by Wine Owners

Posted on 2022-10-13

Today the wine part of the Wine Owners team, as opposed to the tech team who provide our best-in-class software solutions, tasted wines from one of the great sub-sections of the Union of Grand Crus; it is called the Bordeaux Grands Crus Classés - to avoid confusion!

Wines offered came from 2018-2021 vintages. What was abundantly clear was that 2019 has reconfirmed itself as the best of modern vintages. Also, 2018 is not for the faint hearted, especially Montrose, and also that second wines offer a lot of drinking pleasure at a diddly squat fraction of grand vin prices. La Dame de Montrose excelled, as did La Croix de Canon. The unpronounceable Chateau d’Aiguilhe from the Cotes de Castillon performed well, as usual (apart from the ’21), and at £150 per 12 in bond for the 2019 is remarkable value. Chateau Canon reinforced its ‘polished’ status and was probably the most consistent.

There were some volatile samples of ‘21s, which we imagine not to be representative.

To my mind, the question is not what to buy but when to buy, if you haven’t already - 2019 should be in everybody’s cellars.

Chateaux represented:

Smith Haut Lafitte

Gazin

Vignobles Comtes Von Niepperg - d’Aiguilhe, Clos de l’Oratoire, Canon La Gaffeliere, La Mondotte

Canon

Rauzan Segla

Branaire Ducru

Pontet Canet

Montrose

Guiraud

For enormous pleasure and for a twist on sweet wines, readers should definitely embrace the current trend of lighter wines from the region. Fresher and less sweet wines from Sauternes were particularly well represented by the second wines of Chateau Guiraud and these will make a very stylish aperitif. The dry whites of Smith Haut Lafitte were superb, and are so often overlooked for more obvious alternatives, Burgundy normally, as are most dry white Bordeaux wines - in the U.K. at least.

Miles Davis October 11th 2022

by Wine Owners

Posted on 2021-07-11

Will Cheval Blanc and Ausone no longer be Grand Cru Classé ‘A’ as from the 2021 vintage?

If so, it won’t be because of the Commission de Classement. The closing of the Saint-Emilion classification applications took place on June 30 and neither Cheval Blanc nor Ausone returned their copies.

Unlike the left bank classification system of 1855 that is pretty much immutable (with the exception of Mouton’s promotion to Premier Cru in 1973), the St Emilion classification is reviewed approximately once every 10 years, permitting a periodic revaluation of quality and performance. It’s not all been plain sailing; the 2006 reclassification was plagued by accusations of impropriety and was eventually annulled. Consequently, tastings conducted for the 2012 reclassification were outsourced to independent groups from across France to rehabilitate the process.

Cheval Blanc and Ausone, the first St Emilion producers to be awarded Classé A classification in 1954 when it was created, are effectively leaving the classification system.

The Classé A incumbents evidently concluded that the system is no longer sufficiently discriminating to reflect the ranking of their respective properties compared to their peers.

This bombshell threatens to undermine the kudos and financial benefits of promotion to Classé A, and in turn the market pricing potential of those that are elevated. Not to mention it raises questions of the credibility of the St Emilion classification system more broadly.

So what does the two colossus’s departure say about the process of decennial review? How does this reflect on the composition and process of the Commission de Classement?

Is Grand Cru Classé A about to lose its lustre; devalued by ambitious properties busy erecting glitzy edifices? Concrete and stone, some say, matter more than they ought to compared to the brilliance of the wines and their track record.

Or, is Classé A promotion a reflection of the qualitative transformation we see taking place in St Emilion - given the strongly weighted preconditions of a sustained track record of exceptional results and market recognition - and therefore are not elevations thoroughly deserved?

Let’s see what happens over the coming weeks. Can Cheval Blanc and Ausone be courted back into the fold, or is their departure (by omission of submission) a fait accompli? Assuming the latter, perhaps we'll see more promotions next year than we might have otherwise. What effect this all has economically on those producers who attain Classé A classification is now more uncertain than ever.

