeaux

The overall share of trade in the wines of Bordeaux has continued to decrease and the 2018 en primeur campaign was another damp squib. 2019 is another good, possibly great, vintage but the Bordelais need to respond accordingly if they want to stop the rot (how many times have we heard that!??). Young Bordeaux wine is still in a state of over supply with warehouses packed; a new lease of life is urgently required and if the Bordelais, by lowering prices, can take advantage of the huge media machine of en primeur to capitalise, they have a chance to turn the worm. I believe they have severely undervalued the power of the en primeur message over the years – we live in hope!

Climate change

Apart from the devastating fires we have seen in the U.S. in recent years, and Australia very recently, what does climate change mean for fine wine? Although winemakers are learning new techniques to deal with warmer weather the obvious and irrefutable consequence will be higher alcohol levels. Bordeaux 2018 demonstrated this in spades, with most wines well above 14%, and some around 15%. Although a lot of these wines can be well balanced, where the riper, more generous fruit copes with the higher alcohol levels, it does not take away from the fact there is a higher level of alcohol, and that’s not good. Most people, but especially connoisseurs, would prefer their wine to be around 13%. Other than the obvious benefits of scarcity, this is another good reason to favour older wines, they tend to be less alcoholic. I remember 2010 recording higher alcohol levels than we were accustomed to and causing quite a stir at the time - they seem perfectly natural now.

General (more for drinking)

South Africa has been receiving some very good press in recent times and quality is improving. It maybe not yet offering wines for investment, but it is certainly worth dipping a toe. I recently bought Meerlust’s Rubicon 2015 following some massive reviews, for not much money, for example.

Piedmont has had a string of good vintages, and there’s a lot of great quality Langhe Nebbiolo and Barbaresci on the market. Produttori del Barbaresco 2016s are both excellent and good value. Prices for these types of wines are the equivalent of generic Bourgogne.

Climate change is good for Beaujolais. The Gamay grape is a tough little number that needs plenty of sun and warmth. There has been plenty of investment in the region and quality and the number of wines providing pleasure is on the up. Do not overlook the versatile Chardonnay from the area either, a leaner style in general compared to the Maconnais and further north.

2018 Burgundy will provide plenty of easy pleasure but don’t believe all the hype from the merchants. Check alcohol levels, there are some that are too warm but in the main they, especially the reds, are generous.

Try and understand the critics and their scoring. At the Judgement of Paris in 1976, the range of scores, out of twenty, came in between two and seventeen. Some of today’s critics don’t really start at anything below ninety three (out of one hundred) and famous producers in half decent vintages are all north of ninety five. Big scores sell wines and are commercially attractive for nearly all involved – they just don’t necessarily reflect the truth! It has all gone way too far and this observer, for one, has had enough of it.

Wishing you well for 2020!

As ever, if you have any questions or would like to discuss anything wine related, do let me know.

by Wine Owners

Posted on 2019-10-08

Is it time to hit the bottle?

At the risk of sounding like a stuck record, the market mood is sombre. It does, however, remain reasonably steady amidst a turbulent sea of macro factors.

Hong Kong is an important market for wine and the ongoing protests are a concern. The original cause of complaint, an extradition agreement between the territory and the Chinese mainland, has long since been retracted but the protests continue, becoming ever more violent. This is about democracy and freedom and the eyes of the world are watching. It is an uncomfortable position for China who cannot afford to handle the situation as perhaps it might in its own provinces but in the long term, remains a very powerful parent. Already the economic effects are being felt; officially occupancy rates in Hong Kong hotels are currently running at about 20%, unofficially they are in single digits. A quick internet search found a room in the territory for US$9 a night, including breakfast!

As we know, Hong Kong, apart from having its own burgeoning wine scene, is currently the gateway to the wine market of China, legally or otherwise. We expect China will open new free ports in time, but the current troubles may just accelerate that process. We think this is a short term problem but in the meantime, trade form that corner of the world is quiet.

U.S./China trade negotiations and Brexit shenanigans continue, and emerging markets are threatened by contagion emanating from Argentina. Thrown in the unrest in various parts of the Middle East and various other more localised scenarios, it’s a right old mess. And what does well in right old messes – physical assets! Here is the Gold price performance so far this year against the WO 150 index.

We’re not saying there is any correlation, delayed or otherwise, between wine and gold but recent financial history (since the last global financial crisis) has made physical and alternative assets increasingly popular.

We live in an era of negative real interest rates, where buyers of roughly a third of the world’s outstanding bonds will lose money if held to maturity and where even high yielding equities with strong balance sheets are not performing – all very sobering! With all this going on, is it time to hit the bottle?