by Wine Owners

Posted on 2020-06-04

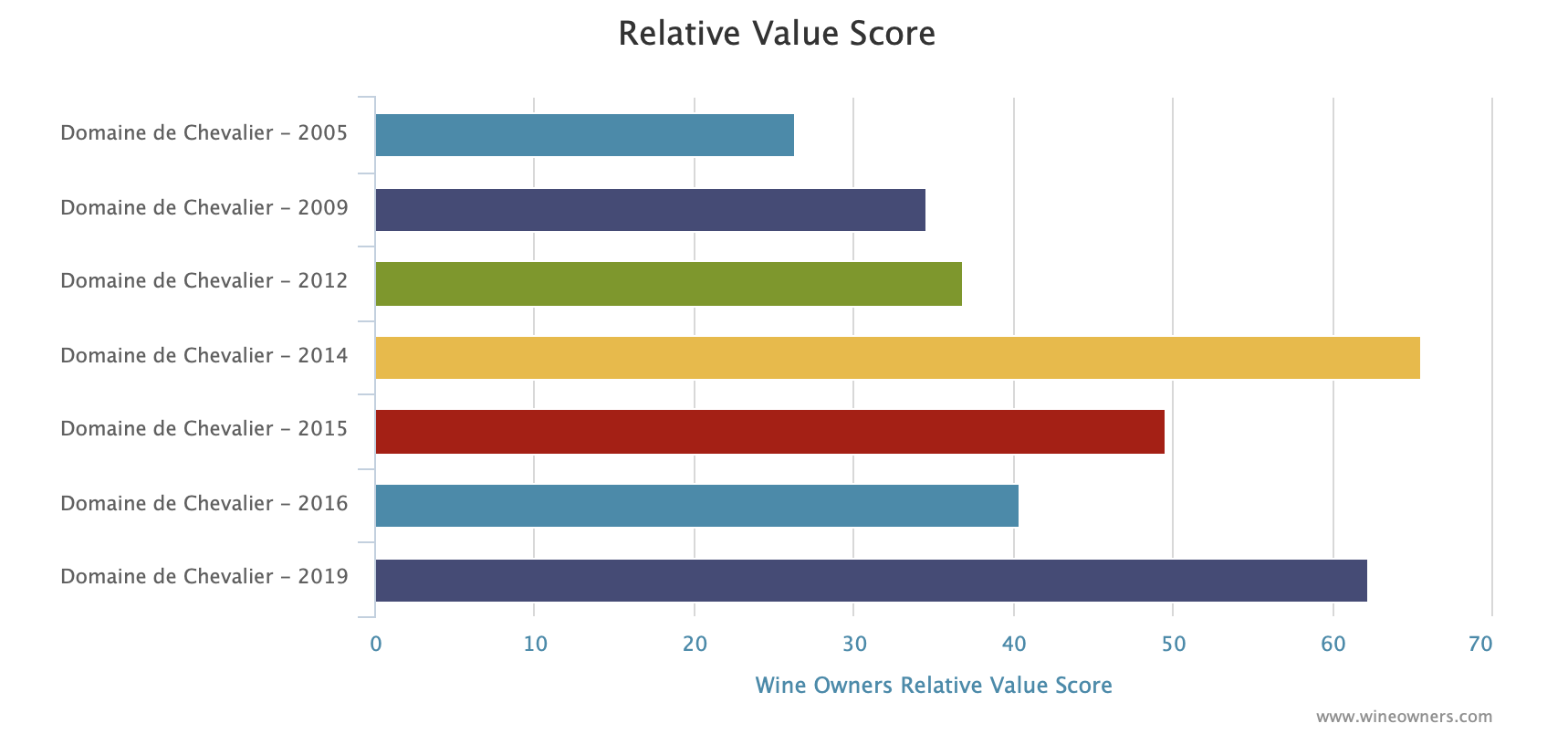

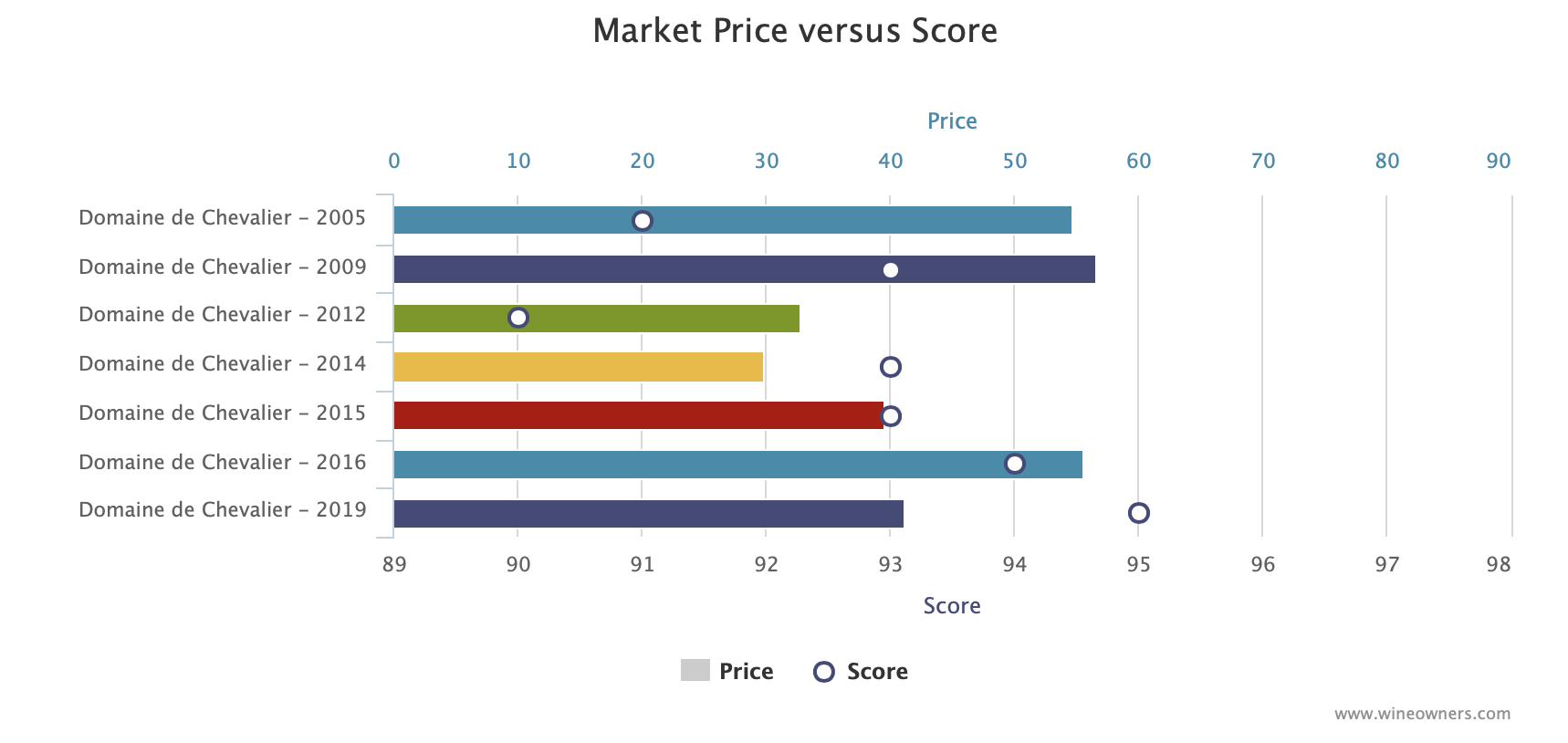

Chevalier is out this morning at £247 per 6, a perennial favourite and on the back of a seemingly great success in 2018. Hopefully in 2019 they’ll have tamed the merlot alcohols which hit 15 degrees in 2018. Bordeaux being blends saved the day and early pickings of Cabernet brought the assemblage down to under 14 degrees. Still, that kind of inherent excessiveness does make you wonder. Chevalier does age with unusually consistent grace no matter the kind of vintage.

Relative value analysis points to 2014 as being a rather decent pick of an excellent run of recent vintages. 2019 is fairly priced for collectors of this lovely estate but not to attract the short term profiteers.

Banner Image: http://www.domainedechevalier.com

by Wine Owners

Posted on 2020-06-03

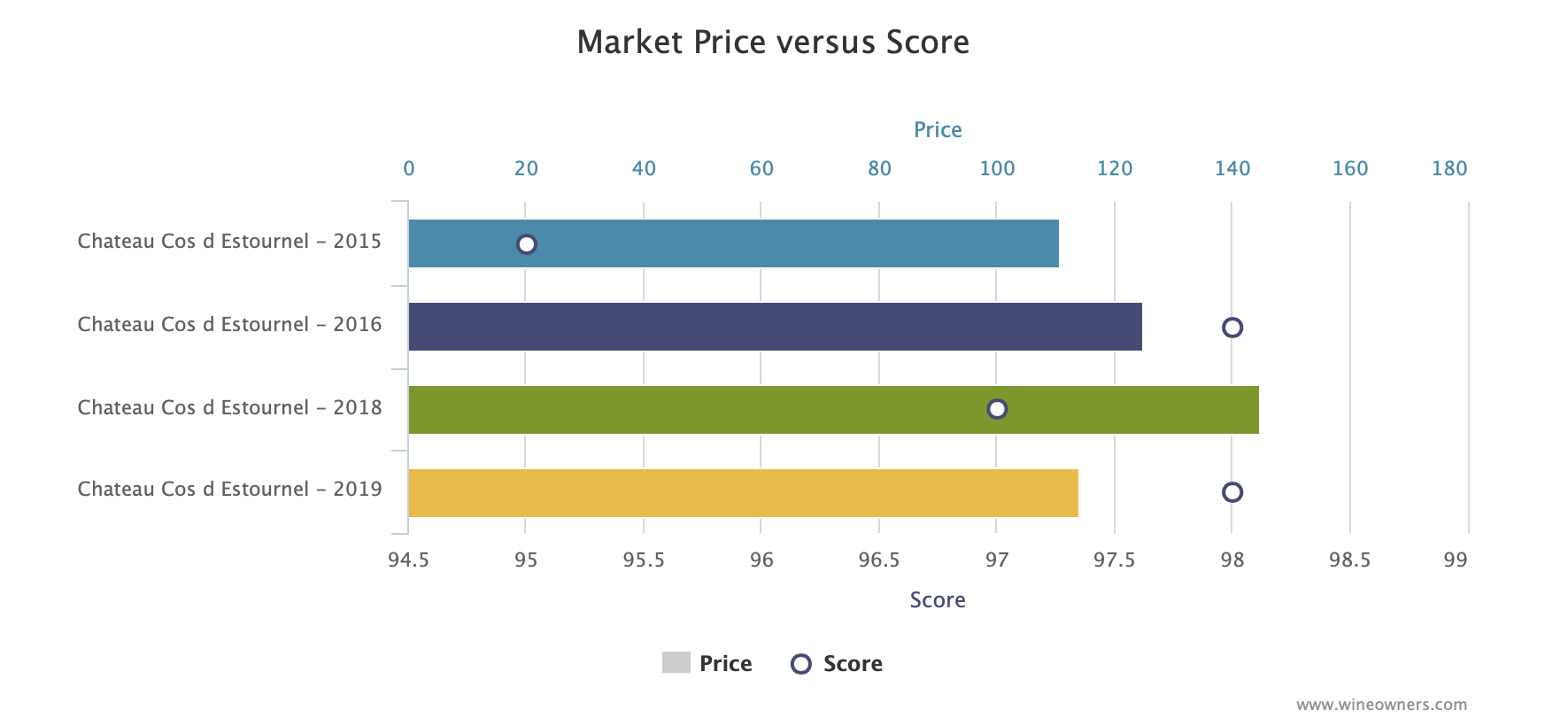

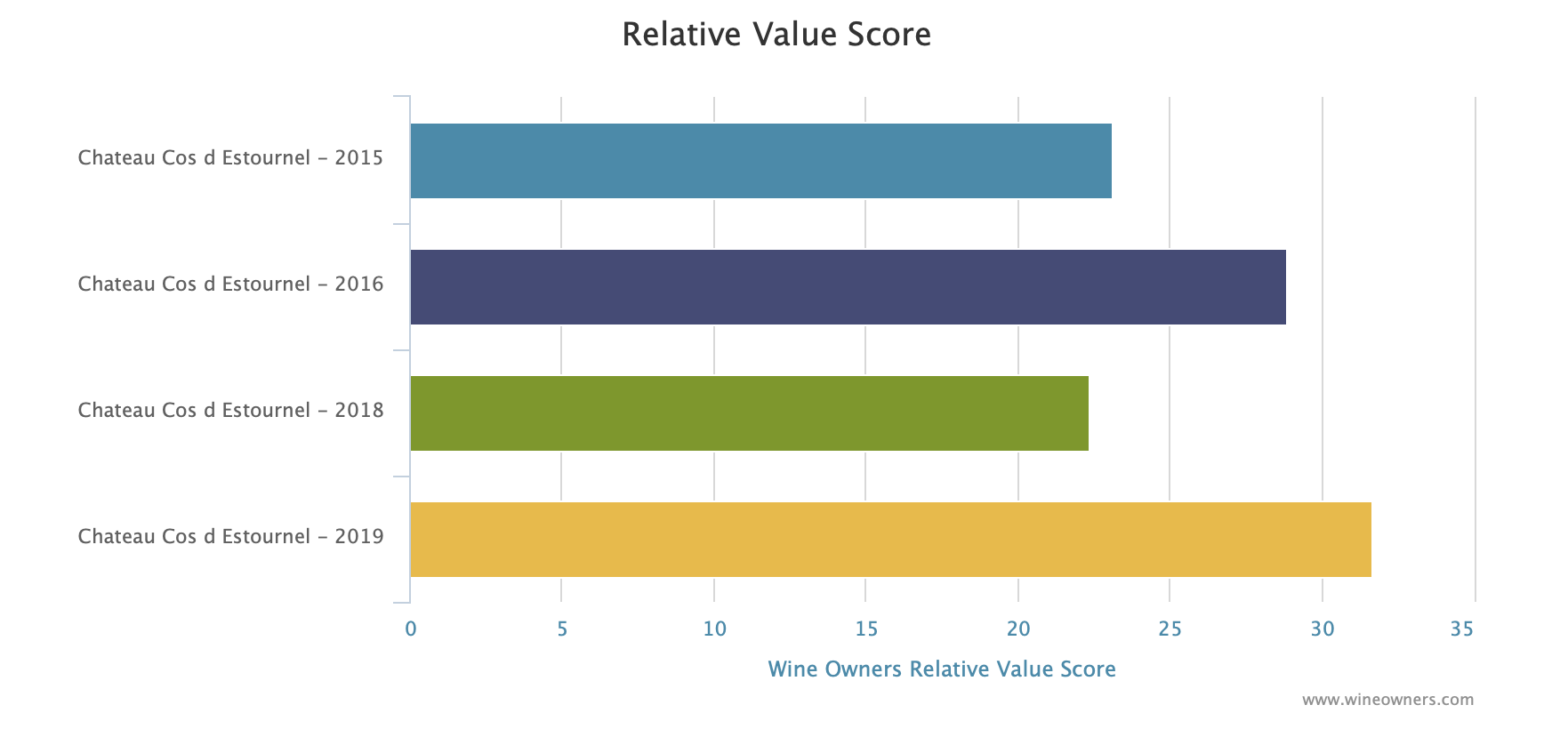

Cos d’Estournel is out £684 per 6. -23% down on 2018. Great wine they say but is the price reduction enough?

The magisterial 2016 is hovering 10% above this release price, which is among the greatest young Bordeaux