Within the wine world, my investment themes remain the same; focus on regional allocation, combined with scarcity and relative value is the game.

Please contact miles.davis@wineowners.com with any questions.

by Wine Owners

Posted on 2019-03-07

In terms of reputation Screaming Eagle is the ne plus ultra of American wines, the equivalent of Petrus on the Right Bank, Romanee-Conti on the Cote de Nuits and Conterno Monfortino in Piedmont.

The prices of the wine varies from £2240 per bottles up to £2600 per bottle for the vintages of 2009, 2011, 2012, 2013 and 2014, but over the last two years it has been the 2009 and 2011 that have made the greatest gains, with 37.9% and 42.7% respectively. Double digt growth seems to be the norm on a CAGR basis.

The 100 point vintages of 2010 and 2007 are roughly £3600 per bottle, and have gown at a slower rate in the last two years, suggesting again that there is better vakue to be had in the 97 to 99 point bracket currently.

Current market levels puts the 97 point ’09 at £2602 a bottle and the 94 point ‘11 at £2461 per bottle. These prices are at a premium of £350 and £200 respectively to the 97 point 2013 and 98 point 2014, which would seem a little illogical. Hard to see a justification for a discount for equivalently scored wines. As the chart below shows, the 2011 in particular seems over-priced and the more recent vintages would seem to offer greater upside potential.

Trying to compare Screaming Eagles with other US wines is a rather thankless task as it operates on a different pricing level entirely to every other wine in California. There are several things you can say about it in isolation, however:

- There is no vintage values at less than £2000 a bottle, and many tip the scales at over £3500 per bottle

- Three pack OWCs are the norm – almost all stock available comes in this format

- It has the highest average Parker score over the last twenty years of any wine in the world except Conterno Monfortino

- No more than 700 cases (12 pack equivalent) are made in any vintage.

It would seem logical to suggest for the medium to long term that younger, higher point scoring vintages offer the greatest potential for capital growth. Not for the faint hearted, of course, but the fundamentals of extremely small production, a style that will see each vintage improve for a minimum of 25 years form bottling and a brand that has cemented itself as the epitome of great modern Californian wine making make this a wine that needs to be considered very seriously as an unavoidable component in any top drawer cellar…