Lisa Perotti-Brown has ever tasted, it’s in bottle and widely available, so we think they needed to do a little more to make this really attractive. However good the 2019 proves to be, it does not prompt the same compulsion to buy this year as Pontet Canet and Palmer.

Prices and points (we have allocated 98 points)

Banner Image: www.estournel.com

by Wine Owners

Posted on 2020-06-02

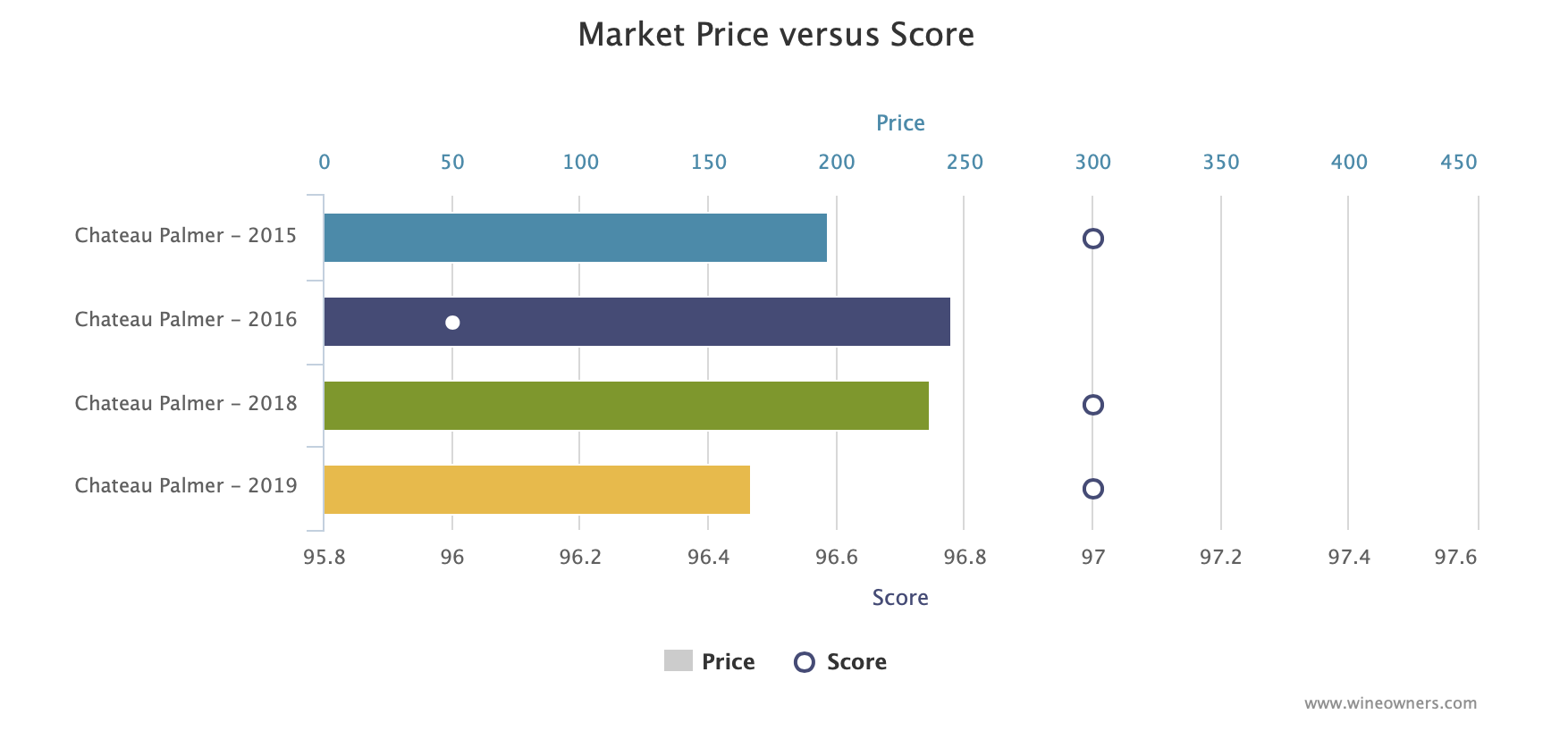

Palmer was released this morning at £999 per 6, a 31% reduction from the (pumped-up) pricing levels of 2016 and 2018. We are back into rational release pricing territory.

Does it work? Absolutely. Note we have put in a placeholder of 18 points but it works at 17 points too.

At this rate, if the whole of Bordeaux rallies around the reduction level of -30% to -35% set by Pontet Canet and now Palmer (and rumoured to be the level of reduction that Lafite will apply), this’ll be the first en primeur campaign since 2014 where it would make sense to buy more broadly than the very specific, narrow range that we’ve suggested makes any sense at all in the last 3 campaigns.

Here’s the analysis of Palmer.

First pricing and scores:

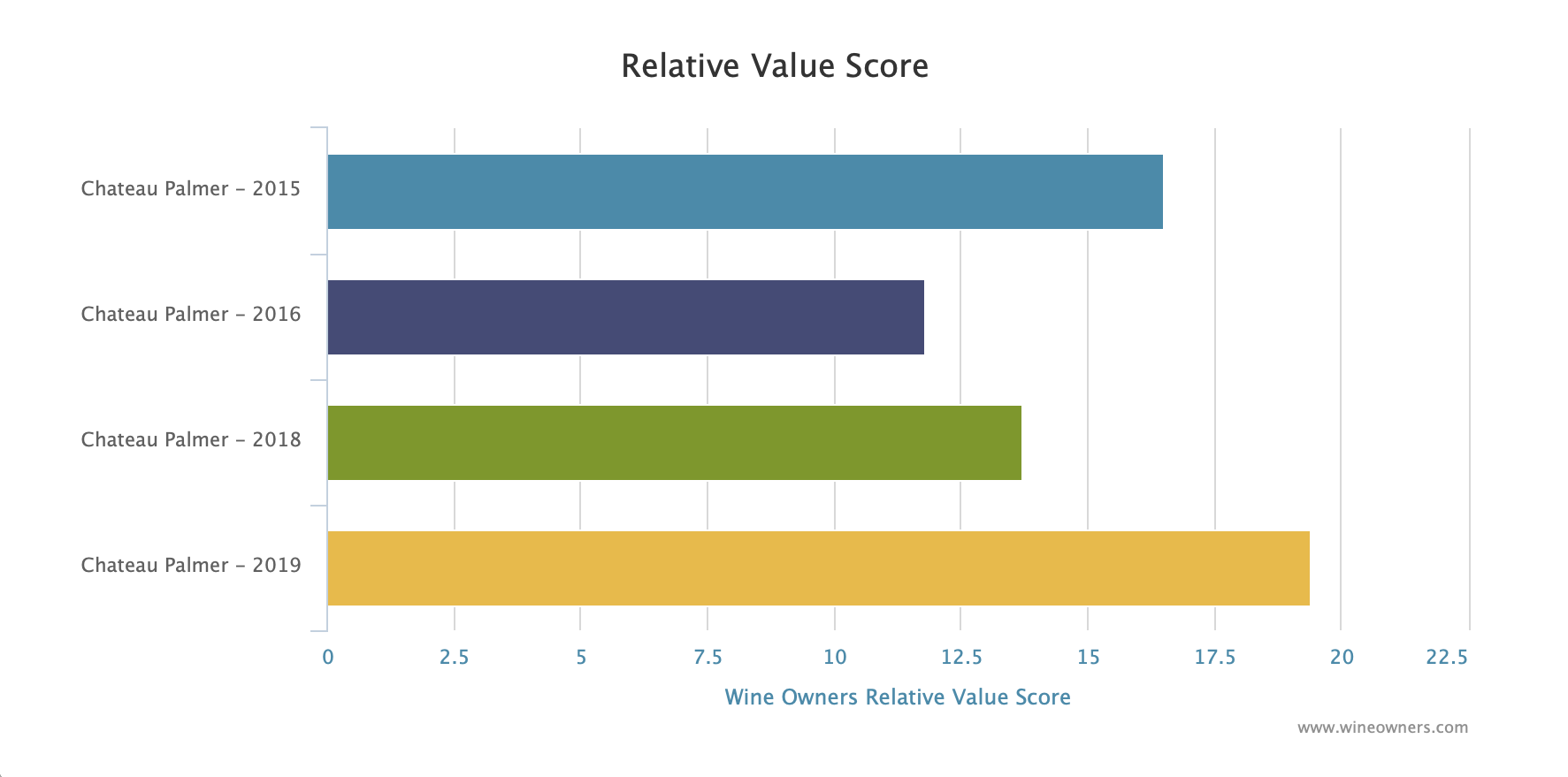

And the relative value calculation. Note how much longer, and therefore better value, the 2019 bar is than any of the comparative vintages used for the analysis:

Banner Image: www.chateau-palmer.com

by Wine Owners

Posted on 2020-05-27

So Latour 2012 is out today at £350 a bottle. What’s that got to do with 2019 EP I hear you ask? Well coming as it does just before the releases of the 2019 big boys, and because it’s the first release from Latour that wasn’t previously released EP, it’s seen as a test of the market and what the consumer’s appetite is for laying out hard earned spondoolies in The Time of Covid.

I’ve seen emails from merchants this morning gushing that this is the cheapest Latour in the market today, and how they’ve got the pricing right.