by Wine Owners

Posted on 2018-05-17

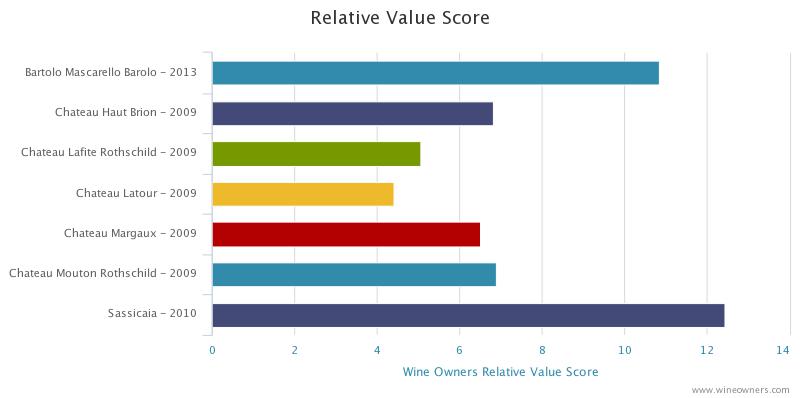

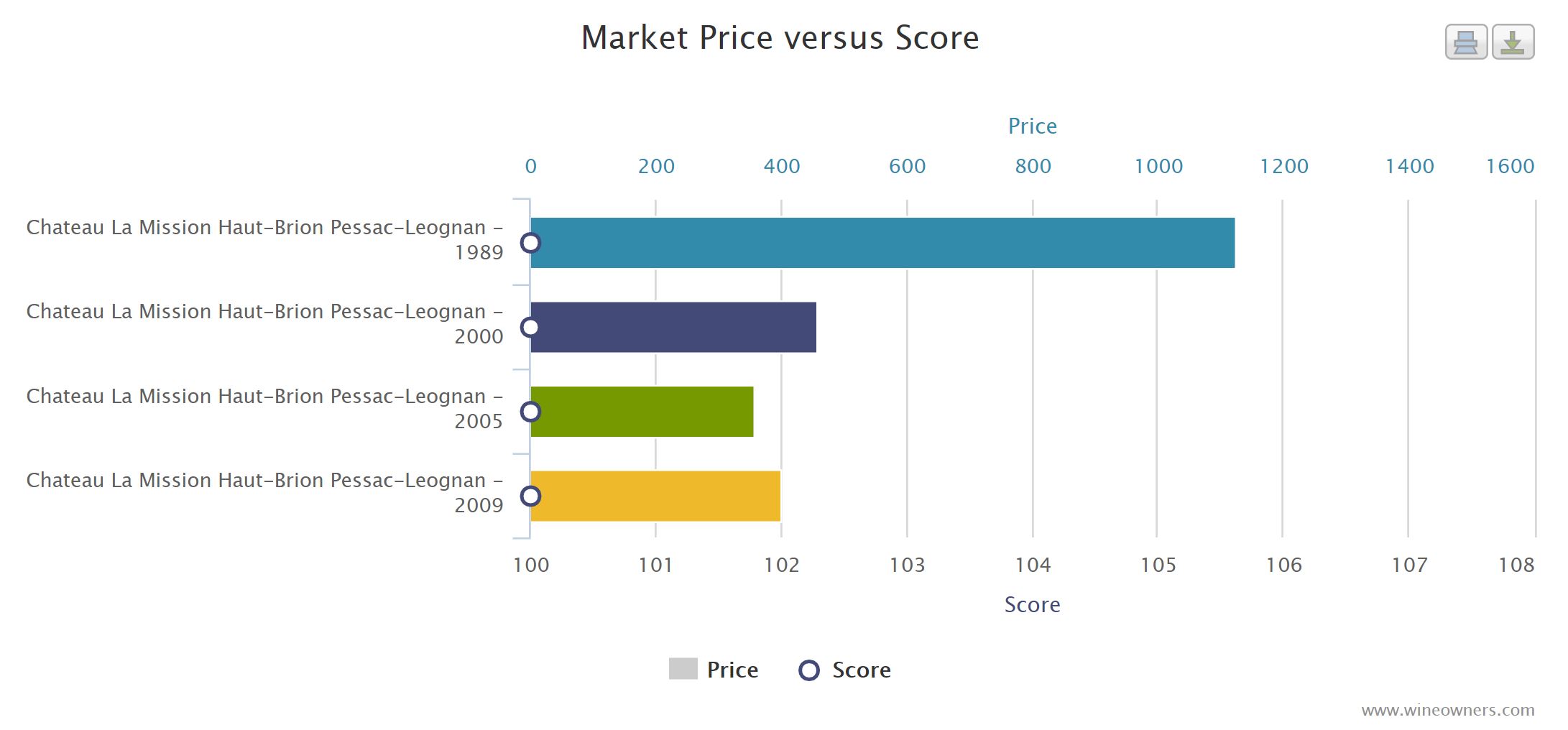

An overlooked example of value for money here from the 100 point La Mission 2005. Compared to Domaine Clarence Dillon stablemate Haut-Brion, and the rest of the 2005 First Growths, 2005 La Mission is a clear winner in terms of value as is eminently clear from relative value analysis. The only other 100 point wine on the whole left bank is Haut-Brion, which trades at around £6,500. The other Mouton will cost £5,250, Latour £6,600, and Margaux £6,100, all on 98 points, while Lafite lags behind them all in relative terms, commanding £7,700 for 96 points.

Compared to other 100 point La Missions over the year, the 2005 wins out on relative value as well. Whether any of the 2009, 2005 and 2000 will hit the price highs of the legendary 1989 is a subject on which the verdict is very much out, and will depend on how reputation of the vintages develops. Nevertheless, all three look like relatively sound buys, and the 2005 at the offer price just beats the rest (assuming they can be bought at market level).

“The 2005 La Mission Haut-Brion is pure perfection. It has an absolutely extraordinary nose of sweet blackberries, cassis and spring flowers with some underlying minerality, a full-bodied mouthfeel, gorgeously velvety tannins (which is unusual in this vintage) and a long, textured, multi-layered finish that must last 50+ seconds. This is a fabulous wine and a great effort from this hallowed terroir. Drink this modern-day legend over the next 30+ years. Only 5,500 cases were produced of this blend of 69% Merlot, 30% Cabernet Sauvignon and 1% Cabernet Franc.”

100 points, Robert Parker

La Mission Haut-Brion 2005 is offered £4,300 on the Wine Owners Exchange (£4,435 including fees)

by Wine Owners

Posted on 2014-10-20

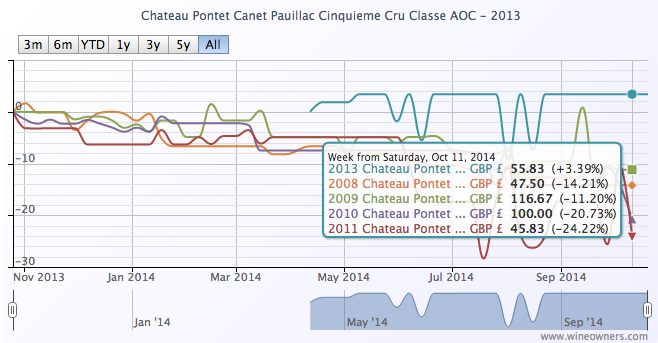

Why is there apparently so little wine in Bordeaux when so little of more recent vintages has been selling through? Why buy young wines at release? Will negociants’ balance sheets cope with more vintages that stick? Why would that happen?