The retail channel needs to see the 2019 releases come out minus 30% v 2018. That would put Lafite et al at around £2,000/ 6 and at that price it would sell. Plus it might just re-energise the Bordeaux secondary market with a dollop of positive sentiment.

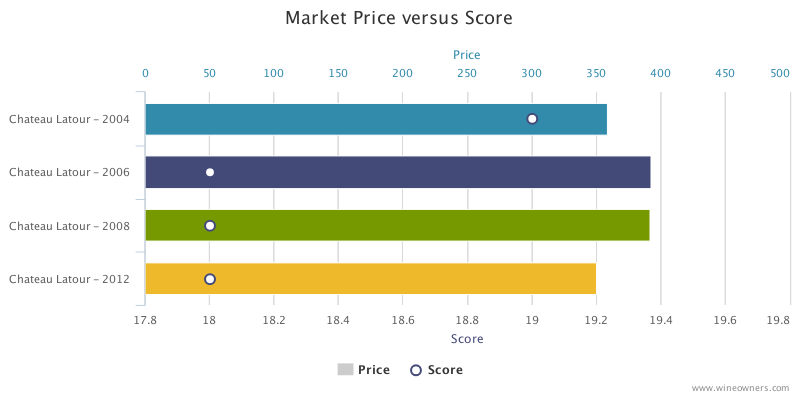

However If we compare 2012 Latour to other comparable vintages of Latour, so say 2008, 2006 and 2004, which I think is rather realistic, we see a very different picture.

Here’s the market price and JR points plotted for 2012 and those benchmark vintages selected:

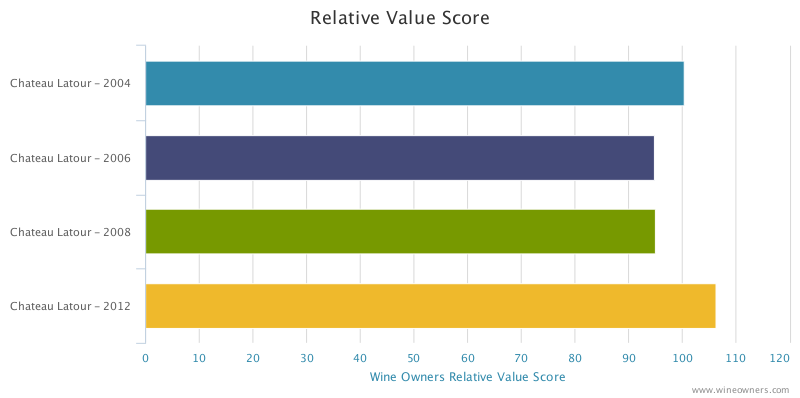

And here’s the weighted effect of that taking into account scores:

The longer the bar the better the value, the bigger the gap between the longest and the next, the more compelling the buy. Not much in it is there? Which says that Ch. Latour, far from doing their 2019 EP peers a massive favour, have given absolutely nothing away. There’s no Covid discount baked into this price. The best you can say is that there’s no guff about ex Chateau premium.

So, as a curtain raiser, it's a damp squib. But that’s their release model now and who’s to say they are wrong? At least we know what we’re drinking. The reply to this question, answerable only by Lafite et al, will come soon enough.

by Wine Owners

Posted on 2020-05-20

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.” Charles Dickens.

18th May 2020 kicks off the Bordeaux 2019 en primeur campaign with the release of Chateau Angludet. They’ve partially gone down the amphora route to gain purity. It’s a great success, a very great Angludet, according to a number of merchant emails received today. Those same emails belie one small issue - that the wine has yet to be tasted. A reminder of the impact of Covid-19, the anxieties and emotions over this year’s releases dominated by hope and despair. So we have to take the Bordelais at their word that it’s a great vintage, fresher than 2018, in the same mould as 2016 or 2010. I’m sure producers are excited by what they have in cask or tank or whatever receptacle the juice is in these days. But it’s not unjustified to say that local opinion isn’t always entirely objective. So bring on those Chronopost and UPS samples and let us all taste...

We have to be honest, we’d have much preferred a deferral of the campaign to October after the harvest. We don’t agree that would have caused any issues with other regions’ releases. There is something very strange about releasing a futures campaign whilst so much of our economy is in deep purdah. But the die has been cast and June it is (for the 60-odd releases that the market chooses to focus on).

The choice of timing of the releases is significant. It is quite obvious that, just like the 2008 vintage release, there will have to be a very significant reduction in release prices for 2019 to find a market. Those properties who have tended to use en primeur more as a marketing opportunity than a selling one will have to think about what it means to them: the prospect of a marketing campaign has more or less evaporated. For those properties who expect or need to sell a sizeable percentage of the harvest, only one one of the four marketing ‘P’s matter. It can be the best vintage in the world, it can garner (in the fullness of time) more 100 pointers than any of the last 40 years, but success will boil down to one thing and one thing only: price.

That decision will have ramifications on the whole of the Bordeaux global secondary market. A significant reduction of 30%-40% can ignite interest in the region’s great wines. It can draw in a new generation that has largely ignored the region, or doesn’t see the point of purchasing new releases two years before shipping. It can reward buyers of the last vintages who are under water and likely to remain so. A compromise that shows intent but brings us back to the levels of 2015 will consign Bordeaux to another year in the shallow quicksands of a secondary market lacking direction, fearful of the future, unwilling to commit cash, failing to see the point anymore.

Ah, I hear you say, but the world is awash with cash desperately looking for a home, just as it was post-Lehmann - when the fine wine market benefitted royally. I disagree. We are entering uncharted waters and cash in the bank trumps FOMO, the fear of missing out. Warren Buffet can be wrong sometimes, but not all the time, and moving to an underinvested position does not seem completely crazy.