Pontet Canet 2013 famously ‘sold out’ within an hour or two of being offered on the Bordeaux Place. Negociants sucked it up and took their allocations. That’s their historical role after all. Merchants generally weren’t having any of it. More relevantly, nor were their private clients. It was a lousy deal for the consumer: 2002, 2004 and 2006 are all cheaper vintages.

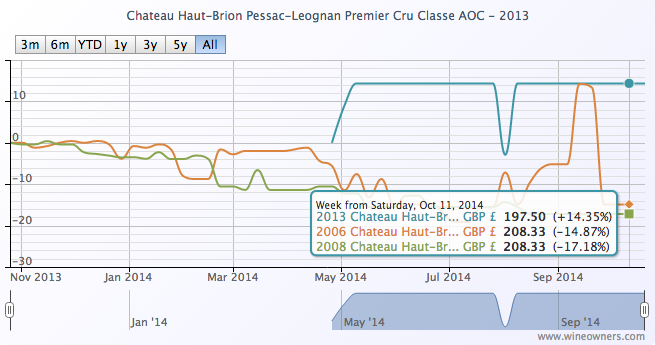

Now we’re on the cusp of a rather good vintage, the first in a small handful of years. Haut Brion 2008 has been trading at £2,400: a fair price for a lovely wine. To be a good buy, what will Haut Brion 2014 need to be offered to consumers for? £2,000? £1,900? £1,800? If instead it’s offered for £2,500, for example, what would be the point of buying it?

Loyalty? Surely not. Would consumers really want to play the stockholder for Chateaux that made extravagant profits out of 2005, 2006, 2009 and 2010 vintages? Some of who pillaged the European Union’s agricultural support fund during the bloody aftermath of Lehmann to construct a new chai or two? Buy into wines that might not drink for 15-20 years and might not be materially more expensive in 2 or 3 or more years’ time? Wines that are made in such benevolent quantities that finding them won't take more than a couple of minutes online? When there are so many back vintages that are coming back down to earth and are challenging our perceptions of value over the last few years?

So let’s imagine that the 2014 vintage proves a tricky sell. Not as thankless a job as the unloved 2013 vintage of course. The really big merchants who have an economic interest in en primeur to succeed and will sell the vintage: the weather, the brilliant Indian summer, the inevitable comparisons with the weather of 1996. Those cool nights, dewy mornings and balmy days under clear skies. But imagine it’s not what you might call a ‘successful’ campaign…

What happens then? How many of the negociants will be able to stomach another huge influx of stock without a corresponding outflux? With credit harder or impossible to come by; stalling European growth; a currency still fairly strong but with a significant downside, undermined by Europe’s recession-states, impatient creditors and a faltering Germany? With banks increasingly wary of lending support?

Of course some negociants will seize the moment to consolidate their position, increasing their market share as they gobble up distressed owners and their stocks. But others?

No one is yet disputing the efficiency of the negociant distribution system via the Bordeaux Place. After all, the huge Tuscan estates were sufficiently impressed by the system to want in. (And if you want your Libournais estate to be Classé, woe betide you if you try to circumnavigate the system.)

But it doesn't automatically follow that you have to believe in en primeur as long as it undervalues the consumer’s stockholding role to adhere to the established Bordeaux distribution model.

Passion-driven many of us may be, but perennially stupid we are not.

by Wine Owners

Posted on 2014-02-06

Average cellar size £60,000

Total cellars under management £40m

|

January |

Overall |

| Bordeaux |

26% of total trades |

39% |

| Tuscany |

23% |

12% |

| Rhone |

21% |

13% |

| Burgundy |

21% |

17% |

Enthusiastic reviews from Antonio Galloni seem to have piqued interest in the 2010 vintage in Tuscany and Piedmont, with back vintages in Tuscany hanging on the coat-tails of the 2010. The tried and tested Supertuscans seem to be the big winners, with trading users offering and bidding around Sassicaia, Ornellaia and Masseto in mid January, with a high correlation of offers to trades across the region.