So let’s say that 2019 is the equal of 2016, increasingly recognised as the greatest classic Bordeaux vintage in a generation. 2019 is likely not its older sibling’s equal (probably, but who knows) but let’s pretend it is for a second. Even on this most optimistic reading of the new vintage, would you rather buy into a vintage that has been tasted, re-tasted, evaluated ad infinitum and has withstood the scrutiny of the entire market, or roll the dice with a vintage that will be narrowly evaluated based on posted samples? Add to that 2016 prices that have barely moved or drifted down, and the comparative case for 2016 is about as strong as it gets.

Bring on June, and a prediction: either the most successful en primeur campaign since 2016 (notwithstanding Covid-19) or a non-event, determined purely by one variable - price.

Nick Martin

20th May 2020

by Wine Owners

Posted on 2019-07-09

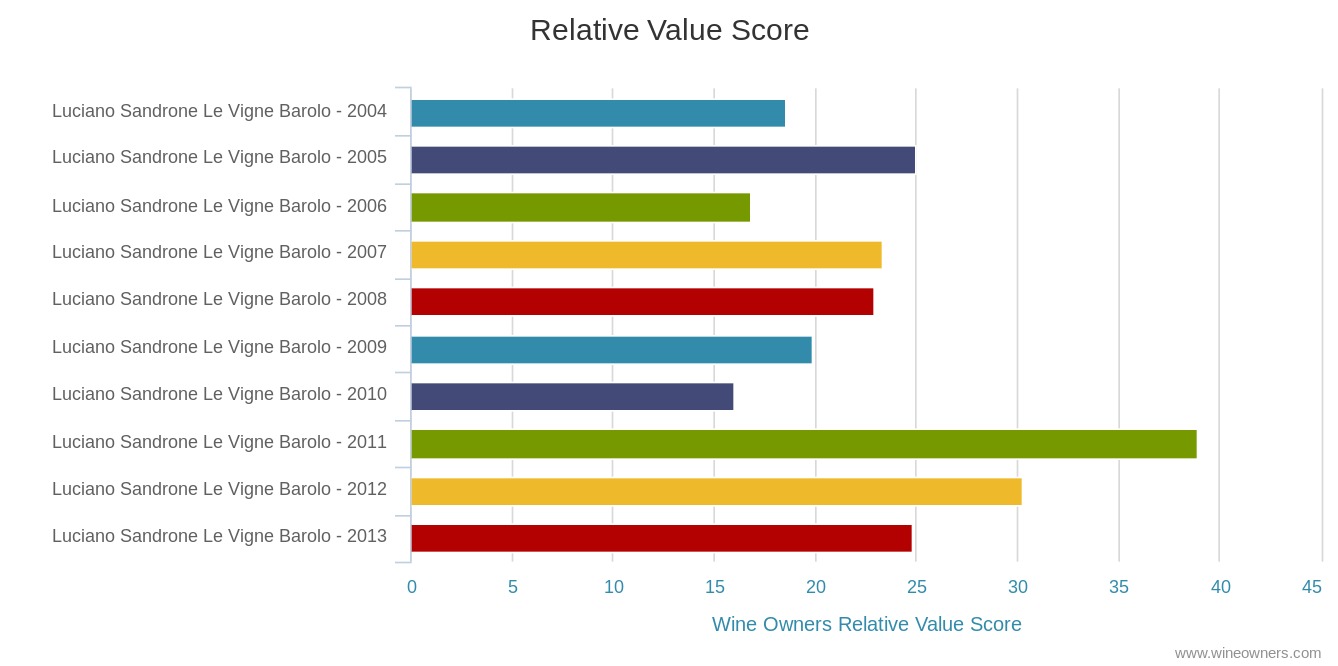

The reputation of Luciano Sandrone continues to grow and grow, in keeping with the popularity of Barolo. Not as famous as the very top tier of Bruno Giacosa, Giacomo Conterno or Giuseppe Rinaldi but nestling just in behind, at a far more attractive price point.

Here we consider Le Vigne cru although the story is much the same for the slightly more expensive Cannubi Boschis (renamed Aleste in 2013 – in classic, designed to confuse, Piemonte style!).The consistency of the scores is incredible - through a mixture of very varied vintages from ’06-’15 the average is 95.3 points (Wine Advocate). Very significantly, the estate releases a small amount of the exact wines (under the labels Le Vigne Sibi et Paucis and Cannubi Boschis Sibi et Paucis) after ten years of age and they consistently achieve greater acclaim at that point, the ’07 going from 96 to 99 points (WA) for example. The range of points scored would indicate these are very fine wines indeed and given the rarity, must be only affordable to only the mega rich. Not so, prices start at c. £60 a bottle, rising to c. £170 for the stonking 2010 vintage.

For comparison sake I looked at some other fine wines from Burgundy and Bordeaux over the same ten year time period. Obviously these comparisons will never be exactly like for like but the differentials are not that great either; brilliant producers from the top tier of their respective regions, producing internationally acclaimed wines from the best local grape varieties designed to take advantage of their particular terroirs and climates to the full. We have a decent premier cru Burgundy, Domaine Dujac Aux Combottes, a sensational Pomerol on top of its game, Vieux Chateau Certan, and the king, Chateau Petrus (just for fun):

Comparisons between ‘06-‘15 vintages: |

Av. points

|

Av. Price

|

Highest price

|

Luciano Sandrone Le Vigne Barolo DOCG |

95.3

|

£98

|

£170

|

Domaine Dujac Gevrey Chambertin Aux Combottes Premier Cru |

91.6

|

£170

|

£234

|

Vieux Chateau Certan |

94.1

|

£134

|

£220

|

Petrus |

96.1

|

£2,200

|

£3,250

|

I suggest there is room for significant upside for this Barolo. And I am going to start selling the Combottes I own, the differential is absurd and further illuminates how crazy Burgundy prices have become. Production of fine wine in Barolo (and Barbaresco) is tiny compared to even Burgundy and completely miniscule in what we could consider the ‘investable’ candidates.

Please see charts for Market Price and Relative Value Scores for available vintage comparison.