The inclusion of some excellent new private collections of Rhone and Burgundy in December and January have pushed up the market share of those regions to rival Bordeaux in those months, with a spread of private and trade buyers picking up top wines from producers like Guigal, including a rare parcel of 1989 la Turque trading at £2,900.

Bordeaux, even in a relatively flat market for the region, continued to account for the largest percentage of Exchange trades in January. Interest focusses around classic wines such as 1982 Latour (recent trades at £13,300), top scorers, and ‘off’ vintages, particularly among the first growths. On the right bank in particular, 2005 appears to be attracting new interest where the price is right, so perhaps the prospect of an uninspiring En Primeur season is already encouraging sparks of interest in great vintages with a track record of quality and performance.

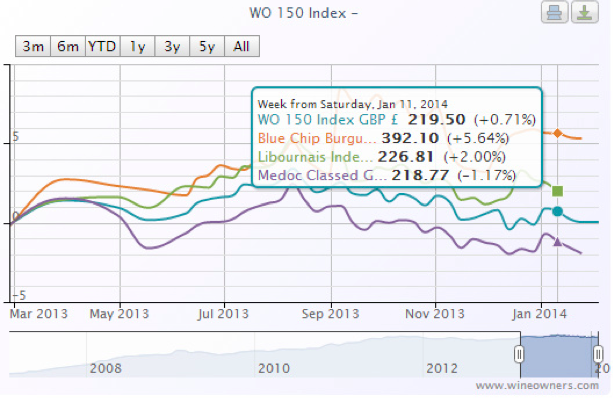

Index comparisons show a relatively flat year’s market, with Medoc Classed Growths slightly underperforming, and top level Burgundy slightly bucking the trend by showing 5.6% growth compared to a base value at Feb 2013.

by Wine Owners

Posted on 2013-10-18

Comparing the 2009 and 2010 vintages of the overachieving Chateau Smith Haut Lafitte shows how vintage styles can make a huge difference to market value. The massive and opulent 2009, which wins a perfect score from Robert Parker, is by no means a huge qualitative improvement on the slightly lower rated 2010. In fact, as we’ll see, plenty of reviewers prefer the 2010.

The obvious feature of the price comparison below is that the market price of the 2009 with its 100 point rating from Robert Parker has risen by well in excess of 100%, while the 2010, which gained a few points on its initial rating (95-97, rerated to 98+), has remained steady at close to release price.

One point to take away is that a very good re-rating is not enough to take a price higher in the current market unless it is a perfect rating. While this may be disappointing for those who bought 2010 and not 2009, it does mean the 2010 is considerably less expensive to buy now, in what is a relatively low market. Considering Neal Martin, Wine Enthusiast and Jancis Robinson all rate the 2010 higher than the 2009, albeit marginally, it certainly seems the better buy of the two vintages with a market value of £870 against 2009’s £1,487. For a price conscious buyer, the prospect of spending almost double for an extra 2 Parker points might seem hard to swallow, so unless the particular style of the 2009 appeals very strongly, the 2010 feels more like a reasonable price for a wine of that quality.

|

2009 |

2010 |

| Robert Parker |

100 |

98+ |

| Neal Martin |

94 |

95 |

| James Suckling |

96 |

95 |

| Jancis Robinson |

17.5 |

18 |

| Wine Enthusiast |

94 |

96 |

| Wine Spectator |

96 |

96 |

| Wine Owners |

95 |

94 |

How does it look in comparison to other comparable wines? Similar scores in Pessac were achieved by Haut Bailly (98 RP) and La Mission Haut Brion (98+):

Haut Bailly has put on a similar amount of weight, but is still quite a bit more expensive to buy at around £80 per bottle. Both wines have outperformed the Wine Owners 150 Index, showing an encouraging ability to hold value in a difficult market. Honorary First Growth La Mission Haut-Brion, on the other hand, has behaved just as one would expect of a top flight wine that didn’t quite make the perfect score, slipping steadily downwards to 15% below the ambitious release price. At around £5400 per dozen, it makes the other two look like good finds.

Perhaps the most interesting thing to note here, though, is the huge influence that Wine Advocate scores continue to exert on market prices, particularly in Bordeaux. With Parker’s sale of his stake in WA, and the high profile departure of influential critics like Jay Miller and Antonio Galloni, many might like to think that the journals days as a key market influencer are numbered. Commentary abounds about the future of wine criticism, whether the future lies in collaborative reviewing along the model of Cellar Tracker, aggregate scoring, or whether a new super-critic will emerge to take Parker’s place. The numbers, however, tell a different story, and testify strongly to the market’s desire for a reference point.

2010 Smith Haut Lafitte is available on the Fine Wine Exchange at £820 IB