Miles Davis

9th July 2019

by Wine Owners

Posted on 2019-07-08

The highlight in June for the wine world was clearly the Daily Telegraph event ‘Wine; for profit or pleasure?’. A sell out crowd witnessed excellent talks from four leading experts from the wine world, including two of us from Wine Owners (Miles and Nick). Please contact us for a copy of the presentation.

Otherwise June was again tranquil with trade bobbing along just fine but with no particular surges or dips anywhere. Global stock markets enjoyed a rise after Messrs. Trump and Xi found some accord but this doesn’t seem to have inspired the wine market as yet! Wine stock levels are healthy amongst Asian traders so not even a continuing depressed sterling is bringing about much marginal demand from that corner although most indices are in positive territory in June.

The Bordeaux en primeur campaign came to an end with an almighty whimper. En primeur gets under the skin of the wine trade and all involved spend far too much time talking, writing and moaning about it…yet even so, I shall continue! Within the wine market(s) it has represented very poor relative value for a decade, prices are just too high, yet merchants don’t dare turn their back on this once great provider. It was a great system for all involved, including the man on the street. Now only a very few wines ‘work’ each year (whereby they make sense to the supply chain and the end buyer). And now, to compound the problems of high prices, the Chateaux have decided to retain more and more of their own stock. How this comes to market, when and at what price will fuel debate but based on the evidence of the mighty Chateau Latour, the market may just turn its back. The feeling of stock overhang may easily outweigh the feeling of short supply and it’s not as if the world is going to go thirsty, there will always be alternative choices.

If only our Italian friends came together with a synchronised offering, we could have a proper old school primeur market again. All the market players would have to be involved at the same time, jostling for position, scrapping over every six pack and would still be able to sell at a price that would make everyone happy. The hype that the merchants used to create in Bordeaux primeur markets, that we are still hungover from, could be regenerated. We all miss the hype and the excitement which created such fear amongst the white-faced, panic-stricken collectors and consumers who couldn’t possibly stand even the faintest whiff of FOMO (fear of missing out).

As it is, Italian releases come to market in no organised way and importers and merchants release when they feel like it. It’s all very Italian really but it does make buying easier. We have been acquiring some 2015 Barolo new releases from Fratelli Alessandria, whose reputation is markedly on the up. Prices are very reasonable for these high scoring wines, ranging from c.£35 per bottle for their basic Barolo (94 Wine Advocate points) to nearer £60 for their top cru, Monvigliero (96+). Outside of the very top group, Luciano Sandrone is another producer worth mentioning - consistently high scores at affordable prices. Their equivalents in quality in either Bordeaux or Burgundy would be far more expensive.

Piedmont is easily our favourite region at the moment, due to the demand/supply equation and the blue chips remain well bid. Whilst Bordeaux and Burgundy remain lacklustre, Champagne and Rhone have attracted some attention. There is no question we would recommend the brilliant 2008 vintage in Champagne and the recently released Sir Winston Churchill looks a good bet with the ’96 being double the price.

Please see the Blog for more articles about the wine investment market.

Miles Davis

8th July 2019

miles.davis@wineowners.com

by Wine Owners

Posted on 2019-05-13

This time of year in the wine trade is always dominated by the Bordeaux en primeur circus. Please see our 2018 ‘In a nutshell' report here. It’s strange really, as en primeur has not made commercial sense for the legions of the swirling and spitting wine trade, let alone the man on the street, for very nearly a decade. En primeur business has shrivelled like a drought savaged grape over the years and there are only a handful of opportunities each year that really make sense. At the time of writing only a few releases have made sense according to our ‘proto-pricing’ (please see jancisrobinson.com), Branaire Ducru, Duhart Milon and Quinault L’Enclos. Palmer sold out quickly (at 2,880 per 12), partly due its rarity (see blog), but also because they have built their brand so brilliantly under the guidance of Thomas Duroux. As a result, Palmer has a strong en primeur following.

In general, the Chateaux are releasing less than ever this year which makes this game ever more senseless. According to one highly experienced trade legend EP is all about building the client base for merchants and clearly the avalanche of similarly persuasive e-mails work to some extent. Experienced wine players are highly selective in the EP arena and returns in the short to medium term are very far and few between. Real scarcity is where it’s at, if you’re hoping for rising prices, and that doesn’t come from en primeur.

| | Level | Month | YTD | 1 Year | 5 Year | 10 Year |

| WO 150 Index | 303 | -0.6% | -2.0% | 6.4% | 57.4% | 83.3% |

| WO Champagne 60 Index | 462.61 | 0.9% | -1.3% | 5.0% | 68.4% | 154.9% |

| WO Burgundy 80 Index | 691.36 | 3.7% | -2.0% | 25.7% | 142.1% | 233.2% |

| WO First Growth Index 75 Index | 276.71 | -0.5% | -2.0% | 2.6% | 45.5% | 71.2% |

| WO Bordeaux 750 Index | 340.71 | 1.0% | 1.7% | 6.3% | 57.5% | 100.3% |

| WO California 85 index | 669.86 | -0.1% | -0.4% | 15.4% | 106.4% | 309.9% |

| WO Piedmont 60 Index | 318.83 | -0.3% | 0.9% | 9.2% | 75.6% | 126.4% |

There were no new themes detected over the month and scarcity is still the biggest driver. Interest in Piedmont is still firm although the monthly movement of the index would suggest otherwise. The same can be said of Burgundy, which is still active but is trading below advertised offer levels, with buyers negotiating harder.

Brexit concerns seem to have been put on hold for now, more through ennui than anything else, which led to some increased activity from U.K. private clients but overall the market trundles along rather than powering up. It’s a time for gentle accumulation on the bid side of the market.

As an aside; several collectors have approached us about reviewing their cellars, mainly to consider what holdings are investment grade and which are not. This has led to most people making the realisation their collections lack structure. The combination of our expertise and the technological support from the platform is proving to be very valuable.